Calculadora de multas e intereses del IRS — Año tributario 2012

Por qué su saldo tributario de 2012 puede ser mucho mayor de lo esperado

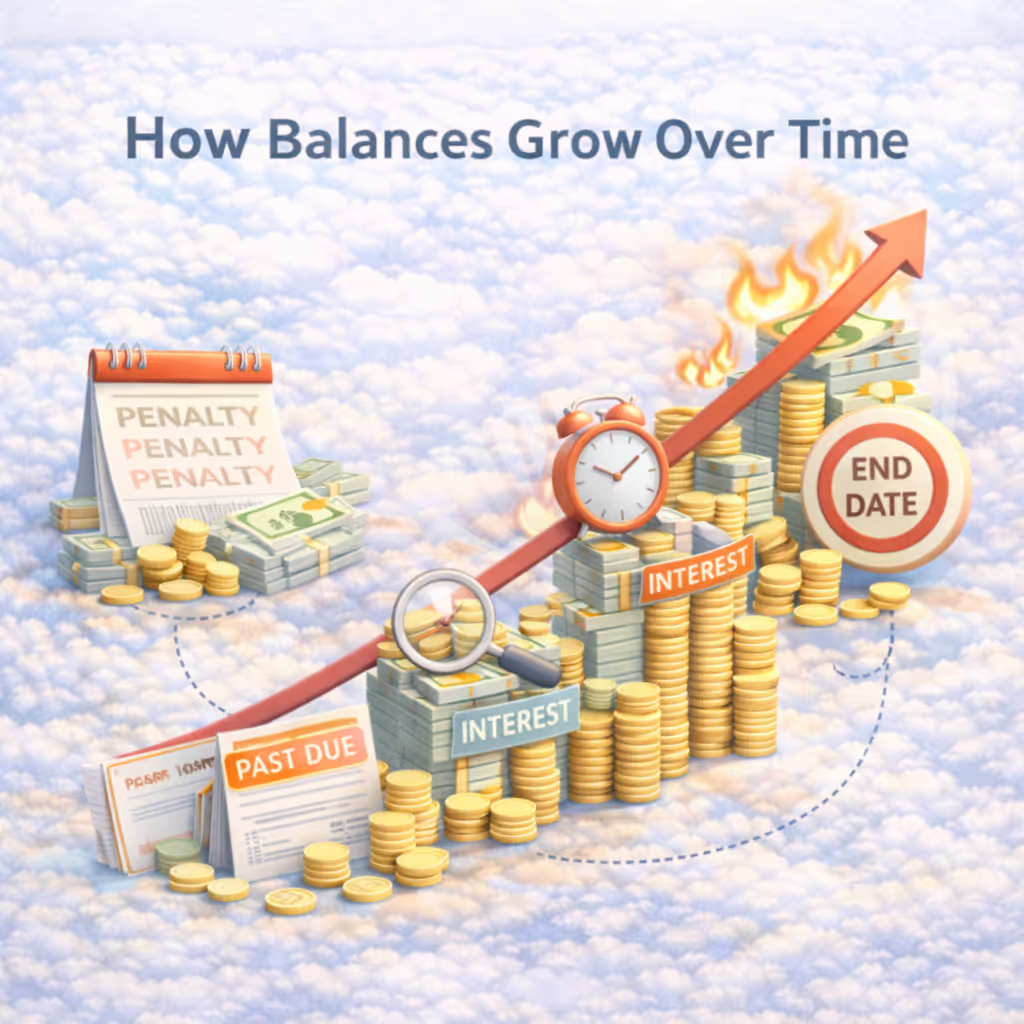

Si adeuda al Servicio de Impuestos Internos por el año tributario 2012, la reacción más común es la sorpresa, no porque el año sea reciente, sino porque el saldo parece mucho mayor de lo esperado. Muchos contribuyentes recuerdan el 2012 como un año en el que «en realidad no pasó nada». Es posible que el IRS haya recibido algunos avisos al principio o que no haya recibido ninguno después de cierto punto. Como la aplicación de la ley no era inmediata, era fácil suponer que los impuestos impagos se mantenían estables o que no crecían de manera agresiva.

Tarda entre 60 y 90 segundos

No se requiere número de seguro social

Solo estimación

.avif)