IRS Bank Levy Help |

Immediate Relief

We assist individuals facing bank account levies by requesting a levy release within the 21-day window and addressing economic hardship. Our team works to resolve your tax debts through options like an installment agreement, payment plan, or offer in compromise while protecting your financial account from further enforced collection.

What This Service Does

When you retain our firm, we provide immediate representation designed to stop the seizure, stabilize your finances, and resolve the underlying tax issue.

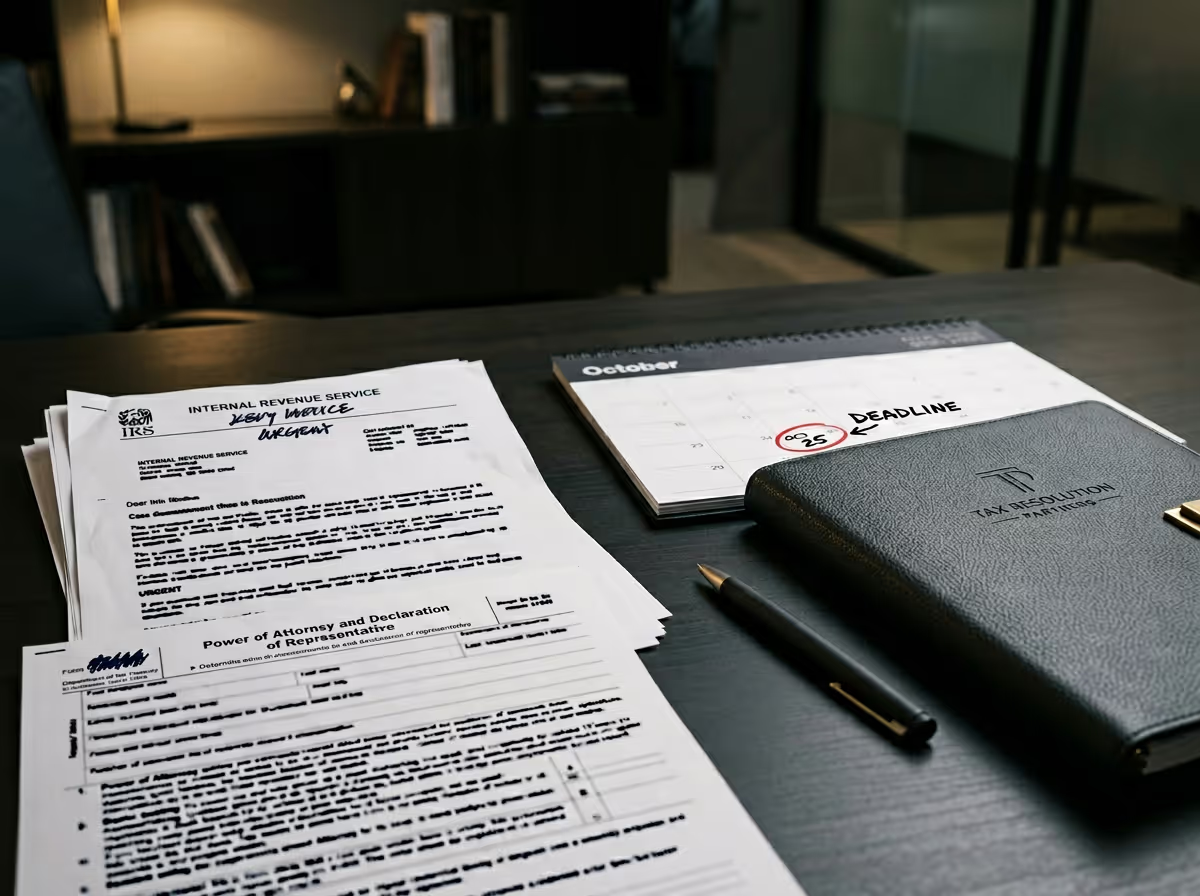

Power of Attorney Filing: We prepare and file IRS Form 2848 to legally represent you. Once on file, the IRS communicates directly with us about your case. This removes the burden of stressful collection calls and gives you professional advocacy immediately.

Direct Contact With Collections: We contact the appropriate IRS collection division, whether the Automated Collection System or an assigned revenue officer. We notify them that you are represented and begin discussions regarding the release of the levy and enforcement holds.

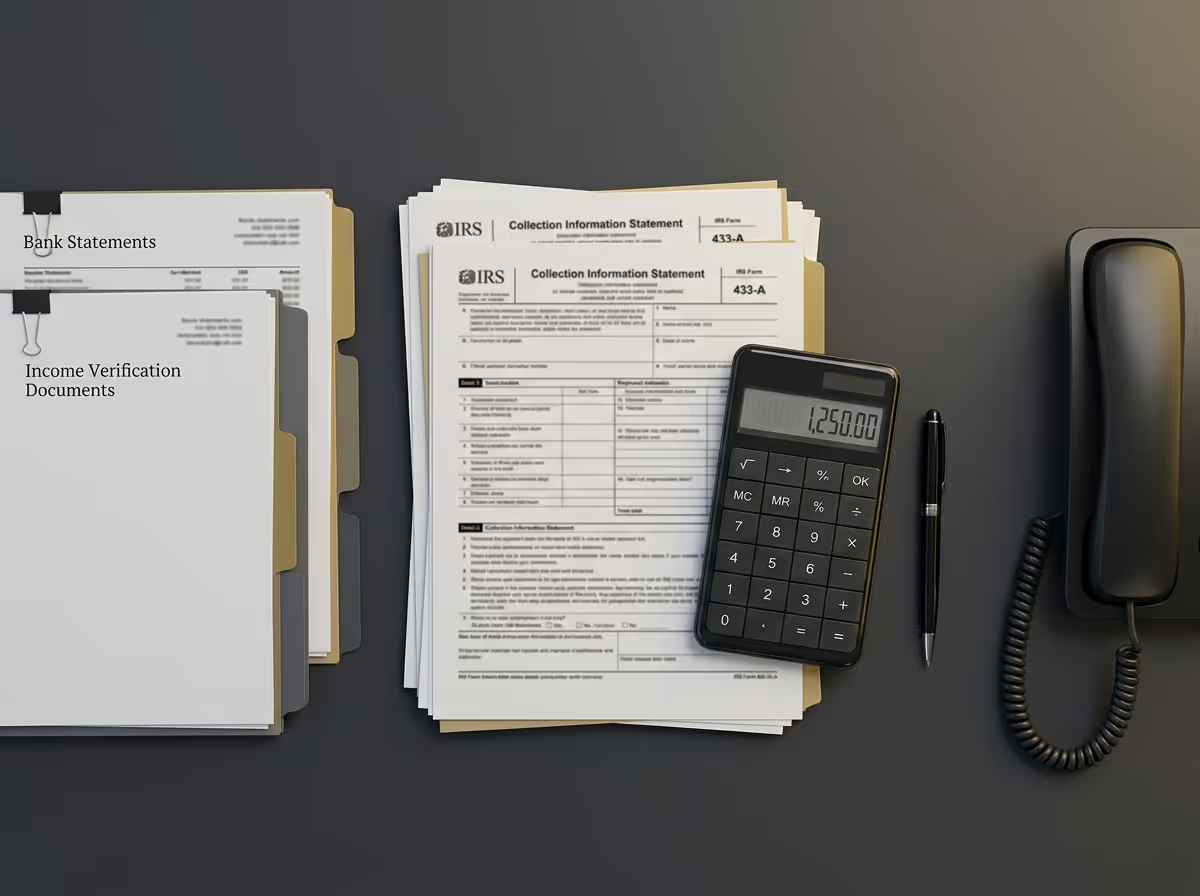

Economic Hardship Documentation: IRS.gov explains that the IRS must release a levy if it is causing immediate financial hardship. We prepare Form 433-A and supporting documentation to demonstrate that the levy prevents you from paying necessary living expenses.

21-Day Hold Intervention: Banks must hold levied funds for 21 days before transferring them to the IRS. During this period, we intervene and demand the release of the funds before they are assigned. Acting early significantly increases your chances of keeping your money.

Transcript Review and Balance Verification: We obtain your IRS transcripts to confirm assessments, penalties, interest, and collection timelines. We review whether the IRS followed proper notice procedures before levying.

Resolution Planning: We determine whether an installment agreement, Currently Not Collectible status, Offer in Compromise, or penalty abatement may apply. Stopping one levy without addressing the root issue invites repeat enforcement.

Structured Payment Negotiation: If payment is possible, we negotiate terms you can realistically afford. Sustainable agreements help prevent default and renewed levy action.

Compliance Monitoring: We guide you on filing requirements and current tax obligations so you remain protected from future enforcement.

Why This Gets Worse Without Help

You usually receive earlier notices before an IRS bank levy. It is typically the result of escalating enforcement. Without professional representation, the situation often deteriorates quickly.

- Short Timeframe to Act: The 21-day bank holding period passes quickly. If no action is taken, funds are permanently transferred to the IRS.

- Repeat Bank Levies: A bank levy captures funds on deposit at the time it is levied. However, the IRS may issue additional levies against future deposits if the debt remains unresolved.

- Wage Garnishment Risk: IRS.gov explains that wage levies continue each pay period until released. Unlike a one-time bank levy, wage garnishment is ongoing.

- Growing Balance: Penalties and interest continue to accrue monthly, increasing your total debt.

- Reduced Negotiating Position: Once enforcement is successful, the IRS may be less flexible unless a structured, well-documented resolution plan is presented.

Delay almost always increases financial damage.

How the IRS Enforces This

The IRS has broad authority under federal law to collect assessed tax debts. IRS.gov outlines required notice procedures and levy mechanics.

Required Notice Before Levy

Before issuing a levy, the IRS must:

Should you fail to provide a timely response, the IRS reserves the right to initiate levy action.

Bank Levy Process

This final notice gives you 30 days to request a Collection Due Process hearing before enforcement begins.

Mandatory Release Situations

According to IRS.gov, the IRS must release a levy if:

A hardship release requires detailed, accurate documentation.

Who This Service Is For

You need this service if:

- Immediate Account Freeze: You need this if your bank account is frozen and you cannot access your funds for basic living expenses.

- Within the 21-Day Window: You need this if your bank has notified you of a levy and funds are being held for 21 days.

- Repeat Levy Concerns: You need this if the IRS has levied you before and you fear additional seizures.

- Final Notice Received: You need this if you received a Final Notice of Intent to Levy, and enforcement may be imminent.

- Severe Financial Hardship: You need this if the levy prevents you from paying rent, utilities, medical expenses, or food.

- Self-Employed Impact: You need this if your operating account was levied and business operations are threatened.

- Failed DIY Attempts: You need this if you contacted the IRS on your own and were unable to secure a release.

Common Mistakes People Make

Our Representation Process

Our process is structured, proactive, and focused on protecting you.

Emergency Consultation

We initiate an immediate consultation to review the levy date, identify affected accounts, and determine whether you are within the 21-day holding period. We assess financial hardship, notice history, and enforcement risk to prioritize urgent action.

Power of Attorney Filing

We prepare and file IRS Form 2848 to obtain legal authority to represent you before the IRS. This allows us to access your account transcripts, speak directly with collections personnel, and intervene without delay.

Immediate IRS Contact

We contact the appropriate IRS collection division the same day whenever possible. We notify them that you are represented, request consideration of a levy release, and seek temporary holds on additional enforcement while documentation is prepared.

Financial Documentation Preparation

We guide you through completing Form 433-A and gathering required financial records, including income verification, monthly expenses, and bank statements. Accurate and complete documentation strengthens your hardship case and supports discussions on levy release.

Hardship Submission and Negotiation

We formally present your documented hardship to the IRS and negotiate directly with assigned personnel. We explain how the levy prevents the payment of necessary living expenses, and we push for release in accordance with the guidelines outlined on IRS.gov.

Long-Term Resolution Strategy

While pursuing levy release, we evaluate installment agreements, Currently Not Collectible status, or other relief options. Establishing a sustainable resolution prevents repeat levies and protects you from continued enforcement activity.

Compliance and Ongoing Protection

After securing relief or a resolution, we clearly explain your ongoing compliance requirements. Staying current with filings and agreed payments is essential to avoid future levies and maintain long-term financial stability.

What Happens If You Do Nothing

Funds Are Transferred: After the 21-day holding period, the bank permanently sends frozen funds to the IRS.

Financial Disruption Increases: Overdraft fees, missed payments, and late penalties accumulate quickly.

Additional Levies May Occur: The IRS may seize new deposits if the debt remains unresolved.

Wage Garnishment Risk Grows: The IRS may issue a wage levy that withholds part of every paycheck.

Severe Financial Instability: Continued levies and garnishments may make housing and utilities unaffordable.

Expanded Enforcement: The IRS may pursue other assets if compliance is not restored.

Acting early significantly improves your available options.

Frequently Asked Questions (FAQs)

Take Action Now

The clock starts ticking the moment your bank account freezes. The 21-day holding period swiftly progresses, and once you transfer funds, your options become more limited.

We promptly assist by contacting the IRS, presenting documented hardship when appropriate, and negotiating long-term protection from future levies. You do not have to handle this crisis alone.

Call now. Acting today can make the difference between recovery and continued enforcement.

Results depend on individual circumstances and IRS determinations. No outcome is guaranteed. Representation is subject to IRS rules and procedures. IRS Circular 230 Disclosure applies.