Gracias por contactar

Obtenga TaxReliefNow.com!

Hemos recibido tu información. Si tu problema es urgente, como un aviso del IRS

o embargo de salario: llámenos ahora al + (88) 260 941 para obtener ayuda inmediata.

o embargo de salario: llámenos ahora al + (88) 260 941 para obtener ayuda inmediata.

¡Uy! Algo salió mal al enviar el formulario.

¡OBTENGA UNA DESGRAVACIÓN FISCAL AHORA!

NUESTROS SERVICIOS

Soluciones integrales de desgravación fiscal hechas a su medida

Desde ofertas de compromiso del IRS y reducciones de multas hasta apoyo a nivel estatal para declaraciones no presentadas, nuestros servicios integrales están personalizados para resolver su deuda tributaria y recuperar su tranquilidad financiera.

Planes de pago del IRS para individuos | Immediate Relief

Si se enfrenta a una acción fiscal del IRS y no puede pagar su factura de impuestos, podemos ayudarlo a establecer un plan de pago del IRS.

.svg)

Oferta de compromiso para individuos | Immediate Relief

Si está abrumado por las deudas tributarias y se enfrenta a embargos salariales o impuestos bancarios, podemos ayudarlo a solicitar una oferta de compromiso (OIC).

Actualmente no es coleccionable | Immediate Relief

Si adeuda impuestos sobre la renta y no puede pagar, las acciones de cobro del IRS pueden crear una grave presión financiera.

.avif)

Ayuda del IRS para el embargo salarial | Immediate Relief

Si se enfrenta a un embargo salarial por parte del IRS, el Servicio de Impuestos Internos puede emitir un embargo salarial después de recibir una notificación final de intención de recaudar.

Ayuda con impuestos bancarios del IRS |

Alivio inmediato

Alivio inmediato

Si su cuenta bancaria ha sido congelada debido a las tasas bancarias del IRS, es posible que el Servicio de Impuestos Internos haya emitido una notificación final de intención de embargar.

Resolución de gravámenes fiscales federales | Alivio inmediato

Un gravamen tributario federal es un registro público presentado por el Servicio de Impuestos Internos cuando las deudas tributarias permanecen impagas, relacionadas con bienes inmuebles, bienes personales y activos financieros.

Representación de auditoría del IRS | Protección inmediata

Si recibió una carta de auditoría del IRS, el Servicio de Impuestos Internos está revisando su declaración de impuestos según la ley tributaria federal y el Código de Impuestos Internos.

.avif)

Representación de apelaciones del IRS | Ayuda inmediata

Si el Servicio de Impuestos Internos rechazó su solicitud o emitió una notificación de deficiencia, aún puede impugnar la decisión a través de la Oficina de Apelaciones Independiente del IRS.

.avif)

Alivio para cónyuges inocentes | Alivio inmediato

Si el IRS tiene obligaciones tributarias vinculadas a una declaración conjunta con un excónyuge, es posible que califique para una compensación por cónyuge inocente.

.avif)

Representación de cobros del IRS | Ayuda inmediata

Si se enfrenta a cobros del IRS por impuestos atrasados, el Servicio de Impuestos Internos puede tomar medidas de cumplimiento a través del proceso de recaudación del IRS.

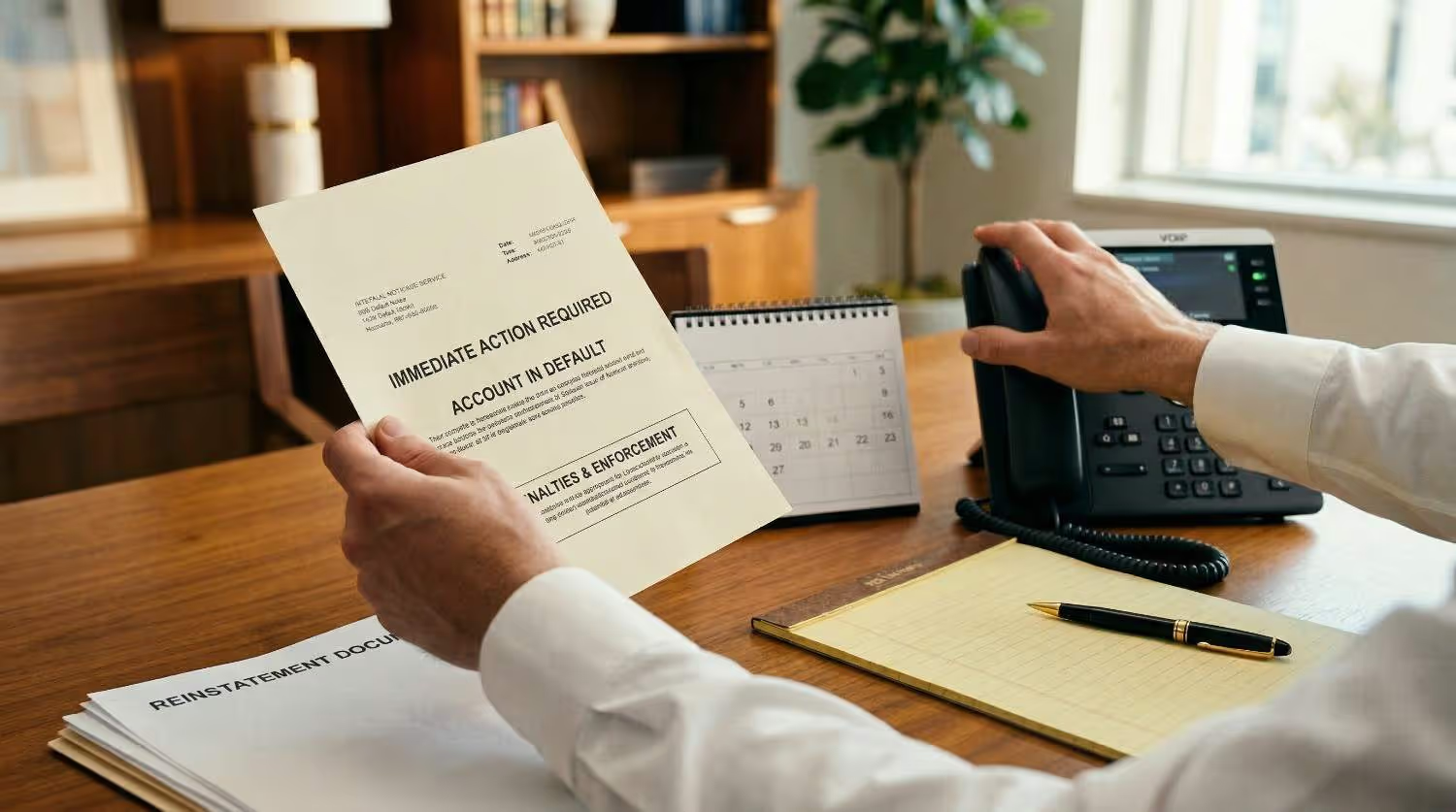

Resolución de notificaciones del IRS | Ayuda inmediata

Si recibió una notificación del IRS, es posible que el Servicio de Impuestos Internos esté revisando su declaración de impuestos, su cuenta tributaria o sus declaraciones de impuestos federales sobre la renta.

Declaraciones de impuestos individuales sin presentar | Immediate Relief

Si tiene declaraciones de impuestos sin presentar, es posible que el Servicio de Impuestos Internos ya tenga los datos de ingresos del formulario W-2, el formulario 1099 o los registros de transcripciones de salarios e ingresos.

Preparación de impuestos atrasados para individuos | Immediate Relief

Si tiene declaraciones de impuestos sin presentar, el Servicio de Impuestos Internos puede señalar la falta de actividad de declaración de impuestos vinculada a su número de seguro social durante la temporada de impuestos.

Revisión de la transcripción del IRS | Immediate Relief

Si recibió un aviso de saldo adeudado y no comprende sus obligaciones tributarias, una revisión de la transcripción del IRS puede aclarar la información de su cuenta tributaria.

Planes de pago del IRS para empresas | Immediate Relief

Si su empresa le debe al IRS y no puede pagar el saldo total, se encuentra en una situación urgente. El IRS hace cumplir la ley contra las empresas con rapidez, especialmente cuando se trata de impuestos sobre la nómina.

Defensa contra multas por recuperación de fondos fiduciarios | Immediate Relief

Si el IRS se ha puesto en contacto con usted en relación con una multa por recuperación de fondos fiduciarios, se enfrenta a una exposición personal por el impago de impuestos sobre la nómina.

.avif)

Ayuda para recaudar impuestos a bancos comerciales del IRS | Immediate Relief

La cuenta bancaria de su empresa ha sido congelada o acaba de recibir un aviso de que el IRS tiene la intención de embargarla. La nómina vence. Los vendedores están esperando.

Defensa del oficial de ingresos del IRS | Ayuda inmediata

Si su empresa le debe al IRS y no puede pagar el saldo total, se encuentra en una situación urgente. El IRS hace cumplir la ley contra las empresas con rapidez, especialmente cuando se trata de impuestos sobre la nómina.

Representación de auditoría del IRS para empresas | Immediate Relief

Si su empresa ha recibido una notificación de auditoría del IRS, se enfrenta a un examen federal serio. Una auditoría del IRS no es una solicitud rutinaria de documentación.

.avif)

Representación de apelaciones del IRS para empresas | Immediate Relief

Si su empresa ha recibido una carta de 30 días, una carta de 90 días, un informe de auditoría, una notificación de multa, un plan de pago rechazado o una notificación final de intención de gravar, se enfrenta a una disputa fiscal federal grave.

Representación de cobros del IRS (empresarial) | Immediate Relief

Cuando su negocio se dedica a las recaudaciones del IRS, no está tratando con un acreedor típico. El Servicio de Impuestos Internos tiene la facultad administrativa de hacer cumplir la ley, lo que le permite embargar cuentas bancarias, embargar cuentas por cobrar, declarar embargos tributarios federales y, en casos graves, cerrar operaciones.

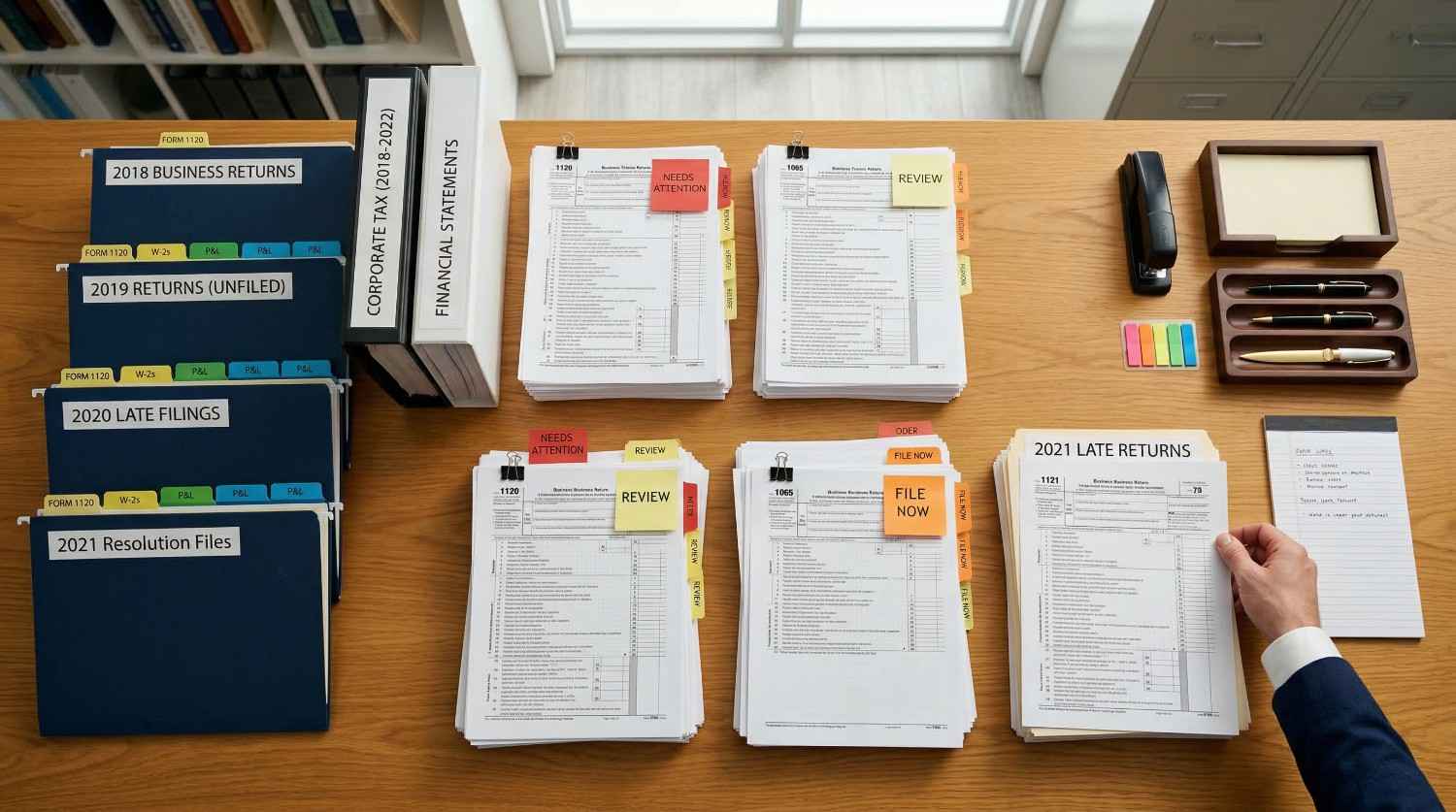

Declaraciones de impuestos comerciales no presentadas | Immediate Relief

Si sus declaraciones de impuestos comerciales permanecen sin presentar, corre el riesgo de que el IRS las haga cumplir. La aplicación de la ley por parte del IRS podría afectar sus cuentas bancarias, ingresos, activos comerciales y responsabilidad personal. Es posible que las cartas ya estén llegando.

Declaraciones de impuestos sobre nómina atrasadas | Immediate Relief

Cuando su negocio se dedica a las recaudaciones del IRS, no está tratando con un acreedor típico. Si tiene declaraciones de impuestos sobre la nómina sin presentar, se encuentra ante una de las categorías de cumplimiento más graves del IRS. Los impuestos sobre la nómina no se tratan como los impuestos sobre la renta ordinarios. El Servicio de Impuestos Internos tiene la facultad de hacer cumplir la ley administrativa que le permite embargar cuentas bancarias, embargar cuentas por cobrar, presentar gravámenes tributarios federales y, en casos graves, cerrar operaciones.

Planes de pago de impuestos estatales para individuos | Immediate Relief

Si su estado dice que debe impuestos atrasados y no puede pagar el saldo total, es probable que esté bajo una gran presión.

Ayuda estatal para el embargo de salarios | Immediate Relief

Si los impuestos impagos están embargando su salario, es probable que se sienta atrapado y abrumado. Trabajas duro, pero parte de tu salario desaparece incluso antes de que llegue a tu cuenta.

Ayuda con impuestos de State Bank | Ayuda inmediata

Cuando el IRS congela su cuenta bancaria, todo cambia de la noche a la mañana. De repente, el IRS bloquea el dinero que estaba disponible solo ayer.

Resolución de gravámenes fiscales estatales | Alivio inmediato

Si su estado dice que debe impuestos atrasados y no puede pagar, enterarse de que el IRS ha presentado una notificación de gravamen fiscal federal contra usted o su empresa puede resultar abrumador. Es público. Afecta a su crédito. Al saldo total, es probable que esté bajo una fuerte presión.

Representación de auditoría estatal: individuos | Immediate Relief

Una auditoría del IRS puede parecer que su vida acaba de detenerse. Abres un aviso y, de repente, el gobierno federal cuestiona tus ingresos, deducciones, créditos o registros comerciales.

Declaraciones de impuestos estatales sin presentar | Immediate Relief

Si tiene declaraciones de impuestos estatales sin presentar, no está solo. Muchas personas y propietarios de pequeñas empresas se atrasan durante períodos financieros difíciles, problemas de salud, divorcios, crisis empresariales o una simple desorganización de sus registros.

Planes estatales de pago de impuestos comerciales | Immediate Relief

Cuando su empresa se atrasa en el pago de sus obligaciones tributarias federales, la presión puede ser inmediata y abrumadora.

Problemas de impuestos estatales sobre la nómina | Immediate Relief

Los problemas con los impuestos sobre la nómina pueden resultar abrumadores, especialmente cuando comienzan a llegar avisos del IRS y el lenguaje se vuelve más urgente.

Ayuda para recaudar impuestos a bancos comerciales estatales | Ayuda inmediata

Cuando el IRS impone impuestos a la cuenta bancaria de su empresa, la interrupción es inmediata. La nómina puede fallar. Los pagos a los proveedores pueden rebotar.

Representación de auditoría estatal para empresas | Immediate Relief

Una auditoría empresarial del IRS puede interrumpir sus operaciones de la noche a la mañana. Es posible que se concentre en la nómina, los proveedores, el servicio al cliente y el crecimiento cuando, de repente, una notificación formal del IRS exige registros, explicaciones y plazos estrictos.

Declaraciones de impuestos comerciales estatales sin presentar | Immediate Relief

Cuando su empresa tiene declaraciones de impuestos estatales sin presentar y el IRS ya está enviando avisos, la presión puede ser constante.

Planes de pago del IRS en mora | Immediate Relief

Si su plan de pago del IRS está en mora, ya no se encuentra en una posición protegida. Es posible que lo que antes lo protegía del cobro agresivo ya no exista.

Oferta rechazada en compromiso | Immediate Relief

Si el IRS rechazó su oferta de compromiso (OIC), es probable que se sienta frustrado, desanimado y ansioso por los próximos pasos.

Problemas de impuestos atrasados de varios años | Immediate Relief

Cuando le debe al IRS durante varios años, el problema rara vez se mantiene controlado. Las multas y los intereses siguen aumentando.

Defensa policial del IRS | Alivio inmediato

Si el IRS ha empezado a enviar cartas certificadas amenazando con embargar su cuenta bancaria, embargar su salario o presentar una notificación de gravamen fiscal federal, no se trata solo de tramitar documentos.

Ayuda de acción de emergencia del IRS | Immediate Relief

Cuando el IRS comienza a hacer cumplir la ley, no parece algo rutinario. Se siente urgente y personal. Un impuesto salarial puede reducir su salario sin previo aviso.

Servicios de reducción de multas | Immediate Relief

Si se enfrenta a multas del IRS, ya comprende lo rápido que pueden aumentar. El incumplimiento de la fecha límite de presentación, un saldo impagado de impuestos o un problema con el depósito de nómina pueden generar multas que aumentan mes tras mes.

Planificación tributaria para individuos | Immediate Relief

Si recibe avisos del IRS, se enfrenta a un saldo creciente o le preocupa el embargo salarial o los impuestos bancarios, puede sentir que sus finanzas están bajo una amenaza constante.

Planificación fiscal para empresas | Immediate Relief

Cuando su empresa está bajo la presión del Servicio de Impuestos Internos, la planificación tributaria ya no se basa solo en ahorrar en el futuro.

Defensa de sustitución por devolución (SFR) | Immediate Relief

Cuando su empresa está bajo la presión del Servicio de Impuestos Internos Si el IRS presentó una declaración de impuestos en su nombre, la situación ya es grave. Una declaración sustitutiva (SFR) significa que el IRS preparó una declaración en su nombre porque usted no la presentó usted mismo. La planificación fiscal ya no se basa solo en ahorrar para el futuro.

Casos de deuda tributaria con saldos altos | Immediate Relief

Si le debe un saldo elevado al IRS, es probable que sienta una presión intensa. Es posible que los avisos lleguen con más frecuencia.

Problemas tributarios multiestatales | Immediate Relief

Cuando su empresa está bajo la presión del Servicio de Impuestos Internos, los problemas tributarios multiestatales pueden resultar abrumadores muy rápidamente. Es posible que se haya mudado a un nuevo estado, pero siga recibiendo las facturas tributarias de su estado anterior. La planificación fiscal ya no consiste solo en ahorrar para el futuro.

Impuesto sobre la nómina y responsabilidad personal | Alivio inmediato

Cuando los impuestos sobre la nómina se retrasan, la situación puede agravarse muy rápidamente. Lo que comienza como un problema de flujo de caja dentro de su empresa puede convertirse en una amenaza personal directa.

Declaraciones de impuestos federales y estatales sin presentar | Immediate Relief

El retraso en las declaraciones de impuestos puede ocurrir lentamente. Un año perdido se convierte en dos. Luego, la vida se vuelve ajetreada, los negocios se complican, los registros se pierden y el miedo se apodera.

Calendario de publicación de impuestos del IRS | Immediate Relief

Cuando el IRS embarga su cuenta bancaria o comienza a embargar su salario, el impacto es inmediato.

Preguntas Frecuentes (FAQs)

¿Necesito un abogado o un profesional de impuestos para responder a la intención del IRS de imponer un embargo?

¿Qué pasa si el impuesto del IRS causa dificultades financieras inmediatas?

¿Puede el IRS emitir varios gravámenes tributarios en la misma cuenta?

Hágame saber cuánto tiempo suele tardar en liberarse un impuesto del IRS.

¿Qué sucede si ignoro un aviso de intención de embargar del IRS?

¿Puede el IRS embargar una cuenta bancaria conjunta?

¿En qué se diferencia una tasa bancaria de un embargo salarial por deuda tributaria?

¿Cómo puedo asegurarme de que la información de mi presentación es correcta antes de enviarla?

¿El IRS alienta a los transmisores a usar plataformas autorizadas?

¿Qué sucede después de obtener un TCC en línea?

¿Está listo para empezar?

No se pierda una valiosa desgravación fiscal. Cuanto antes presente la solicitud, más pronto podrá recibirla

facturas de impuestos reducidas, pagos más bajos y posibles reembolsos.

facturas de impuestos reducidas, pagos más bajos y posibles reembolsos.

Obtenga una revisión de la desgravación fiscal estatal