Oferta rechazada en compromiso | Alivio inmediato

Le ayudamos revisando su carta de rechazo del IRS, analizando el formulario 656, el formulario 433-A o el formulario 433-B y preparando la documentación de respaldo para el proceso de apelación. Actuando en virtud de un poder notarial, presentamos el formulario 13711 ante la Oficina de Apelaciones y buscamos opciones de desgravación fiscal, como acuerdos de pago a plazos, planes de pago o la condición de no cobrable actualmente en función de las dificultades financieras.

Qué hace este servicio

Una oferta de compromiso rechazada no es simplemente una carta de denegación. Es un cambio en el estado de su caso que requiere un análisis inmediato y una respuesta estructurada. Diseñamos nuestro servicio para protegerlo de la aplicación de la ley mientras identificamos el curso legal y procesal más sólido bajo la jurisdicción del IRS.

Intervenimos bajo un poder notarial y tomamos el control de la comunicación

Una vez que contrate a nuestra firma, preparamos y presentamos el formulario 2848 del IRS, poder notarial y declaración de representante. En IRS.gov se explica que el formulario 2848 autoriza a un representante elegible a actuar en su nombre ante el IRS. Esto nos da la autoridad para hablar directamente con el IRS, recibir avisos sobre las cuentas y administrar su caso de manera estratégica.

A partir de ese momento, ya no tendrá que atender las estresantes llamadas telefónicas del IRS ni interpretar únicamente las cartas técnicas. Nos convertimos en el punto de contacto oficial, lo que evita que las declaraciones inconsistentes, el incumplimiento de los plazos o las reacciones emocionales perjudiquen su caso.

Realizamos un análisis detallado de los rechazos

El IRS explica en IRS.gov que acepta una presentación del programa de oferta de compromiso cuando el monto refleja lo máximo que puede recaudar razonablemente en función de su potencial razonable de cobro, ingresos, gastos y capital patrimonial. El rechazo de una oferta de compromiso significa que el IRS determinó que su propuesta no cumplía con ese estándar en virtud de la ley tributaria.

Revisamos la carta de rechazo junto con el formulario 433-A o el formulario 433-B, incluida la declaración de información de cobro y los estados de cuenta bancarios y declaraciones de impuestos de respaldo, para verificar cómo se evaluó su situación financiera.

Analizamos cómo el especialista en ofertas calculó su obligación tributaria utilizando las tablas de ingresos/gastos y activos/patrimonio y determinamos si los ingresos se exageraron o si los gastos se rechazaron indebidamente. Si procede, preparamos el formulario 13711, el PDF de solicitud de apelación de una oferta de transacción, para llevar el caso a la oficina de apelaciones o evaluar alternativas, como un plan de pago, un acuerdo de pago parcial en cuotas o la condición de no cobrable actualmente.

Lo protegemos de la escalada de la actividad de recolección

El proceso de cobro del IRS continúa hasta que se resuelva una deuda tributaria o hasta que el IRS ya no pueda cobrarla legalmente. Tras un rechazo por parte de la OIC, su cuenta puede volver al estado de cobro activo si no existe ninguna otra solución.

Evaluamos de inmediato su exposición a la aplicación de la ley y determinamos si corre el riesgo de presentar un gravamen, recibir avisos de embargo o embargar su salario. Si se encuentra dentro del plazo de apelación de 30 días, nuestra prioridad es proteger ese plazo y, al mismo tiempo, estabilizar el estado de su cuenta.

Creamos la próxima estrategia correcta

No todas las ofertas de compromiso rechazadas deben apelarse. A veces, una apelación es apropiada porque el IRS se basó en información incompleta o incorrecta. Otras veces, la estrategia más sólida es abordar los problemas de cumplimiento y volver a colocar su caso en otra vía de resolución reconocida por IRS.gov, como un acuerdo de pago a plazos o una situación de dificultad temporal.

Evaluamos su situación de manera objetiva y seleccionamos el enfoque que se ajuste a su situación financiera real y a la postura del IRS en materia de cumplimiento de la ley. No hacemos conjeturas. Analizamos y actuamos deliberadamente.

Por qué esto empeora sin ayuda

No hacer nada después de que se rechace una oferta de compromiso puede aumentar rápidamente el riesgo. El IRS no detiene la ejecución indefinidamente porque se haya rechazado una oferta.

Los plazos de apelación vencen

IRS.gov establece que puede apelar una OIC rechazada en un plazo de 30 días. Si pasa ese plazo, pierde la oportunidad de una revisión independiente durante el proceso de apelaciones. Esperar incluso unas pocas semanas puede anular una de sus protecciones procesales más sólidas.

La actividad de recolección puede reanudarse

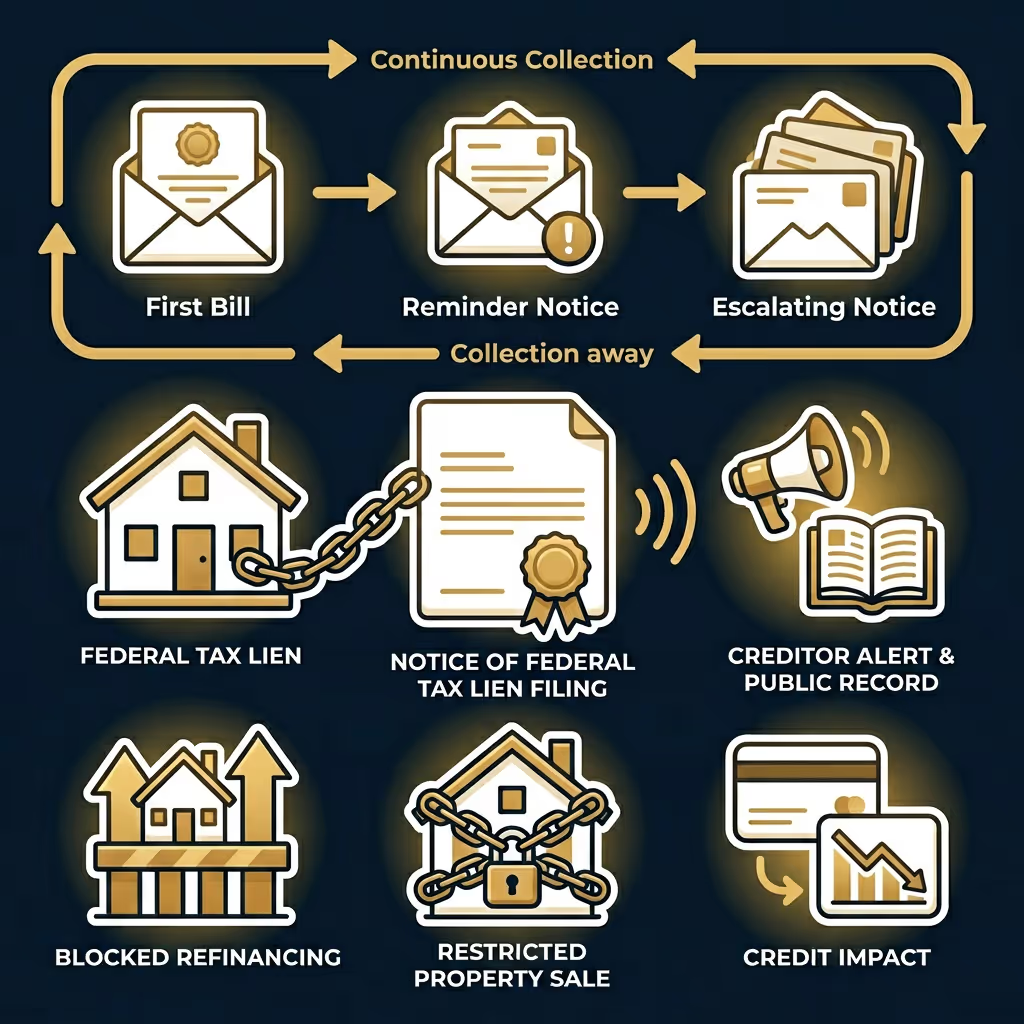

El proceso de cobro del IRS comienza con las notificaciones y continúa hasta que se resuelva la deuda. Si no hay ninguna resolución activa después de un rechazo, la cuenta puede continuar con el proceso de cobro. Los avisos pueden aumentar en tono y urgencia.

Se pueden presentar gravámenes fiscales federales

IRS.gov explica que un gravamen tributario federal es la demanda legal del gobierno contra su propiedad cuando usted descuida o no paga una deuda tributaria. El IRS puede presentar una notificación de gravamen fiscal federal en los registros públicos. Un gravamen puede afectar el crédito, las oportunidades de financiación y las relaciones comerciales.

Los impuestos se convierten en una posibilidad real

Según IRS.gov, un embargo es una incautación legal de una propiedad para satisfacer una deuda tributaria. Esto puede incluir embargos salariales y gravámenes a cuentas bancarias. Tras el rechazo, si no existe ningún otro acuerdo, el IRS conserva la autoridad para solicitar un embargo.

Las reacciones emocionales crean problemas de registro permanentes

Muchos contribuyentes llaman al IRS inmediatamente después de recibir un rechazo y argumentan su caso emocionalmente. Las declaraciones hechas durante esas llamadas pasan a formar parte del registro oficial del IRS. Las explicaciones inconsistentes sobre los ingresos, los activos o los gastos pueden socavar las apelaciones o negociaciones futuras. La representación profesional evita estos errores.

Cómo el IRS hace cumplir esto

Comprender la autoridad de cumplimiento del IRS ayuda a aclarar por qué es importante tomar medidas inmediatas después de que una OIC sea rechazada.

Avisos de cobro: iniciar y escalar el proceso

IRS.gov explica que si no paga sus impuestos en su totalidad, el IRS envía una factura que inicia el proceso de cobro. El proceso continúa hasta que la cuenta esté liquidada o hasta que el IRS ya no pueda cobrarla legalmente. Por lo general, las notificaciones aumentan con el tiempo y pasan de ser recordatorios a advertencias formales sobre la intención de cobrar.

Gravámenes fiscales federales

IRS.gov afirma que un gravamen fiscal federal es la demanda legal del gobierno contra su propiedad cuando usted no paga una deuda tributaria. El IRS puede presentar una notificación de gravamen fiscal federal para alertar a los acreedores. Esta presentación pública puede afectar la refinanciación, la venta de propiedades y el acceso al crédito.

CP504 Aviso de intención de gravar

IRS.gov explica que la CP504 es una notificación de intención de gravar emitida en virtud de la sección 6331 (d) del Código de Impuestos Internos. El aviso advierte que si no se realiza el pago, el IRS podría embargar ciertos bienes. Este aviso indica que la autoridad de ejecución se acerca a la ejecución.

Aviso final de LT11 o carta 1058

IRS.gov afirma que la LT11, o la carta 1058, le informa que el IRS tiene la intención de confiscar la propiedad o los derechos de propiedad. Indica a los contribuyentes que se comuniquen con el IRS de inmediato. En esta etapa, la autoridad recaudatoria puede ejercerse si no se establece ninguna resolución.

Los gravámenes bancarios y el período de retención de 21 días

IRS.gov explica que cuando el IRS impone impuestos a una cuenta bancaria, el banco generalmente retiene los fondos durante 21 días antes de enviarlos al IRS. Este período está diseñado para dar tiempo a comunicarse con el IRS o resolver errores. Sin embargo, durante esos 21 días, el acceso a los fondos está restringido.

Embargos salariales

IRS.gov afirma que un gravamen puede embargar los salarios. Una vez activo, el embargo salarial continúa hasta que se pague la deuda, se libere el embargo o se apruebe otra resolución autorizada. Este procedimiento puede crear problemas financieros a largo plazo si no se aborda rápidamente.

Para quién es este servicio

- Oferta rechazada en un plazo de 30 días: Lo necesita si su oferta de compromiso fue rechazada recientemente y aún se encuentra dentro del plazo de apelación de 30 días. Actuar con rapidez protege su derecho a apelar según los procedimientos del IRS.

- Cálculos controvertidos del IRS: Necesita este documento si cree que el IRS exageró sus ingresos, infravaloró los gastos permitidos o calculó mal el capital de sus activos al rechazar su oferta.

- Avisos de impuestos activos: La necesita si ha recibido la CP504, la LT11 o la carta 1058 y le preocupa un embargo salarial o un embargo bancario.

- Riesgo de gravamen fiscal federal: La necesita si le preocupa que el IRS pueda presentar o haya presentado una notificación de gravamen fiscal federal que afecte sus operaciones crediticias o comerciales.

- Incapacidad para pagar en su totalidad: Lo necesita si no puede pagar su deuda tributaria en su totalidad y necesita una resolución alternativa estructurada y legalmente reconocida.

- Exposición a pequeñas empresas: Necesita esta opción si es propietario de una pequeña empresa cuya nómina, cuentas o capital operativo podrían verse interrumpidos por la aplicación de la ley del IRS.

- Deseo de representación profesional: Lo necesita si desea que un representante calificado gestione todas las comunicaciones del IRS en virtud de un poder notarial y evite errores evitables.

Errores comunes que cometen las personas

Muchos contribuyentes empeoran su situación al cometer errores evitables:

Nuestro proceso de representación

Revisión inicial del caso y desglose del rechazo

Comenzamos con una revisión exhaustiva de su oferta de compromiso rechazada, que incluye la carta de rechazo del IRS, los estados financieros, la documentación de respaldo y el historial de cumplimiento. Comparamos cuidadosamente los motivos declarados por el IRS para la denegación con su situación financiera real. Esto nos permite identificar los errores de cálculo, las lagunas en la documentación o los problemas de cumplimiento que deben abordarse antes de seguir adelante con una estrategia de apelación o resolución alternativa.

Presentación de un poder notarial

Preparamos y presentamos el formulario 2848 del IRS, poder notarial y declaración de representante, para que podamos actuar legalmente en su nombre. Una vez que el IRS procese la autorización, nos convertimos en el contacto oficial para su caso. Esto significa que los agentes del IRS se comunican directamente con nosotros y no con usted, lo que evita declaraciones erróneas, reduce el estrés y garantiza que cada interacción siga una estrategia legal coordinada.

Transcripción de la cuenta y evaluación de riesgos

Una vez que se otorgue la autorización, obtendremos las transcripciones de su cuenta del IRS para confirmar los saldos, las multas, los códigos de incumplimiento y los indicadores de cumplimiento. Verificamos el motivo exacto por el que se rescindió el acuerdo de pago a plazos y si existe algún problema de cumplimiento adicional. Este paso evita suposiciones y garantiza que nuestra estrategia de negociación se base en registros precisos y completos del IRS.

Evaluación de apelaciones y decisión estratégica

Cuando la apelación es apropiada, preparamos los formularios requeridos y reunimos la documentación financiera organizada para respaldar su posición. Aclaramos los cálculos de ingresos, los gastos permitidos y las valoraciones de los activos para que la autoridad revisora pueda evaluar la información con precisión. Nuestro objetivo es presentar un caso claro y bien fundamentado en lugar de un argumento reactivo o emocional.

Planificación de resoluciones alternativas

Si no es aconsejable presentar una apelación, pasamos rápidamente a otras opciones reconocidas por el IRS, como los acuerdos de pago a plazos o la situación de dificultad temporal. Estructuramos propuestas que reflejen su capacidad realista de pago y, al mismo tiempo, lo protejamos del cobro forzoso. Este enfoque garantiza que se mantenga proactivo en lugar de permitir que su caso vuelva a derivar en una aplicación incontrolada.

Supervisión continua del cumplimiento

Una resolución exitosa requiere el cumplimiento continuo de las obligaciones de presentación y pago. Lo guiamos a través de los pagos estimados, las presentaciones obligatorias y las responsabilidades futuras de presentación de informes para evitar que se reinicie la aplicación de la ley. Mantener el cumplimiento fortalece su credibilidad ante el IRS y ayuda a garantizar la estabilidad de cualquier resolución.

Qué pasa si no haces nada

Se cierra la ventana de apelación: IRS.gov establece que debe apelar una oferta de compromiso rechazada en un plazo de 30 días. Si ese período vence, pierde el derecho formal de apelar la decisión.

El estado de recopilación se reactiva: Es posible que tu cuenta vuelva a ser de cobro activo, lo que aumentará la frecuencia y la urgencia de las notificaciones.

Escalación de avisos: Puede recibir el CP504, que IRS.gov describe como un aviso de intención de embargar. Esto indica que el IRS se está preparando para ejercer la autoridad de embargo si el saldo sigue sin pagarse.

Mayor riesgo de cumplimiento: Sin una resolución en vigor, el IRS puede evaluar la presentación de un gravamen o una acción de embargo.

Aviso final de gravamen: Es posible que reciba una LT11 o una carta 1058, lo que según IRS.gov significa que el IRS tiene la intención de confiscar la propiedad o el derecho de propiedad.

Exposición a impuestos bancarios: Si se emite un embargo bancario, los fondos pueden congelarse y quedar sujetos al período de retención de 21 días descrito en IRS.gov.

Riesgo de embargo salarial: Los impuestos salariales pueden comenzar y continuar hasta que se resuelva la deuda o se libere el impuesto.

Preguntas frecuentes (FAQ)

Actúe ahora

Una oferta de compromiso rechazada no es el final de sus opciones, pero es un momento crítico. El plazo de apelación es limitado. La presión de recolección puede regresar. Los embargos y gravámenes siguen estando legalmente disponibles para el IRS bajo la autoridad federal.

Intervenimos bajo el poder notarial, tomamos el control de la comunicación, analizamos minuciosamente el rechazo y construimos la estrategia más sólida posible de acuerdo con los procedimientos del IRS.

No espere al próximo aviso. Póngase en contacto con nosotros ahora y permítanos protegerlo antes de que la aplicación de la ley se intensifique aún más.

Los resultados dependen de las circunstancias individuales y de las determinaciones del IRS. No se garantiza ningún resultado. La representación está sujeta a las normas y procedimientos del IRS. Se aplica la divulgación de la Circular 230 del IRS.