Declaraciones de impuestos comerciales no presentadas | Ayuda inmediata

Ayudamos a cumplir con la declaración de impuestos preparando impuestos comerciales precisos mediante formularios como el formulario 1120 o el formulario 1065 y obteniendo las transcripciones de impuestos a través del formulario 4506-T del IRS. Actuando en virtud de un poder notarial, organizamos los registros financieros, abordamos la posibilidad de reducir las multas y buscamos soluciones como un acuerdo de pago a plazos o un acuerdo de pago en línea para resolver la deuda tributaria.

Qué hace este servicio

Nuestro servicio de declaraciones de impuestos comerciales no presentadas es una representación estructurada ante el Servicio de Impuestos Internos. No se trata simplemente de la preparación de impuestos. Se trata de la autorización legal, la corrección del cumplimiento, la promoción de sanciones y la protección de la aplicación de la ley que se gestionan en conjunto bajo una estrategia coordinada.

Representación legal inmediata

- Presentación de un poder notarial: Preparamos y presentamos el formulario 2848 del IRS para representarlo legalmente ante el IRS. Una vez procesado, los agentes del IRS deben comunicarse con nuestra oficina en lugar de contactarlo directamente, lo que lo protege de cualquier inexactitud y reduce su estrés personal.

- Comunicación directa del IRS: Hablamos directamente con los representantes del sistema de cobro automatizado y los funcionarios de ingresos. Esto garantiza conversaciones estratégicas y documentadas que protejan sus derechos y estabilicen su exposición a la aplicación de la ley.

Diagnóstico de cumplimiento completo

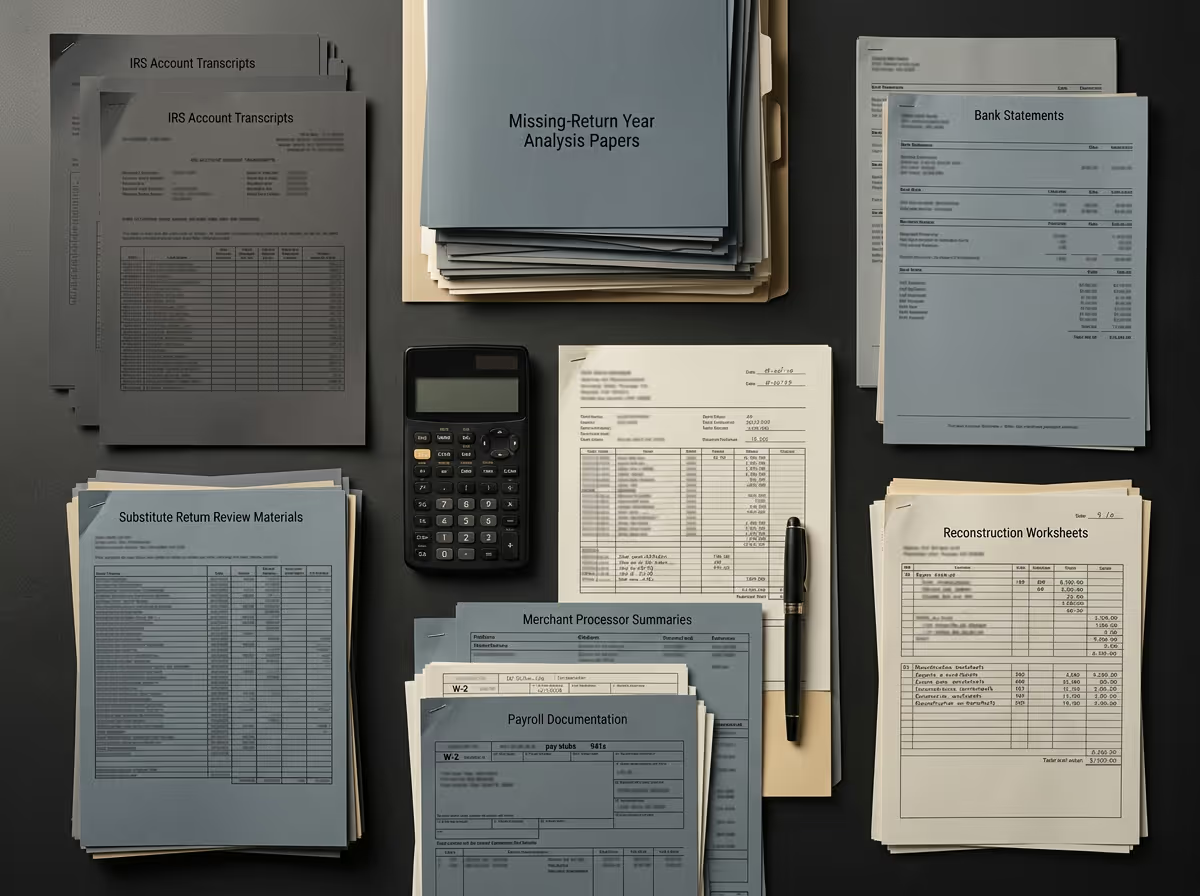

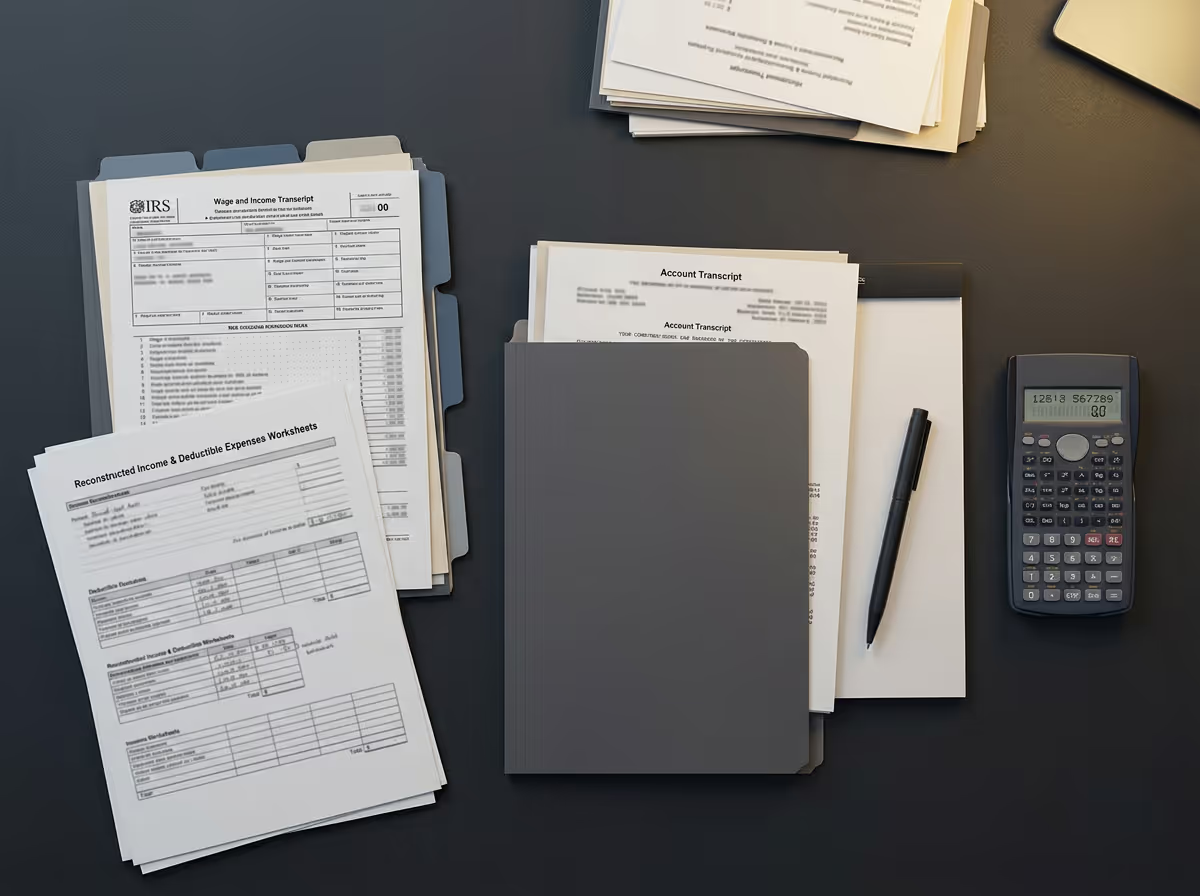

- Recuperación de transcripciones: Obtenemos las transcripciones completas de su cuenta del IRS para determinar qué declaraciones faltan, qué saldos se evalúan y si se han presentado declaraciones sustitutivas. Esto nos proporciona datos verificados directamente de los sistemas del IRS.

- Revisión de cumplimiento: Identificamos si los embargos, gravámenes, embargos o asignaciones de funcionarios de ingresos están pendientes o activos. La identificación temprana nos permite intervenir antes de que se incauten los activos o se congelen las cuentas.

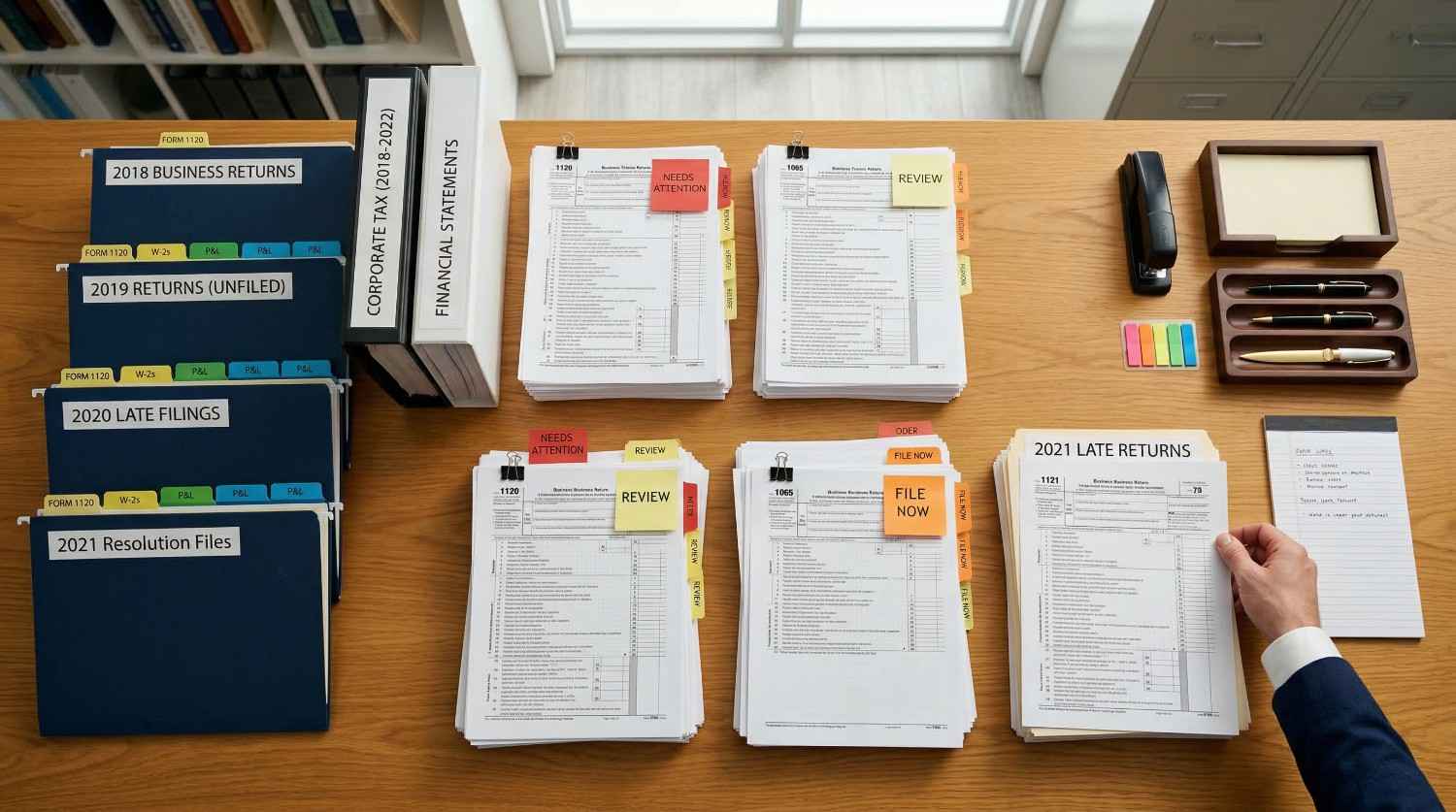

Reconstrucción y archivado preciso

- Reconstrucción de registros financieros: Si sus libros están incompletos, reconstruimos los ingresos y los gastos mediante extractos bancarios, informes de procesadores comerciales, formularios de terceros y la documentación disponible. Nuestro enfoque sigue los estándares de reconstrucción aceptados por el IRS.

- Preparación de la devolución específica de la entidad: Preparamos los formularios federales correctos según la estructura de su empresa, incluidos el Anexo C, el formulario 1065, el formulario 1120-S, el formulario 1120 y las declaraciones de nómina cuando es necesario. Cada declaración se revisa con usted antes de presentarla.

- Sustitución de devolución sustitutiva: Si el IRS prepara un sustituto para una declaración según la sección 6020 (b) del Código de Impuestos Internos, presentamos una declaración original exacta para reemplazarla. Las declaraciones sustitutivas generalmente excluyen las deducciones y los créditos, lo que a menudo resulta en un saldo significativamente inflado.

Estrategia de reducción y resolución de sanciones

- Solicitudes de reducción de multas: Evaluamos la elegibilidad para solicitar una reparación por causa razonable o una reducción por primera vez y presentamos solicitudes formales por escrito respaldadas por documentación. Esto puede reducir considerablemente la responsabilidad general cuando se apruebe.

- Negociación de resolución estructurada: Una vez establecidos los saldos precisos, negociamos los acuerdos de pago a plazos, las ofertas de compromiso o las clasificaciones por dificultades económicas en función de su situación financiera. Nuestro objetivo es la estabilidad a largo plazo y el cumplimiento obligatorio.

Por qué esto empeora sin ayuda

Las declaraciones de impuestos comerciales no presentadas crean una exposición compuesta. El IRS cuenta con sistemas automatizados diseñados para detectar las presentaciones faltantes e iniciar la ejecución.

Sustituto de las evaluaciones de devolución

- Devoluciones preparadas por el IRS: Según IRS.gov, cuando no se presenta la declaración requerida, el IRS puede preparar una declaración sustitutiva utilizando la información de ingresos de terceros. Estas presentaciones excluyen los gastos comerciales, las deducciones y los créditos.

- Obligación tributaria inflada: Debido a que las deducciones no están incluidas, el saldo tasado suele ser significativamente más alto de lo que adeudaría si hubiera presentado la declaración correctamente. Esta cantidad inflada pasa a ser legalmente exigible una vez evaluada.

Acumulación de multas e intereses

- Penalización por no presentar la solicitud: La multa es generalmente del 5% del impuesto no pagado por mes, hasta un máximo del 25 por ciento. Esto aumenta rápidamente si se trata de varios años.

- Multas e intereses por falta de pago: El IRS también aplica multas mensuales por falta de pago e intereses compuestos diarios a la tasa federal a corto plazo más un tres por ciento, como se describe en IRS.gov.

Aumento de la actividad de cobro

- Gravámenes fiscales federales: Se puede presentar un gravamen en virtud del artículo 6321 del Código de Impuestos Internos, que se adjuntará a su propiedad y pasará a ser un registro público. Esto puede dañar las oportunidades de crédito y financiación de las empresas.

- Autoridad recaudadora: Según el artículo 6331, el IRS puede embargar cuentas bancarias, embargar salarios o embargar cuentas por cobrar después de emitir las notificaciones requeridas. No se necesita la aprobación del tribunal cuando se siguen los procedimientos legales.

- Asignación de oficial de ingresos: El incumplimiento prolongado aumenta la probabilidad de que su caso sea asignado a un oficial de ingresos local para que lo haga cumplir sobre el terreno.

Cuanto más espere, menos protecciones procesales estarán disponibles.

Cómo el IRS hace cumplir esto

El IRS hace cumplir las obligaciones de presentación y pago a través de la autoridad legal otorgada por el Código de Impuestos Internos.

Requisitos de presentación obligatoria

Proceso de escalamiento de avisos

Autoridad de cobro

Ejecución penal

El cumplimiento voluntario reduce sustancialmente la severidad de la aplicación y preserva los derechos procesales.

Estas herramientas de cumplimiento son reales y se utilizan activamente. La representación temprana permite la intervención antes de que se produzca un daño financiero irreversible.

Para quién es este servicio

Necesita este servicio si:

- Varios años sin archivar: Lo necesita si no ha presentado una o más de las declaraciones de impuestos comerciales requeridas y los avisos del IRS han empezado a llegar a su dirección.

- Evaluación de devolución sustitutiva: Lo necesita si el IRS preparó un sustituto de una declaración que exageró sus ingresos y generó un saldo que no puede explicar.

- Amenazas de aplicación activa: Lo necesita si el IRS ha amenazado con imponer un embargo, ha presentado un gravamen tributario o ha asignado su caso a un oficial de ingresos.

- Exposición al impuesto sobre la nómina: Necesita una auditoría si su empresa tiene declaraciones de nómina sin presentar o impagas y teme que la multa por recuperación del fondo fiduciario asuma la responsabilidad personal.

- Brechas en el mantenimiento de registros: Lo necesita si carece de registros financieros completos y se siente incapaz de reconstruir sus libros sin ayuda profesional.

- Necesidades de financiación empresarial: Lo necesita si los prestamistas, inversores o compradores requieren una prueba de cumplimiento tributario antes de seguir adelante.

- Miedo a ponerse en contacto con el IRS: Lo necesita si tiene miedo de hablar directamente con el personal del IRS y desea una representación para gestionar las comunicaciones.

Si esto se aplica a usted, la representación estructurada es esencial.

Errores comunes que cometen las personas

Muchos contribuyentes empeoran su situación al cometer errores evitables:

Evitar estos errores protege sus finanzas personales y empresariales.

Nuestro proceso de representación

Evaluación integral del caso

Comenzamos con una revisión detallada y confidencial de toda su situación tributaria. Esto incluye identificar todas las declaraciones comerciales no presentadas, revisar las notificaciones del IRS que haya recibido y evaluar si ya se han tomado medidas de ejecución, como embargos o gravámenes. También evaluamos la estructura de su empresa, la exposición a la nómina y su situación financiera actual. Este procedimiento nos permite desarrollar un plan estructurado adaptado específicamente a sus circunstancias, en lugar de aplicar un enfoque único para todos los casos.

Presentación del poder notarial del IRS

A continuación, preparamos y presentamos el formulario 2848 del IRS, poder notarial y declaración de representante. Esto nos autoriza a actuar en su nombre ante el IRS. Una vez que el IRS procese el formulario, los agentes deben comunicarse directamente con nuestra oficina en lugar de comunicarse con usted. Tenemos acceso a las transcripciones de su cuenta y a las notas de casos internas, y podemos hablar directamente con los funcionarios de ingresos y los representantes de recaudación para proteger sus intereses de inmediato.

Revisión de la transcripción y el cumplimiento

Una vez que confirmemos la autorización, adquiriremos las transcripciones completas de su cuenta del IRS para todos los años pertinentes. Estos registros revelan exactamente qué declaraciones faltan, si se presentaron declaraciones sustitutivas, qué sanciones se han impuesto y si se acercan los plazos de cobro. Analizamos estos datos detenidamente para determinar los años prioritarios e identificar oportunidades para reducir las exageradas cuotas o evitar la adopción de medidas coercitivas inminentes.

Reconstrucción de registros financieros

Si sus registros están incompletos, reconstruimos su historial financiero utilizando métodos aceptados por el IRS. Recopilamos los estados de cuenta bancarios, los resúmenes de los procesadores comerciales, los registros de las tarjetas de crédito, la documentación de nómina y cualquier formulario de presentación de informes de terceros, como los formularios 1099 o W-2. Con esta información, calculamos los ingresos totales defendibles e identificamos los gastos comerciales legítimos. Nuestro objetivo es preparar declaraciones precisas que resistan el escrutinio y, al mismo tiempo, asegurarnos de que usted reclame todas las deducciones a las que tiene derecho legalmente.

Preparación y presentación de declaraciones

Una vez que se completa la reconstrucción, preparamos todas las declaraciones federales de negocios e individuales relacionadas requeridas. Revisamos cuidadosamente cada declaración para comprobar su precisión y coherencia antes de presentarla. Puede revisar y hacer preguntas para comprender completamente lo que se presenta. Después de la presentación, supervisamos el procesamiento del IRS para confirmar que las declaraciones sustitutivas se sustituyan y que los saldos se actualicen correctamente.

Abogacía por la reducción de sanciones

Tras la evaluación, evaluamos su elegibilidad para la desgravación de la multa. Determinamos si se aplican los argumentos de causa razonable o si se cumplen los criterios de reducción por primera vez. Preparamos las solicitudes formales por escrito respaldadas por documentación que explica las circunstancias que rodearon su falta de presentación. Luego, hacemos un seguimiento constante con el IRS para buscar reducciones que puedan reducir significativamente su responsabilidad general.

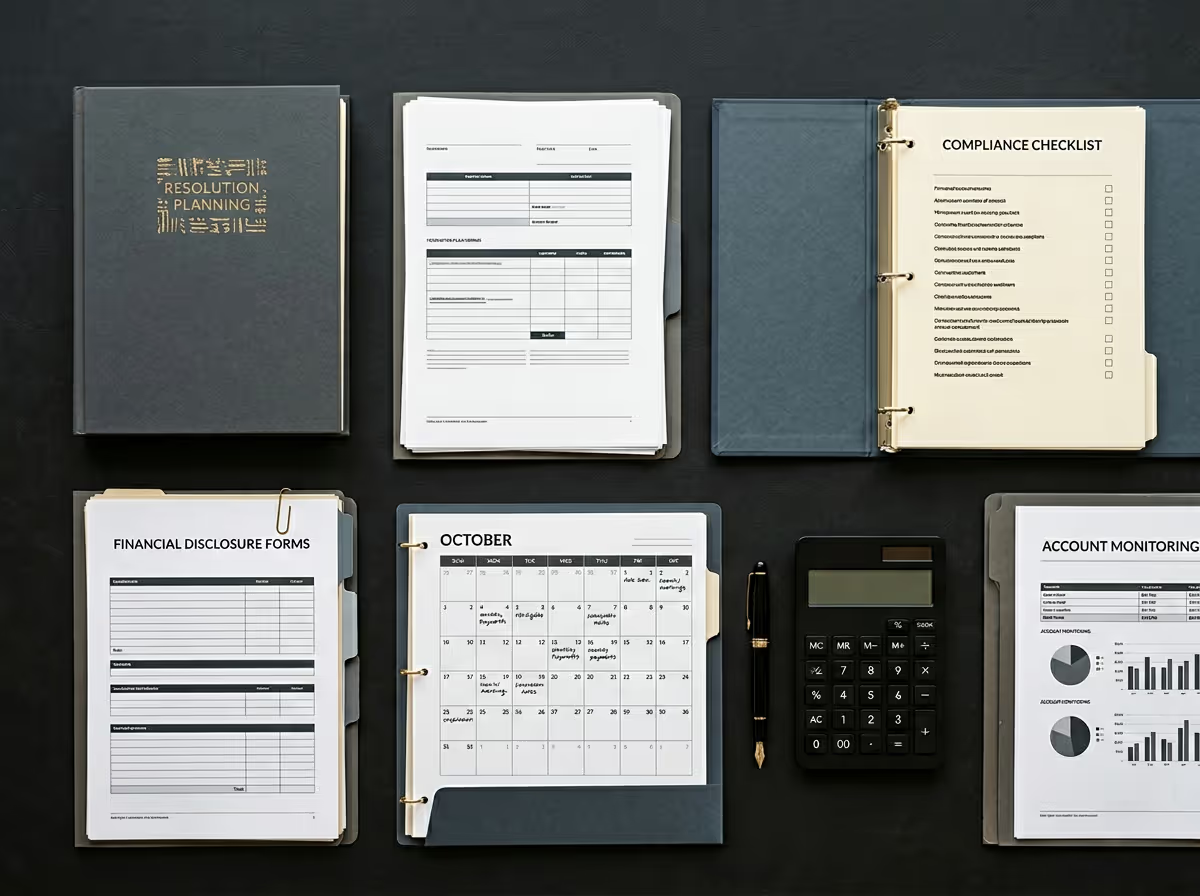

Negociación de resolución

Una vez establecidos los saldos precisos, negociamos una resolución estructurada. Esto puede implicar un acuerdo de pago a plazos, una oferta de compromiso o una situación de dificultad económica, según su capacidad financiera. Preparamos los formularios de divulgación financiera requeridos, presentamos su caso de manera clara y abogamos por condiciones que sean realistas y sostenibles. Nuestro objetivo es la estabilidad a largo plazo, no las promesas a corto plazo.

Supervisión continua del cumplimiento

Una vez que la resolución esté en vigor, lo ayudamos a mantener el cumplimiento en el futuro. Brindamos orientación sobre la presentación oportuna, los pagos de impuestos estimados, los depósitos de nómina y las prácticas de mantenimiento de registros. Mantenerse al día es esencial porque la falta de nuevas presentaciones puede resultar en incumplimiento de los acuerdos existentes. Estamos disponibles para atender la correspondencia futura del IRS y asegurarnos de que su plan de cumplimiento siga por buen camino.

Qué pasa si no haces nada

Finalización de la evaluación: El IRS puede finalizar las evaluaciones de declaraciones sustitutivas si los plazos del Tribunal Tributario vencen sin respuesta.

Acumulación de penalizaciones: Las multas por no presentar la solicitud y por no pagar siguen aumentando mes a mes.

Avisos de escalada: Las comunicaciones del IRS se vuelven más urgentes y menos flexibles.

Aviso final de intención de gravar: El IRS puede emitir la CP90 o la carta 1058, iniciando los derechos de embargo después de 30 días.

Presentación de gravámenes tributarios federales: Se puede registrar un gravamen público, lo que afecta el crédito y la reputación empresarial.

Asignación de oficial de ingresos: Los casos se pueden asignar a la actividad de recopilación de datos sobre el terreno.

Impuestos sobre cuentas bancarias: Es posible que se congelen las cuentas comerciales y se incauten los fondos.

Embargo salarial: El salario o los sorteos pueden redirigirse al IRS.

Incautación de cuentas por cobrar: Los pagos de los clientes pueden ser interceptados.

Incautación de activos: Se pueden tomar y vender equipos, vehículos o bienes inmuebles.

Riesgo de remisión penal: Los casos graves pueden remitirse a la Investigación Criminal del IRS.

El retraso aumenta el daño.

Preguntas frecuentes (FAQ)

Actúe ahora

Las declaraciones de impuestos comerciales no presentadas ponen en riesgo sus finanzas comerciales y personales. El IRS tiene la autoridad para evaluar, embargar, embargar e incautar. Esperar no mejora la situación.

Intervenimos en virtud de un poder notarial. Identificamos los documentos que faltan. Reemplazamos las devoluciones. Solicitamos una desgravación de la multa. Negociamos una resolución estructurada. Lo protegemos de la aplicación de la ley siempre que sea posible.

Actúe ahora mientras haya opciones abiertas.

Llama hoy para comenzar a restablecer el cumplimiento y proteger su futuro.

Los resultados dependen de las circunstancias individuales y de las determinaciones del IRS. No se garantiza ningún resultado. La representación está sujeta a las normas y procedimientos del IRS. Se aplica la divulgación de la Circular 230 del IRS.