Defensa de sustitución por devolución (SFR) | Ayuda inmediata

Una vez evaluada, su cuenta entra en el proceso de cobro del IRS, al que pueden seguir medidas de cobro, como gravámenes o gravámenes tributarios federales. Avisos como el aviso CP2566 o la carta 3219 indican urgencia. Ayudamos a preparar una declaración correcta, utilizamos las transcripciones de impuestos y buscamos opciones como la reducción de las multas y un acuerdo de pago a plazos para restablecer el cumplimiento tributario y reducir lo que adeuda.

Qué hace este servicio

Un sustituto de la defensa de las declaraciones es una representación tributaria federal estructurada que se centre en corregir las declaraciones preparadas por el IRS y evitar que se agraven. No se trata de una preparación básica de impuestos. Es el restablecimiento del cumplimiento combinado con la gestión del cumplimiento.

Asumimos la representación autorizada

Preparamos y presentamos el formulario 2848 del IRS para representarlo ante el IRS. Una vez que se tramita el poder notarial, nos comunicamos directamente con el IRS en su nombre, obtenemos las transcripciones, respondemos a las notificaciones y coordinamos con las divisiones de cumplimiento y cobro.

Esto lo alivia del estrés de la comunicación del IRS y garantiza un enfoque estratégico y coherente para su caso.

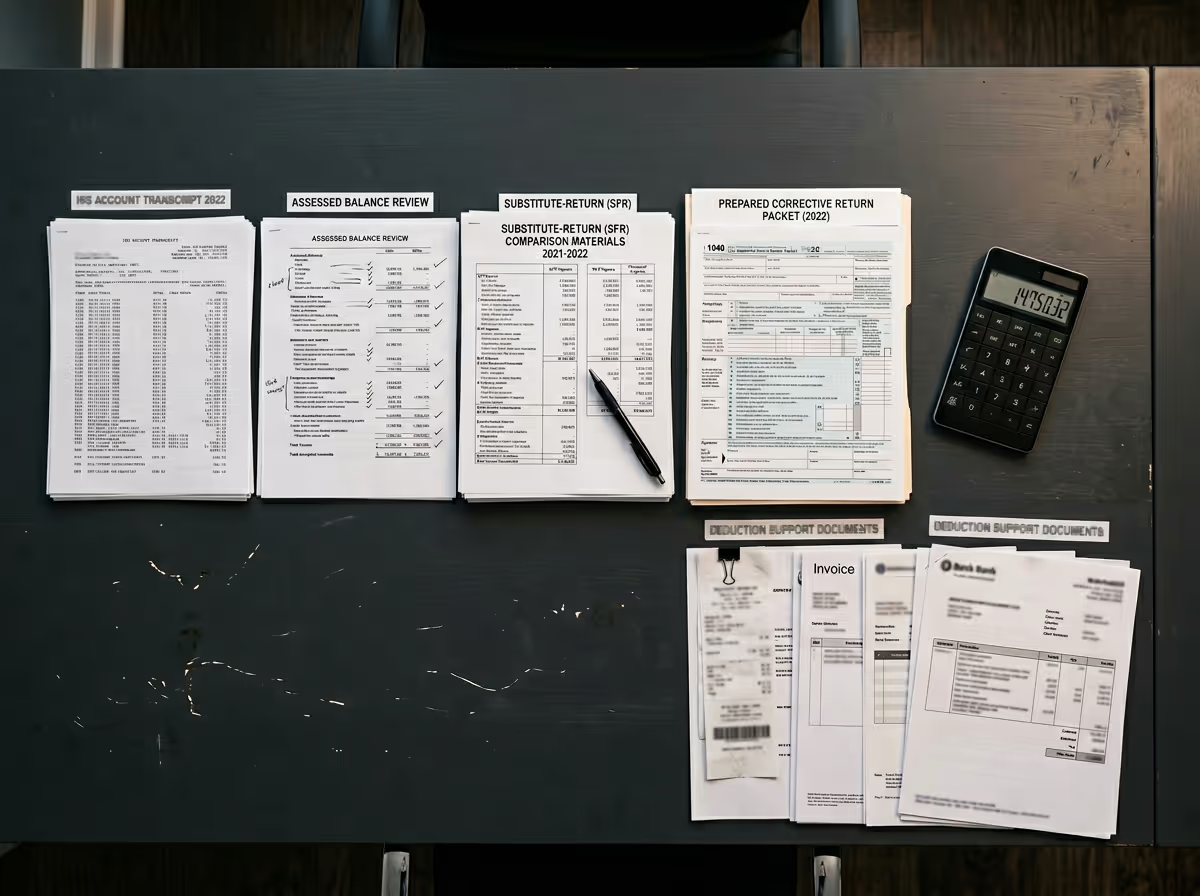

Realizamos una revisión completa de la cuenta

Obtenemos y revisamos las transcripciones de su cuenta del IRS para determinar:

- Verificamos si el IRS ha preparado una declaración sustitutiva o sustitutiva para su declaración de impuestos.

- Identificamos qué años tributarios faltan actualmente o qué años tributarios ya han sido evaluados por el IRS.

- Determinamos si se ha emitido una notificación de deficiencia para alguno de los períodos tributarios afectados.

- Confirmamos si tu cuenta está asignada a la recaudación automática o a un oficial de ingresos para que tome medidas coercitivas.

Preparamos y presentamos declaraciones precisas

El IRS afirma que, incluso si presenta una declaración sustitutiva, por lo general lo mejor para usted es presentar su propia declaración exacta. Una vez procesada, el IRS normalmente ajustará la cuenta para reflejar las cifras correctas.

Preparamos declaraciones federales completas y precisas para todos los años requeridos. En el caso de las personas, esto incluye la presentación adecuada de informes sobre los ingresos, las deducciones y los créditos, así como sobre el estado civil de la declaración. Para los propietarios de pequeñas empresas, el procedimiento consiste en declarar los ingresos comerciales y los gastos legítimos respaldados por la documentación disponible.

Reemplazar una SFR por una declaración debidamente preparada puede reducir significativamente los saldos evaluados en muchos casos.

Protegemos los derechos de las personas con deficiencias

Si recibió el CP3219N, por lo general tiene 90 días para responder antes de que el IRS proceda con la evaluación. Durante este período, puede presentar su declaración correcta o buscar las opciones de procedimiento apropiadas.

Hacemos un seguimiento y administramos estos plazos para preservar sus derechos.

Abordamos la exposición a las colecciones

Una vez que se evalúan los impuestos, comienza el proceso de recaudación del IRS. Determinamos si la aplicación de la ley ha comenzado o es inminente y tomamos las medidas apropiadas para reducir la exposición inmediata a gravámenes o gravámenes mientras se llevan a cabo las labores de cumplimiento.

Hacemos la transición a una resolución estructurada

Después de la presentación, se restablece el cumplimiento y evaluamos las estrategias de resolución a largo plazo. Estas pueden incluir acuerdos de pago a plazos, comprometer la contraprestación cuando existe la elegibilidad o demoras temporales en el cobro debido a dificultades financieras.

Un sustituto de la defensa de la devolución suele ser el primer paso hacia una resolución completa del IRS.

Por qué esto empeora sin ayuda

Los casos de sustitución de devoluciones se intensifican porque el IRS opera con plazos procesales estrictos.

Cuando el IRS prepara una SFR, por lo general calcula los impuestos basándose únicamente en los ingresos que se le reportan. Con frecuencia, no se incluyen las deducciones, los créditos ni los ajustes al estado tributario. Si ese número no se corrige, se convierte en el saldo tasado.

El IRS procede a realizar una evaluación si no se tiene en cuenta una notificación de deficiencia. El saldo pasa a ser legalmente cobrable después de haber sido evaluado.

Tras la evaluación, se emiten los avisos de facturación. Los intereses se acumulan a diario. Las multas siguen acumulándose. Si el saldo sigue sin pagarse, el IRS puede presentar una notificación de gravamen tributario federal. El IRS puede emitir una última notificación de intención de imponer un embargo y proceder con la imposición de gravámenes bancarios o embargos salariales si la ejecución persiste.

Las demoras reducen los derechos procesales y limitan las opciones disponibles. La intervención temprana preserva la flexibilidad.

Cómo el IRS hace cumplir esto

Los problemas de impuestos atrasados de varios años suelen seguir un camino estructurado de aplicación.

Sustituto de la creación de devoluciones

Cuando no se presentan las declaraciones requeridas, el IRS puede preparar una declaración sustitutiva utilizando los informes de ingresos de terceros. Estas declaraciones generalmente se basan en los ingresos brutos, no después de las deducciones.

Aviso de deficiencia

Después de preparar una declaración sustitutiva, el IRS puede emitir el CP3219N, también conocido como aviso de deficiencia. Los contribuyentes generalmente tienen 90 días para responder antes de la evaluación.

Evaluación del impuesto

Si no se responde dentro del período de deficiencia, el IRS evalúa el impuesto propuesto. El monto estimado se convierte en su obligación tributaria oficial.

Proceso de facturación y cobro

Después de la evaluación, el IRS envía los avisos de facturación. El proceso de cobro comienza y continúa hasta que se pague el saldo o se resuelva de otro modo.

Gravamen fiscal federal

Si el pago no se realiza después de la facturación, el IRS puede presentar una notificación de gravamen fiscal federal. Esto crea una demanda legal pública contra su propiedad y puede afectar las transacciones crediticias y financieras.

Notificación final de intención de gravar

Antes de incautar los activos, el IRS debe emitir un aviso final de intención de embargo, como el LT11. Si el problema sigue sin resolverse, se puede proceder a la ejecución.

Impuestos salariales y bancarios

El IRS puede embargar los salarios o emitir gravámenes bancarios. En el caso de un embargo bancario, los fondos generalmente se congelan durante 21 días antes de enviarlos al IRS, lo que proporciona un período de intervención limitado.

Certificación de pasaportes

En los casos relacionados con una deuda tributaria gravemente morosa, el IRS puede certificar la deuda ante el Departamento de Estado, lo que puede afectar la emisión o renovación del pasaporte.

Comprender esta estructura de cumplimiento nos permite intervenir estratégicamente.

Para quién es este servicio

- Necesita este servicio si recibió una notificación en la que se indica que el IRS presentó una declaración sustitutiva en su nombre y cree que el saldo calculado es incorrecto.

- Necesita este servicio si recibió el CP3219N y se encuentra dentro del período de respuesta de 90 días para evitar la evaluación.

- Necesita este servicio si tiene varios años tributarios sin declarar y el IRS ha comenzado a enviar avisos de cumplimiento.

- Necesita este servicio si el IRS evaluó los impuestos basándose únicamente en los ingresos declarados sin incluir las deducciones legítimas o los gastos comerciales.

- Necesita este servicio si recibió el CP504 o el LT11 y le preocupa un embargo salarial o un embargo bancario.

- Necesita este servicio si dirige una pequeña empresa y se ha retrasado en la presentación de los documentos requeridos debido a dificultades financieras.

- Necesita este servicio si está experimentando una creciente presión recaudatoria del IRS y desea una representación estructurada.

Para quién es este servicio

- Necesita este servicio si recibió una notificación en la que se indica que el IRS presentó una declaración sustitutiva en su nombre y cree que el saldo calculado es incorrecto.

- Algunas personas ignoran la fecha límite de notificación de deficiencia de 90 días, lo que hace que el IRS evalúe el impuesto propuesto sin impugnación.

- Muchas personas asumen que la declaración sustitutiva es definitiva y no se puede corregir, aunque presentar declaraciones precisas puede reducir el saldo.

- Algunos contribuyentes intentan establecer acuerdos de pago a plazos antes de presentar las declaraciones requeridas, lo que a menudo resulta en la denegación o el retraso.

- Llamar repetidamente al IRS sin una estrategia coordinada puede crear una comunicación inconsistente y debilitar la administración de casos.

- Ignorar las notificaciones de impuestos, como las CP504 o LT11, aumenta la probabilidad de embargo salarial o incautación de cuentas bancarias.

Nuestro proceso de representación

Evaluación inicial del caso

Comenzamos con una revisión detallada de sus avisos del IRS, las transcripciones de sus cuentas y el historial de presentación de solicitudes para comprender exactamente cuál es la situación de su caso. Esto incluye identificar si se preparó una declaración sustitutiva, si se emitió una notificación de deficiencia y si el impuesto ya se ha evaluado. También determinamos si la cuenta está en proceso de cobro activo. Esta evaluación nos permite priorizar de inmediato los plazos urgentes y los riesgos de cumplimiento.

Autorización de poder notarial

Preparamos y presentamos el formulario 2848 del IRS para establecer formalmente nuestra autoridad para representarlo ante el IRS. Una vez que el IRS acepte el poder notarial, podemos comunicarnos directamente con el personal del IRS, solicitar transcripciones, recibir avisos y responder en su nombre. Este paso garantiza una comunicación estratégica y centralizada, lo que protege su caso del incumplimiento de los plazos y de las declaraciones inconsistentes.

Análisis de transcripciones y cumplimiento

Tras la autorización, obtenemos las transcripciones completas de las cuentas y las analizamos cuidadosamente. Confirmamos qué años no se han presentado, si se han creado declaraciones sustitutivas, si se han evaluado los saldos exactos y si el caso ha sido asignado a una agencia de recaudación automatizada o a un oficial de ingresos. También revisamos las multas y la acumulación de intereses. Este análisis sirve como base para una estrategia correctiva informada y precisa.

Preparación de devoluciones correctas

Preparamos declaraciones de impuestos federales precisas para todos los años requeridos, asegurándonos de que las deducciones, los créditos y las elecciones de estado civil permitidos se informen correctamente. Para los propietarios de pequeñas empresas, esto incluye identificar los gastos comerciales legítimos respaldados por la documentación disponible. El objetivo es reemplazar las declaraciones sustitutivas por declaraciones precisas que reflejen su verdadera obligación tributaria y, potencialmente, reducir el saldo tasado.

Presentación y supervisión

Una vez que se completan las declaraciones, las enviamos a la ubicación de procesamiento correspondiente del IRS y supervisamos su progreso. Los tiempos de procesamiento del IRS pueden variar, por lo que hacemos un seguimiento de las actualizaciones y verificamos cuando se producen ajustes en la cuenta. Si el IRS solicita documentación o aclaraciones adicionales, respondemos con prontitud. El monitoreo continuo garantiza que las correcciones se reflejen adecuadamente y que la aplicación no se intensifique durante el procesamiento.

Estrategia de estabilización de colecciones

Si tu cuenta ya está en estado de cobro, evaluamos la fase de aplicación y tomamos medidas para reducir los riesgos inmediatos. Esto puede implicar comunicarse con las unidades de cobro del IRS para evitar que se impongan impuestos mientras se procesan las declaraciones. Durante esta fase, nos centramos en estabilizar la cuenta, evitar la incautación de activos y mantener una comunicación estructurada a medida que avanzamos en la presentación de solicitudes correctivas.

Planificación de la resolución

Una vez restablecido el cumplimiento y confirmados los saldos actualizados, evaluamos las opciones de resolución a largo plazo adecuadas en función de sus circunstancias financieras. Esto puede incluir un acuerdo de pago a plazos, comprometer la contraprestación cuando sea elegible o un retraso temporal en el cobro debido a dificultades económicas. Evaluamos los ingresos, los gastos permitidos y el capital de los activos para determinar la estrategia más adecuada para el futuro.

Guía de cumplimiento continuo

Una vez que se resuelva el problema del sustituto inmediato de la devolución, proporcionamos orientación para ayudar a evitar que vuelva a ocurrir. Esto puede incluir revisar los ajustes de retención, los requisitos de impuestos estimados y las prácticas de mantenimiento de registros. Mantener el cumplimiento futuro es fundamental para evitar que se renueven las medidas de cumplimiento. Queremos solucionar el problema actual y ayudarlo a mantenerse al día con el IRS.

Qué pasa si no haces nada

Si se encuentra dentro del período de notificación de deficiencia y no responde, el IRS puede continuar con la evaluación tributaria propuesta.

El incumplimiento de los plazos de respuesta puede limitar sus derechos procesales y dificultar las impugnaciones posteriores.

El IRS continuará emitiendo avisos de facturación mientras los intereses se acumulen diariamente y las multas aumenten el saldo total adeudado.

La cuenta puede transferirse a un sistema de cobro automático o asignarse a un oficial de ingresos para que tome medidas coercitivas.

El IRS puede presentar una notificación de gravamen fiscal federal, creando una reclamación pública contra su propiedad.

Si no hace los arreglos de pago, el IRS puede emitir una notificación final de su intención de cobrar.

Pueden producirse embargos salariales o gravámenes bancarios si el saldo sigue sin resolverse.

Preguntas frecuentes (FAQ)

Actúe ahora

Las sustituciones de los casos de devolución se llevarán a cabo a menos que se detengan. La evaluación conduce a la facturación. La facturación lleva al cobro. El cobro puede resultar en un gravamen y un embargo.

Tiene derecho a corregir las presentaciones sustitutivas inexactas y a presentar información financiera precisa. Actuar con prontitud protege esos derechos y amplía las opciones disponibles.

Intervenimos bajo la autoridad de un poder notarial, rectificamos las declaraciones sustitutivas cuando es posible, supervisamos los riesgos de ejecución y dirigimos su caso hacia una resolución bien organizada.

Llame ahora antes de que pase otra fecha límite.

Los resultados dependen de las circunstancias individuales y de las determinaciones del IRS. No se garantiza ningún resultado. La representación está sujeta a las normas y procedimientos del IRS. Se aplica la divulgación de la Circular 230 del IRS.