Penalty Abatement Services | Immediate Relief

We provide penalty abatement services by submitting a penalty abatement request using Form 843 and supporting claims under reasonable cause or first-time penalty abatement. Acting under the power of attorney, we pursue penalty relief programs, protect taxpayer rights, and coordinate options such as installment agreements or offers in compromise when appropriate.

What This Service Does

Penalty abatement is the formal process of requesting the IRS to reduce or remove certain penalties when you qualify under IRS rules. The IRS explains that administrative relief may be available for taxpayers who meet specific criteria, including first-time abatement and reasonable cause relief.

Our role is to manage this process properly, present your case clearly, and align penalty relief with your overall IRS resolution strategy.

We Represent You Before The IRS Under The Power Of Attorney

Once you sign IRS Form 2848, power of attorney, we are authorized to speak directly with the IRS on your behalf. This allows us to request transcripts, confirm penalty assessments, discuss enforcement status, and respond to notices without you having to handle those communications yourself.

Authorized representatives can receive account information and advocate for taxpayers. We use that authority to control the flow of information, ensure accuracy, and prevent miscommunication that could weaken your case.

We Conduct A Detailed Penalty And Transcript Review

We obtain and analyze your IRS account transcripts to determine exactly what penalties were assessed, for which tax periods, and under what authority. The IRS outlines penalty structures for common penalties such as failure-to-file, failure-to-pay, failure-to-deposit, and accuracy-related penalties.

Our analysis includes verifying calculation accuracy, confirming whether penalties were applied correctly, and identifying whether administrative relief options are available based on your compliance history.

We Determine The Appropriate Relief Path

The IRS provides multiple relief options. We evaluate your situation and determine whether you may qualify for first-time abatement, reasonable cause relief, or statutory exception relief.

We select the relief path that aligns with IRS criteria and your documented facts. This ensures that the request matches the rules that the IRS applies during review.

We Prepare And Submit A Structured Request

Penalty abatement may be requested by phone, written correspondence, or by filing Form 843, a claim for refund, or asking for abatement. We determine which submission method is appropriate for your case.

We prepare a clear, organized request supported by documentation. If reasonable cause is claimed, we provide a factual timeline and evidence that aligns with IRS guidance. If first-time abatement applies, we confirm eligibility before requesting relief.

We Coordinate Penalty Relief With The Collection Strategy

Penalty abatement is often one part of a larger IRS resolution plan. Unpaid balances may lead to liens and levies if unresolved.

We align penalty relief with installment agreement planning, compliance correction, and enforcement defense so that your case is stabilized while relief is being pursued.

Why This Gets Worse Without Help

IRS penalties rarely remain static. Delays increase both financial and enforcement risk.

Penalties Continue To Accrue Monthly

Failure-to-file and failure-to-pay penalties accrue monthly up to statutory caps. As long as returns remain unfiled or balances remain unpaid, the penalties continue increasing.

Interest Accrues On Tax And Certain Penalties

Interest is charged on unpaid tax and on certain penalties until the balance is paid in full. Even if you intend to address the issue later, interest does not pause automatically.

Collection Action May Escalate

If a taxpayer fails to pay after notice and demand, the IRS may file a notice of federal tax lien or issue a levy. Penalties contribute to the total balance that drives enforcement risk.

Missed Deadlines May Limit Your Rights

Collection due process rights include hearing deadlines. If you fail to respond within the specified period, your appeal options may be reduced.

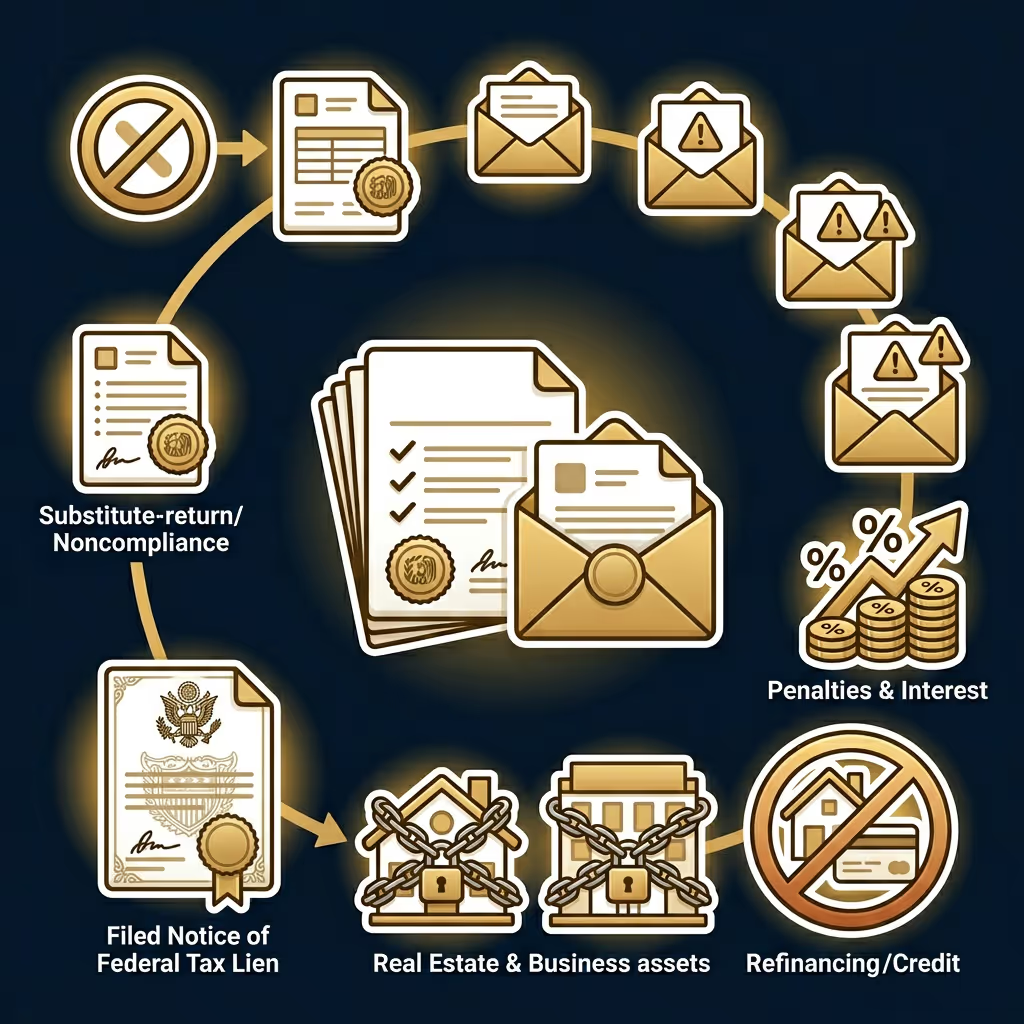

How the IRS Enforces This

The Internal Revenue Service has broad authority under federal tax laws to assess penalties, charge interest, and collect unpaid tax liability. When tax obligations are not met, the IRS follows a structured enforcement process. Understanding how enforcement works is important because IRS penalty abatement is often most effective before collection action escalates.

Notice And Demand For Payment

The enforcement process generally begins after a tax return is filed and a balance is assessed, or when the IRS prepares a substitute return due to tax noncompliance. The IRS issues a notice and demand for payment outlining the tax liability, delinquency penalties, and interest charges. If the balance is not resolved, additional notices follow, increasing urgency and warning of possible collection action.

Federal Tax Lien

If a taxpayer neglects or fails to pay after notice and demand, a federal tax lien may arise by operation of law. The IRS may file a notice of federal tax lien in public records to protect the government’s interest. This lien attaches to property and rights to property, including real estate and business assets, and can affect credit, refinancing, and financial transactions.

Levy Authority

A levy differs from a lien because it involves the actual seizure of property or property rights. The IRS may levy wages, bank accounts, Social Security benefits, and certain business receivables if the balance remains unpaid. Wage levies can continue each pay period until released, and bank levies can freeze available funds, creating immediate financial pressure.

Collection Due Process Rights

Before certain levy actions occur, the IRS must issue a final notice of intent to levy and provide an opportunity for a collection due process hearing. Strict deadlines apply for requesting this hearing. Failing to respond within the required timeframe may limit appeal rights and reduce available options to challenge enforcement actions.

Ongoing Interest And Escalation

Even while enforcement actions are pending, interest continues to accrue on unpaid tax and certain penalties under the IRS tax code. As the balance grows, enforcement pressure can increase. Addressing penalties, restoring tax compliance, and implementing a structured tax resolution strategy early can significantly reduce long-term financial exposure.

Who This Service Is For

- You need this service if you have received an IRS notice showing failure-to-file or failure-to-pay penalties, and the balance continues to increase each month.

- You need this service if your business has been assessed failure-to-deposit penalties and is under cash flow pressure.

- You need this service if you have been compliant in prior years and believe you qualify for administrative first-time penalty relief.

- You need this service if illness, disaster, records loss, or other serious events prevent timely compliance and may support reasonable cause relief.

- You need this service if you are entering a payment plan and want penalties addressed before long-term payments begin.

- You need this service if you are concerned that the IRS may file a federal tax lien or issue a levy due to the growing balance.

Common Mistakes People Make

- Many taxpayers contact the IRS without prepared transcripts or documentation, which can result in incomplete explanations that weaken later relief requests.

- Taxpayers sometimes fail to file, which can block certain relief options until all required returns are submitted.

- Many individuals focus only on penalties and overlook interest and the underlying tax balance, which still must be resolved.

- Some taxpayers miss appeal deadlines on enforcement notices, which can reduce their ability to challenge liens or levies.

- Others wait and hope the issue will resolve, even though enforcement can continue aggressively before any collection statute expires.

Our Representation Process

Initial Case Evaluation And Tax Analysis

We begin with a detailed review of your IRS notices, tax transcripts, and affected tax years to understand the full scope of your tax liability. This tax analysis allows us to identify delinquency penalties, interest exposure, and enforcement risk with the Internal Revenue Service. We evaluate whether your situation involves reasonable cause factors such as natural disasters, serious illness, or other compliance disruptions under applicable tax laws and regulations.

Power Of Attorney And Direct IRS Communication

After you authorize us through Form 2848, we formally step in as your representative before the Internal Revenue Service. This allows us to request account records, confirm penalty calculations, and manage all communication related to your IRS penalty abatement request. By centralizing contact through a tax professional, we reduce confusion, prevent inconsistent statements, and ensure your case proceeds in accordance with IRS tax code procedures.

Compliance Review And Correction Of Tax Noncompliance

Before requesting IRS penalty abatement, we verify that all required tax returns have been filed and that current tax obligations are being met. If there are missing returns, including partnership returns or prior-year filings, we create a compliance plan to address them. The IRS typically expects full tax compliance before granting penalty relief, so addressing outstanding filing or payment gaps is a critical step in the process.

Penalty Relief Strategy Selection

We determine whether your case qualifies for first-time IRS tax penalty abatement, reasonable cause abatement, or statutory exception abatement under IRS guidelines. If circumstances such as medical illness, financial hardship, or reliance on a tax professional contributed to the issue, we evaluate how those facts align with IRS standards. Our goal is to match your documented situation to the correct relief category for the strongest possible penalty relief decision.

Compliance Review And Correction Of Tax Noncompliance

Before requesting IRS penalty abatement, we verify that all required tax returns have been filed and that current tax obligations are being met. If there are missing returns, including partnership returns or prior-year filings, we create a compliance plan to address them. The IRS typically expects full tax compliance before granting penalty relief, so addressing outstanding filing or payment gaps is a critical step in the process.

Penalty Relief Strategy Selection

We determine whether your case qualifies for first-time IRS tax penalty abatement, reasonable cause abatement, or statutory exception abatement under IRS guidelines. If circumstances such as medical illness, financial hardship, or reliance on a tax professional contributed to the issue, we evaluate how those facts align with IRS standards. Our goal is to match your documented situation to the correct relief category for the strongest possible penalty relief decision.

Integration With Long-Term Tax Resolution Planning

Penalty abatement is often one part of a larger tax resolution strategy. Once penalties are addressed, we coordinate next steps, such as installment agreements, interest relief, or other structured tax debt relief options. Our focus is to stabilize your overall tax liability, maintain compliance with federal tax requirements, and reduce the risk of future tax controversy issues with the Internal Revenue Service.

What Happens If You Do Nothing

Penalties and interest continue to accrue under IRS rules, increasing the total balance owed.

Additional IRS notices may be issued requesting payment or warning of further action.

Deadlines for certain response rights may begin running, limiting options if ignored.

The account may move closer to lien filing as part of the collection process.

Enforcement risk increases if the balance remains unpaid and unresolved.

Appeal rights may narrow depending on the stage of the notice cycle.

The IRS may issue or prepare to issue a levy action against wages or bank accounts.

A notice of federal tax lien may be filed publicly, affecting credit and financial transactions.

Resolution becomes more complex and urgent as enforcement tools become active.

Frequently Asked Questions (FAQs)

Take Action Now

IRS penalties grow with time—interest compounds. Enforcement risk increases as balances rise. Acting early provides more options and greater control.

We take over communication, draft a structured relief request, coordinate a comprehensive resolution strategy, design a plan to reduce penalties, and manage your IRS account.

Call us now so we can review your notices and begin protecting your rights.

Results depend on individual circumstances and IRS determinations. No outcome is guaranteed. Representation is subject to IRS rules and procedures. IRS Circular 230 Disclosure applies.