Thank you for contacting

GetTaxReliefNow.com!

or wage garnishment — call us now at +(888) 260 9441 for immediate help.

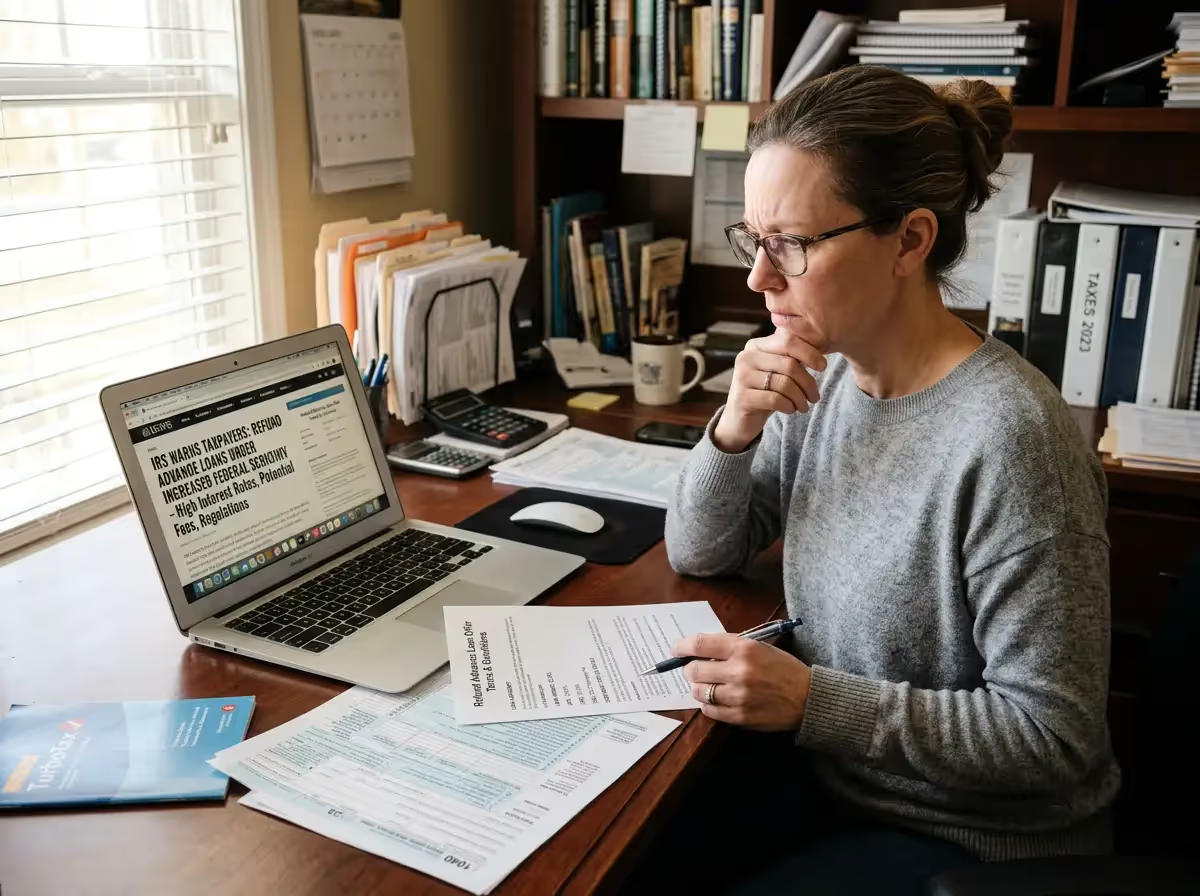

Refund Advance Loans Draw New Federal Scrutiny

Federal regulators are warning taxpayers to look closely at refund advance loans as aggressive marketing returns for the 2026 filing season. Consumer agencies say these fast-cash offers may carry hidden costs and risks, especially for filers expecting delayed IRS refunds tied to credits like the EITC and ACTC. The renewed attention reflects growing concern about how these products are presented to the public.

Regulators Warn on Rising Use of Refund Advances

Federal oversight agencies have stepped up warnings as tax refund anticipation loans and similar products reappear across the industry. These offers promise quick access to an IRS refund, often within minutes of filing, but regulators say the terms can be misleading and may not clearly explain total costs.

The Consumer Financial Protection Bureau has urged taxpayers to review fees, repayment terms, and total costs associated with refund-advance products before signing any agreement. The Federal Trade Commission has also issued alerts about tax-related financial offers that may obscure repayment obligations or present incomplete information.

Industry data shows that refund-advance loans—sometimes marketed as same-day tax advances—are being promoted more aggressively as average tax refunds rise. That trend, combined with refund delays linked to federal rules, has created a favorable environment for lenders targeting taxpayers seeking immediate cash access.

How Refund Advance Loans Work and Who Pays the Cost

Refund advance loans are structured as short-term borrowing against an expected tax refund. When a taxpayer files a return, a preparer estimates the refund. It offers an advance, which may be deposited into a bank account, a prepaid debit card, or a temporary account controlled by the provider.

Repayment is automatic once the IRS issues the refund. The lender deducts the loan amount and releases any remaining balance to the taxpayer. However, complications arise when the refund is lower than expected due to adjustments, processing delays, or offsets for outstanding debts.

Consumer advocates note that while some providers advertise 0% interest, the actual cost often appears through tax preparation fees, administrative charges, or prepaid debit card fees. When combined, these costs can result in very high effective annual percentage rates for traditional tax refund anticipation loans.

IRS Policy Changes and PATH Act Delays Drive Demand

Several policy changes in the 2026 filing season have increased demand for refund advance products. The IRS continues to enforce the PATH Act, which requires the agency to hold refunds that include the Earned Income Tax Credit or Additional Child Tax Credit until at least mid-February.

For many taxpayers, especially those relying on EITC refunds, that delay extends into early March. At the same time, new federal rules are pushing most filers toward direct deposit, reducing reliance on paper checks and increasing the need for accurate banking information.

Tax professionals note that while these delays can create short-term financial pressure, the IRS still processes most e-filed returns with direct deposit within about three weeks. That timeline often makes refund advance loans unnecessary for taxpayers who can wait.

Lower-Income Filers Face Higher Exposure

Lower-income taxpayers are more likely to use refund advance loans, particularly those claiming refundable credits. These filers often depend on their federal tax refund as a major annual source of income and may feel pressure to access funds quickly.

Because they face longer refund delays under PATH Act rules, they are also a key target for refund advance marketing. Financial constraints may lead them to accept loan terms without fully understanding the long-term cost.

For individuals without traditional banking access, prepaid debit cards used for refund advances can add another layer of expense. These cards may include fees for ATM withdrawals, monthly maintenance, or transactions outside a provider’s network.

Refund Offsets Add Another Layer of Risk

Refund offsets can further complicate repayment. If a taxpayer owes back child support, federal student loans, or certain state debts, the IRS may reduce the refund before it is issued through its offset program.

When that happens, the advance loan does not adjust automatically. Borrowers remain responsible for the full loan amount, even if the refund is reduced or delayed. This can create unexpected financial strain at a time when funds are already limited.

Free Filing Options Offer Safer Alternatives

Federal agencies emphasize that most taxpayers have access to lower-cost or no-cost alternatives. Filing electronically and selecting direct deposit remains the fastest way to receive a federal tax refund without additional fees or borrowing.

Programs such as IRS Free File and Volunteer Income Tax Assistance allow eligible taxpayers to prepare and file returns at no cost. These services reduce reliance on paid tax preparation and, in many cases, eliminate the need for refund advance loans.

Taxpayers can also track their refund status using official IRS tools, including the Where’s My Refund portal. These tools provide updates on processing timelines and help taxpayers plan without relying on high-cost financial products.

Experts Urge Careful Review Before Accepting Offers

Financial experts advise taxpayers to review all terms before agreeing to any refund advance. Important questions include the total cost of tax preparation, fees tied to prepaid debit cards, and repayment obligations if the refund amount changes.

Experts also recommend comparing alternatives, including waiting for the IRS refund or using free filing programs. In many cases, the cost of borrowing against a refund outweighs the benefit of early access.

Consumer protection agencies emphasize that the IRS does not issue refund advance loans, and one should not confuse them with official tax refund processes. They are private financial products that require careful evaluation before acceptance.

Source Links

- CFPB tax refund products handout

- FTC alert on tax refund scams and misleading offers

- IRS 2026 filing season announcement and refund timelines

By William Mc Lee, Editor-in-Chief & Tax Expert—Get Tax Relief Now

If you need help with a tax issue discussed in this article, you can reach a licensed tax professional at Get Tax Relief Now at (888) 260-9441 or visit our contact page.

Thank you for submitting!

Start My Confidential, No-Judgment Case Review

Ready to stop penalties and garnishments? Complete the form or call/email us directly—our experts are standing by to assist.

Have a question?

+ (888) 260 9441Write email

info@gettaxreliefnow.comAddress