Defaulted IRS Payment Plans | Immediate Relief

We assist with tax payment plans by reviewing payment history, preparing a Collection Information Statement using Form 433 or Form 433-F, and evaluating payment options. Acting under the power of attorney, we work to reinstate installment agreements, pursue an offer in compromise or currently not collectible status, and reduce collection actions.

What This Service Does

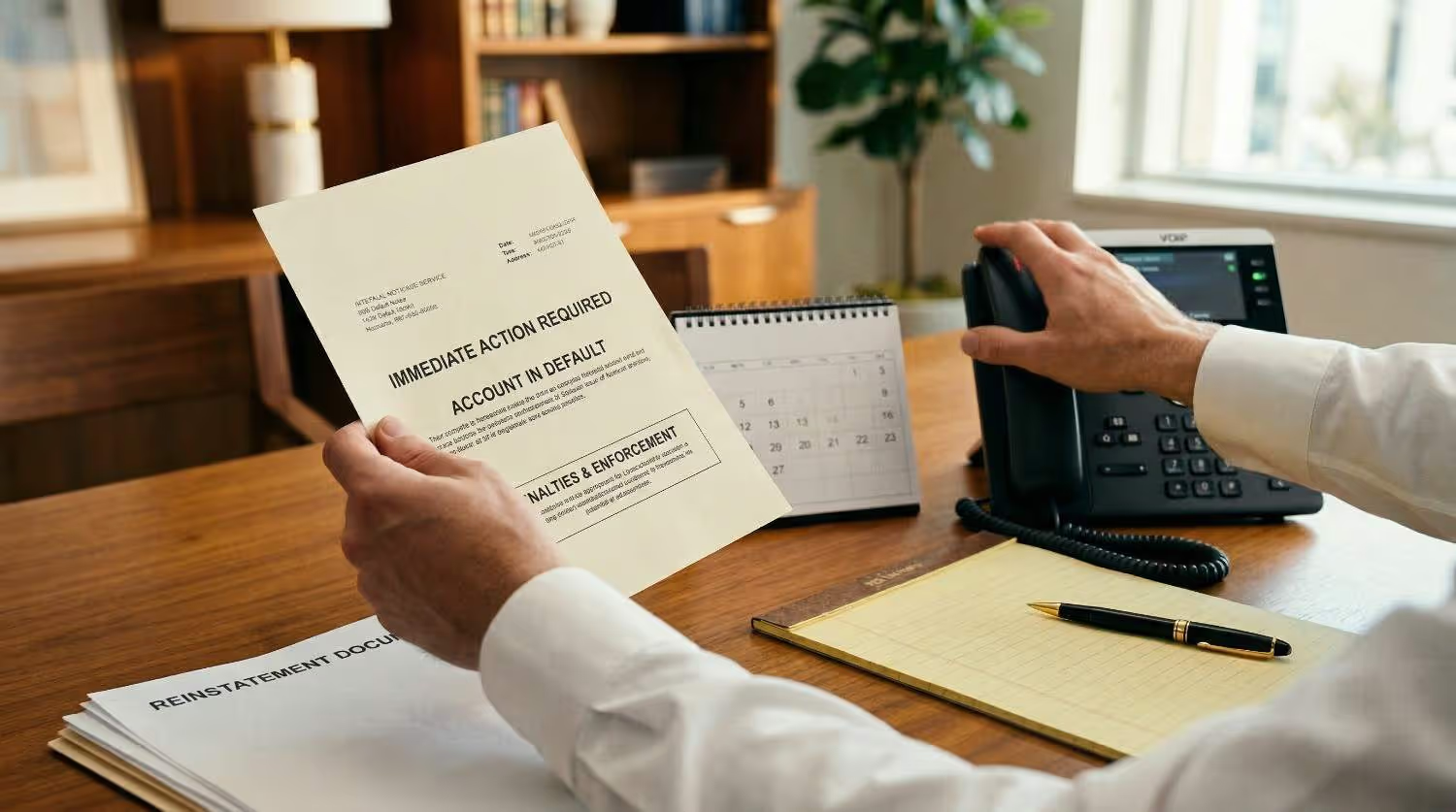

When an IRS installment agreement defaults, the issue is not simply catching up on a missed payment. It is about reestablishing your protected status and preventing escalation. We design our Defaulted IRS Payment Plans service to address both compliance and enforcement risks simultaneously.

We Step In as Your Authorized Representative

Once you retain us, we prepare and file IRS Form 2848, a power of attorney. The IRS explains that Form 2848 authorizes an eligible representative to act on your behalf before the agency. After it is accepted, we speak directly with the IRS so you do not have to manage stressful calls or interpret complex notices on your own. We control the communication and ensure consistent messaging.

We Conduct a Full IRS Account Review

A payment plan can default for several reasons. We obtain your IRS transcripts and confirm the official cause of the termination. We verify whether the issue involves missed payments, failed direct debit drafts, unfiled returns, or new tax debt added after the agreement began. This analysis prevents guesswork and ensures we correct the real problem.

We Address Compliance Gaps Immediately

The IRS generally requires full compliance with filing requirements before reinstating or modifying an agreement. If you have missing returns or newly assessed balances, we work with you to correct them. Restoring compliance is often the key to reopening negotiations and stopping enforcement from expanding.

We Stabilize Enforcement Risk

According to IRS.gov, a levy is a legal seizure of property to satisfy a tax debt and may include wage garnishment or the withdrawal of funds from bank accounts. Once a payment plan defaults, the exposure to levies increases. We act quickly to reduce the risk of lien filings and levies while pursuing reinstatement or alternative arrangements.

We Negotiate Sustainable Terms

If reinstatement is possible, we pursue it. If your financial situation has changed, we can negotiate revised payment terms that reflect your current cash flow. The IRS explains that payment plans allow taxpayers to pay over time, but penalties and interest continue until the balance is paid in full. Our goal is to secure a plan you can realistically maintain so you do not default again.

We Monitor and Guide You Forward

Resolution does not end with a new agreement. We provide ongoing guidance so you stay compliant with filing and payment requirements. Preventing repeat defaults is part of protecting your long-term financial stability.

Why This Gets Worse Without Help

A defaulted installment agreement shifts your case back into the IRS collection system. Delaying action can increase both financial cost and enforcement risk.

Enforcement Activity Can Resume

The IRS explains that the collection process begins after a bill is sent and continues until the account is satisfied or the IRS can no longer legally collect. Without an active agreement in place, your account may proceed with that process.

Notices Escalate in Urgency

IRS notices typically become more serious over time. For example, IRS Notice CP504 is described on IRS.gov as a Notice of Intent to Levy under Internal Revenue Code section 6331(d). That means the IRS is warning you that levy action may follow if the balance is not resolved.

Federal Tax Liens May Be Filed

The IRS explains that a federal tax lien is the government’s legal claim against your property when you neglect or fail to pay a tax debt. The IRS may file a Notice of Federal Tax Lien publicly to alert creditors. This filing can affect financing, credit, and business relationships.

Wage and Bank Levies Can Disrupt Income

According to IRS.gov, a levy may garnish wages, take funds from bank accounts, and seize property. If the IRS levies a bank account, the bank generally holds the funds for 21 days before sending them to the IRS. That short window is critical, and waiting reduces your ability to respond effectively.

Penalties and Interest Continue to Grow

IRS.gov explains that the failure-to-pay penalty is calculated based on how long the tax remains unpaid and can grow up to 25 percent of the unpaid tax. Interest also accrues daily. Delay increases the total balance owed.

How the IRS Enforces This

Understanding enforcement authority helps clarify why defaulted IRS payment plans require immediate attention.

The Collection Process Continues Until Resolved

The IRS states that if you do not pay your tax bill, the collection process continues until the account is satisfied, or the IRS may no longer legally collect. A defaulted agreement removes the structured framework that may have limited enforcement actions.

Notice of Intent to Levy

Before levying, the IRS generally sends a written notice. IRS Notice CP504 is described on IRS.gov as a Notice of Intent to Levy. This letter warns that the IRS may proceed with levy action if payment is not made.

Federal Tax Liens

A federal tax lien arises after assessment, notice, and failure to pay. IRS.gov explains that the IRS may file a Notice of Federal Tax Lien to alert creditors. Once filed, the lien attaches to your property and your rights to it.

Wage Garnishment

The IRS explains that a levy may include wage garnishment. This means a portion of your paycheck can be sent directly to the IRS each pay period until the balance is resolved or alternative arrangements are made.

Bank Levies and the 21-Day Holding Period

IRS.gov explains that when the IRS levies a bank account, the bank must generally hold the funds for 21 days before sending them to the IRS. This waiting period allows time to contact the IRS or address errors. Acting quickly during this window is critical.

Installment Agreement Protections

IRS.gov explains that when you request an installment agreement, with certain exceptions, the IRS is generally prohibited from levying while the request is pending and typically will not take enforced collection while a plan is in effect, for 30 days after rejection or termination, or during an appeal. Restoring this status can significantly reduce enforcement pressure.

Who This Service Is For

- Missed installment payments: You need this if you missed one or more IRS payments and received a default or termination notice warning that your agreement may be canceled.

- Failed direct debit arrangements: You need this if your automatic bank draft failed due to account changes, insufficient funds, or banking errors that caused the IRS to terminate your agreement.

- New tax debt added to your account: You need this if you incurred new balances after your payment plan started, and the IRS defaulted your agreement because you were no longer compliant.

- Levy or lien warnings: You need this if you received Notice CP504 or other letters warning of levy action or federal tax lien filing.

- Small business cash flow changes: You need this if your business revenue has dropped and the existing payment amount is no longer realistic, increasing the risk of repeated defaults.

- Fear of wage or bank levies: You need this notification if you are concerned that the IRS may garnish your wages or levy your bank account due to the defaulted agreement.

Common Mistakes People Make

Many taxpayers worsen their situation by making avoidable mistakes:

Our Representation Process

Initial Case Review

We begin with a detailed review of your IRS notices, account status, and timeline. This allows us to determine how far the collection process has progressed and whether levy or lien actions are pending. By identifying enforcement risks early, we can prioritize urgent issues and develop a strategy designed to stabilize your account as quickly as possible.

Power of Attorney Authorization

We prepare and file IRS Form 2848, a power of attorney, to legally represent you before the IRS. Once the IRS processes this authorization, we will communicate directly with the agency on your behalf. This shifts the IRS contact away from you and ensures that all discussions, documentation, and negotiations are handled professionally and consistently.

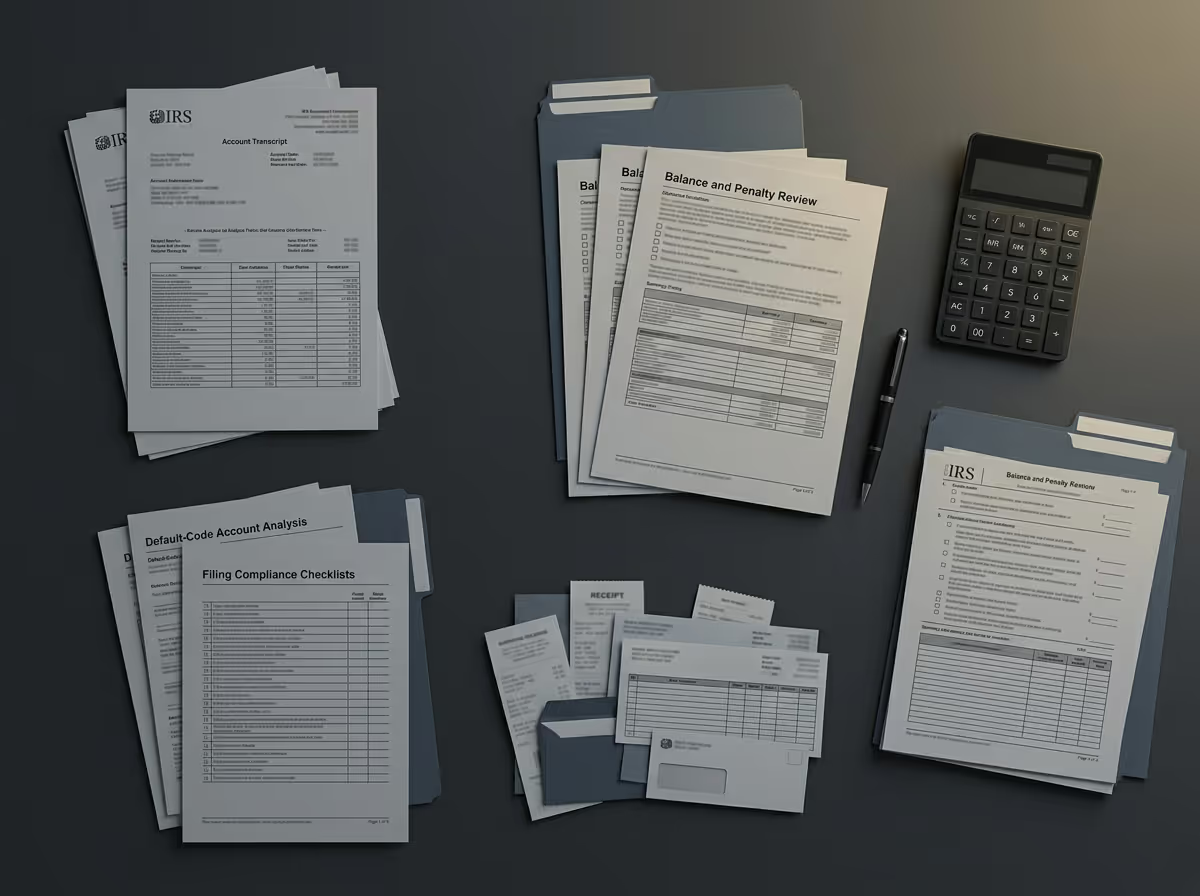

IRS Transcript and Account Analysis

Once authorization is granted, we will obtain your IRS account transcripts to confirm balances, penalty assessments, default codes, and enforcement indicators. We verify the exact reason the installment agreement was terminated and whether any additional compliance issues exist. This step prevents assumptions and ensures that our negotiation strategy is based on accurate, complete IRS records.

Compliance Correction and Documentation

If missing tax returns, new balances, or documentation gaps caused the default, we work with you to resolve them promptly. The IRS generally requires full compliance with filing requirements before reinstating or modifying an agreement. By resolving compliance problems early, we remove barriers that could delay reinstatement and reduce the likelihood of another termination.

Enforcement Risk Management

If your account shows levy warnings or lien indicators, we act quickly to address those risks. This may involve immediate communication with the IRS to clarify status, request holds where appropriate, and position your case for reinstatement or review. Timing is critical when enforcement actions are approaching, and early intervention can prevent significant financial disruption.

Negotiation for Reinstatement or Revised Terms

Once we restore compliance and address enforcement risks, we strive to reinstate your prior installment agreement whenever possible. If your financial circumstances have changed, we negotiate revised terms that reflect your actual ability to pay. Our goal is to secure a sustainable arrangement that reduces the risk of future defaults and enforcement.

Ongoing Monitoring and Compliance Guidance

Our work continues even after we secure a new agreement. We provide guidance on staying current with filing and payment obligations to prevent future problems. Ongoing compliance is critical because new tax debt or missed returns can trigger another default. We help you understand the requirements so you can maintain stability moving forward.

What Happens If You Do Nothing

Escalating collection notices: You may receive additional letters warning of levy action and increasing urgency.

Notice of Intent to Levy: IRS Notice CP504 may be issued, warning that the IRS intends to levy if payment is not made.

Reduced flexibility: Early opportunities to resolve the issue voluntarily may begin to narrow.

Federal tax lien filing: The IRS may file a Notice of Federal Tax Lien, creating a public record of the government’s legal claim.

Credit and financing impact: A filed lien can affect borrowing ability and business relationships.

Increased enforcement preparation: Your account may be reviewed for potential levy action.

Wage garnishment risk: The IRS may begin a wage levy, redirecting a portion of your paycheck.

Bank levy action: Funds in your bank account may be frozen and held for 21 days before being sent to the IRS.

Ongoing penalties and interest: Your balance continues to grow, making resolution more expensive over time.

Frequently Asked Questions (FAQs)

Take Action Now

A defaulted IRS payment plan is a serious turning point. The longer you wait, the greater the risk of liens, levies, and growing balances. Early intervention preserves options and reduces enforcement pressure.

We handle communication with the IRS, correct compliance issues, and negotiate realistic terms designed to prevent repeat defaults. If you received a default notice, levy warning, or lien notice, contact us now. Taking action today can prevent forced collection tomorrow.

Results depend on individual circumstances and IRS determinations. No outcome is guaranteed. Representation is subject to IRS rules and procedures. IRS Circular 230 Disclosure applies.