Thank you for contacting

GetTaxReliefNow.com!

or wage garnishment — call us now at +(888) 260 9441 for immediate help.

IRS Payment Plans for Individuals | Immediate Relief

We review payment plan options, including a partial payment installment agreement or a direct debit installment agreement with automatic payments based on your financial condition. Acting quickly can prevent penalties and interest, tax lien filings, or further IRS levy actions as your tax debt moves through the collection period.

What This Service Does

This service provides full representation for individuals who cannot pay their federal tax bill in full and need a structured IRS payment plan to resolve their tax debt while stopping or preventing enforcement. This is not a form-filing service. It is a professional representation designed to protect you and guide the IRS process correctly from start to finish.

Full Representation Under Power of Attorney

When you hire us, we prepare and file IRS Form 2848, Power of Attorney, immediately. This legal authorization allows us to represent you before the Internal Revenue Service.

Once the IRS processes the Power of Attorney:

This step alone often brings immediate relief. Many clients contact us because they are afraid to answer IRS calls or do not understand the notices they are receiving. Once we step in, that burden is lifted.

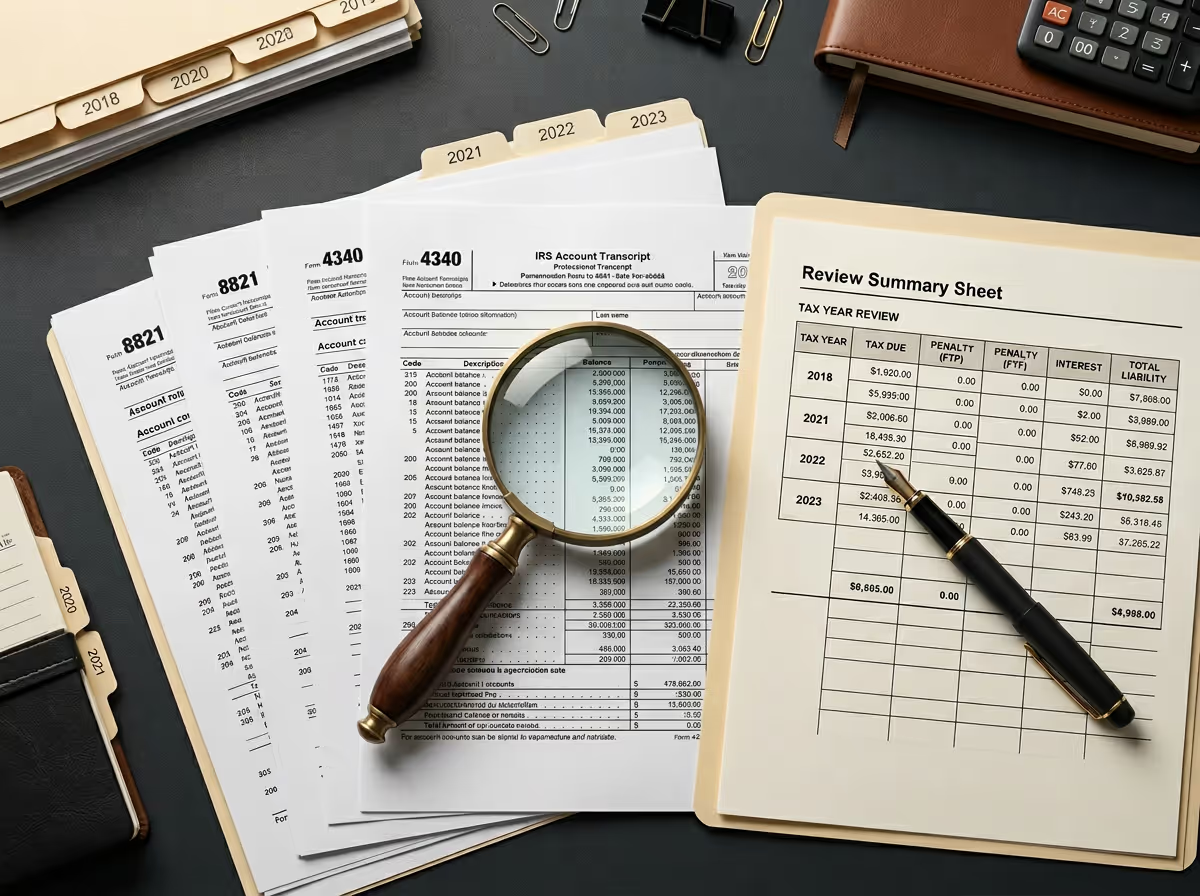

Complete IRS Account Review

We obtain your IRS account records and tax transcripts to understand precisely where your case stands and what actions the IRS may already be taking.

We confirm the accuracy of the IRS balance and identify any issues that may affect your eligibility for your payment plan. In some cases, balances include penalties that may qualify for reduction or assessments that should be challenged.

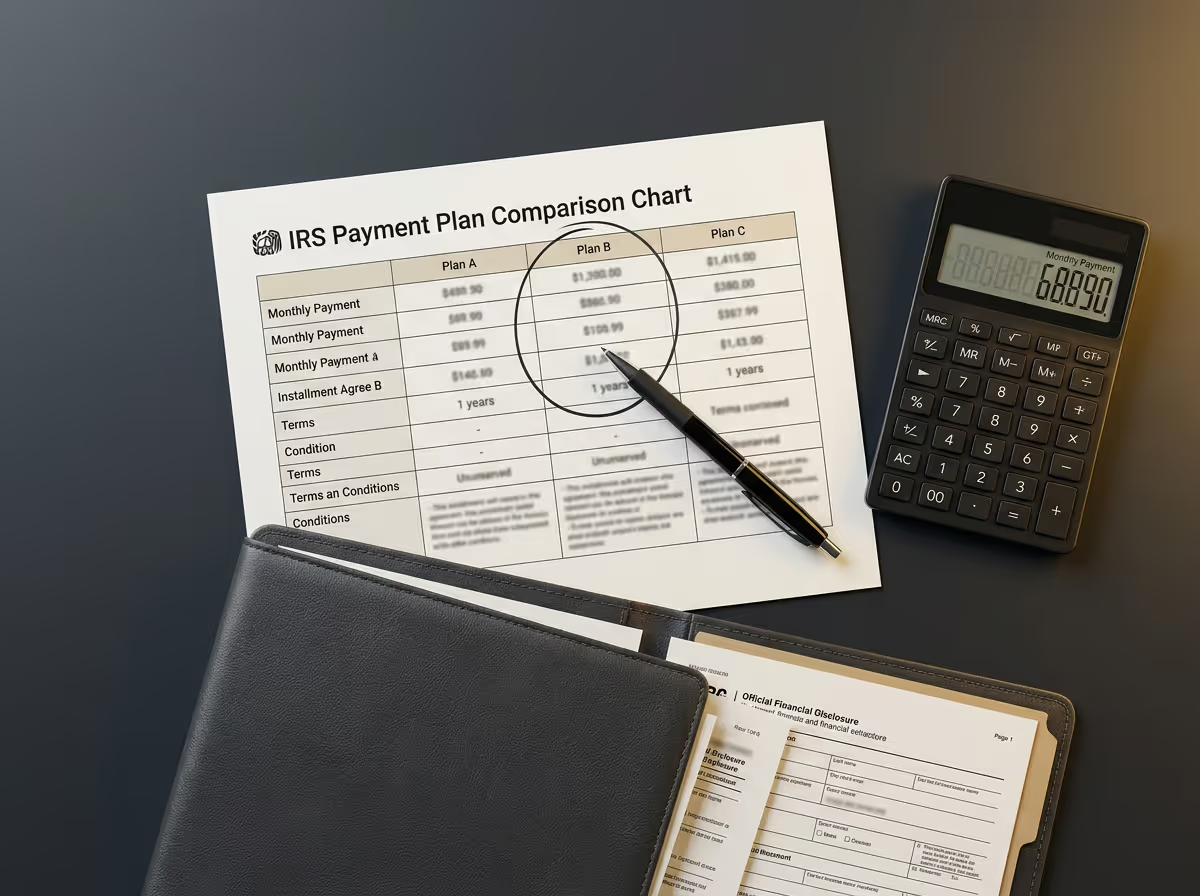

Determining the Right IRS Payment Plan

The IRS offers several types of payment plans, also known as installment agreements, each of which applies to different financial circumstances and compliance situations.

Although the IRS offers an Online Payment Agreement tool, many taxpayers are rejected or approved for unaffordable terms because eligibility rules and financial disclosure requirements are misunderstood. We review your situation carefully before submitting anything to avoid costly mistakes and unnecessary enforcement.

Preparing and Submitting Required Forms

Depending on your case, we prepare and submit all required IRS forms, including:

These forms determine what the IRS believes you can afford. We prepare them carefully to ensure allowable expenses are appropriately documented, and your ability to pay is not overstated.

Negotiation and Ongoing Communication

Once your application is submitted:

If the IRS initially rejects a proposal or requests additional information, we respond and continue negotiations rather than allowing enforcement to resume.

Why This Gets Worse Without Help

IRS tax problems do not resolve themselves. Waiting almost always makes the situation worse.

- The IRS interprets silence as a refusal to cooperate.

- Collection actions escalate automatically.

- Penalties and interest continue to accrue every month.

- Monthly penalties increase the balance due.

- Negotiation options shrink once enforcement begins.

Many people attempt to use the Online Payment Agreement tool or call the IRS directly without understanding filing requirements, financial disclosure rules, or estimated tax obligations. These attempts often result in rejection or approval of unaffordable payment terms.

Once enforcement begins, stopping it becomes more difficult. Acting early preserves leverage and prevents unnecessary financial damage.

How the IRS Enforces This

The Internal Revenue Service has broad authority under the Internal Revenue Code to collect unpaid federal taxes without going to court. This authority and enforcement process are outlined on IRS.gov.

IRS Assessment and Notice Process

After a tax is assessed through a filed tax return or IRS assessment, the debt becomes legally collectible. The IRS then sends a series of notices, which typically include:

Each notice increases urgency and moves the account closer to enforcement.

IRS Collection Tools

When taxpayers do not make payment arrangements, the IRS may pursue enforcement actions to collect the outstanding balance.

According to IRS.gov, the Internal Revenue Service does not need a court order to use these collection tools.

Penalties, Interest, and the Collection Timeline

Unpaid federal taxes accrue penalties and interest until resolved. The IRS generally has ten years from the date of assessment to collect a tax debt, known as the Collection Statute Expiration Date. Specific actions, including payment plan requests, can pause or extend this period.

Who This Service Is For

You need this service if:

- You owe the IRS more than you can pay in full.

- You received a balance-due notice or a Final Notice of Intent to Levy.

- The IRS is threatening or has started wage garnishment.

- The IRS has levied or is preparing to levy your bank account.

- An IRS revenue officer contacted you.

- You tried to set up a payment plan and were rejected.

- The monthly payment the IRS demands is unaffordable.

- You have unfiled tax returns in addition to tax debt.

- You are self-employed or own a small business.

- You want professional representation before the IRS.

Common Mistakes People Make

Many taxpayers worsen their situation by making avoidable mistakes:

Our Representation Process

Our process is structured, proactive, and focused on protecting you.

Initial Case Review

We begin by reviewing the IRS notices you received, your current balance due, and any enforcement actions already in place. This allows us to understand the urgency of your situation and identify immediate risks.

Power of Attorney Filing

We prepare and file IRS Form 2848 to legally represent you before the Internal Revenue Service. Once processed, the IRS communicates with us instead of contacting you directly.

Transcript and Compliance Review

We obtain your IRS tax transcripts to confirm balances, penalties, interest, and payment history. We also verify whether all required tax returns have been filed and identify any compliance issues.

Financial Analysis and Strategy Development

We analyze your income, expenses, assets, and financial hardship to determine what you can realistically afford. Based on this analysis, we select the most appropriate IRS payment plan option.

Application Preparation and Submission

We prepare and submit all required IRS forms, including payment plan and financial disclosure documents. Each submission is reviewed carefully to reduce the risk of rejection or delay.

IRS Negotiation and Follow-Up

We handle all communication with the IRS while your application is under review. If the IRS requests additional information or proposes different terms, we respond and negotiate on your behalf.

Approval and Compliance Guidance

Once the IRS approves the payment plan, we explain the terms, monthly payment requirements, and compliance rules. We help you understand how to stay in good standing and avoid default.

What Happens If You Do Nothing

Final notices may be issued, levy authority can become active, and a federal tax lien may be filed.

Bank levies and wage garnishments often begin, and funds or income may be seized.

Financial disruption may escalate, and credit damage can increase as enforcement continues.

Frequently Asked Questions (FAQs)

Take Action Now

The IRS will not wait. Penalties and interest will continue. Enforcement will move forward.

We step in, take control, and deal with the IRS for you. The sooner you contact us, the more options we have to protect your income and assets.