Employers operating in the United States are legally responsible for withholding and remitting federal payroll taxes on behalf of their employees. These obligations include federal income taxes, social security, Medicare, and the additional medicare tax, all of which must be deposited with the Internal Revenue Service promptly and accurately. When these taxes remain unpaid, the financial and legal consequences can be severe, including penalties, accrued interest, and potential enforcement actions.

Unpaid federal payroll taxes are considered trust fund taxes because they are funds withheld from employees' wages for the benefit of the government and social security programs. Employers generally act as fiduciaries, meaning they hold these amounts in trust until they deposit them. Failing to submit withheld income taxes or social security and medicare contributions places the business and its officers at risk of personal liability under the trust fund recovery penalty, one of the IRSâs strictest enforcement measures.

This article will guide employers through the steps required to accurately calculate employer payroll taxes, understand reporting requirements, meet each federal tax withholding deadline, avoid unnecessary penalties, and resolve existing tax liabilities. For international employers or self-employed professionals engaging U.S. workers, compliance with federal tax law is not optionalâit is essential to operating legally and sustainably.

Understanding Unpaid Federal Payroll Taxes

Unpaid federal payroll taxes are amounts employers must withhold from employeesâ paychecks and deposit with the Internal Revenue Service, but fail to submit by the designated due date. These include federal income taxes, social security tax, medicare taxes, and the additional medicare tax. The IRS classifies part of these amounts as trust fund taxes because the employer holds these funds on behalf of the government and essential federal programs until payment is completed.

Employers face enforcement when they fail to deposit withheld payroll taxes accurately or on time. Common causes include cash flow issues, mismanagement, or diverting withheld funds for operational expenses. Below are the main tax obligations employers must handle:

- Federal income taxes are withheld from each employeeâs paycheck.

- The employer and employee share social security and medicare taxes.

- An additional medicare tax for employees earning above a set threshold.

- Federal unemployment tax is paid solely by the employer.

- Timely deposits made using IRS-approved forms and schedules.

Failure to meet these obligations can result in immediate penalties, accrued interest, and enforcement actions such as liens or levies. The IRS treats these violations seriously, mainly when employers collect funds from employees and fail to turn them over.

One of the strictest enforcement tools is the trust fund recovery penalty, which holds individuals personally responsible for failing to remit withheld trust fund taxes. This includes business owners, executives, or payroll service providers who neglect their duties. For a complete overview of how the IRS applies this penalty and who can be liable, visit the Trust Fund Recovery Penalty â IRS Overview.

Proper payroll tax withholding is not just a routine taskâit is a legal duty tied to the financial integrity of national programs like social security benefits and unemployment programs. Employers must treat these responsibilities with the seriousness they deserve to avoid long-term legal and economic consequences.

Calculating and Withholding Payroll Taxes

Accurate payroll tax calculation is a legal responsibility that every employer must meet. Federal law requires employers to withhold specific taxes from their employeesâ wages and remit the withheld amounts and their share of taxes to the Internal Revenue Service. This includes federal income taxes, social security, medicare taxes, the additional medicare tax, and federal unemployment tax. These obligations apply regardless of business size and must be handled correctly to avoid penalties and enforcement actions.

Employer vs. Employee Contributions

- Employers calculate federal income tax withholding based on IRS guidelines using either the wage bracket or percentage methods.

- The employee and the employer pay equal shares of Social Security and medicare taxes.

- The additional Medicare tax applies to employees earning over a specific income threshold and is withheld only from the employee; the employer does not match it.

- The employer pays the full federal unemployment tax, based on each employeeâs wages up to the annual wage base limit.

- Self-employed individuals must pay the employer and employee shares of these taxes through estimated quarterly tax payments.

Key Tax Categories and Withholding Responsibilities

- Federal income taxes must be withheld from employeesâ gross pay and deposited using IRS deposit schedules.

- Social security tax has a wage ceiling, and contributions stop once the employee meets the annual wage base limit.

- Medicare tax has no wage limit, and all earnings are taxed accordingly.

- Additional withholding may apply if an employee requests it on their Form W-4.

- Employers generally rely on payroll service providers to handle calculations, but remain legally responsible for accuracy and timely deposits.

Calculating employer payroll taxes correctly can cause financial and legal problems, including interest charges and penalties. Accurate tax withholding supports government programs like Social Security benefits and unemployment programs. Employers managing U.S.-based employees must stay updated on payroll tax rules, verify all calculations regularly, and meet every due date for tax deposits to remain compliant.

Reporting Payroll Taxes to the IRS

Once employers calculate and withhold payroll taxes, they must report these amounts to the Internal Revenue Service using specific federal forms. Reporting ensures that the IRS and the Social Security Administration correctly track employees' wages, withholdings, and contributions. Failure to report accurately or on time can disrupt social security records, delay tax credits, and trigger enforcement actions or financial penalties.

IRS Forms for Reporting

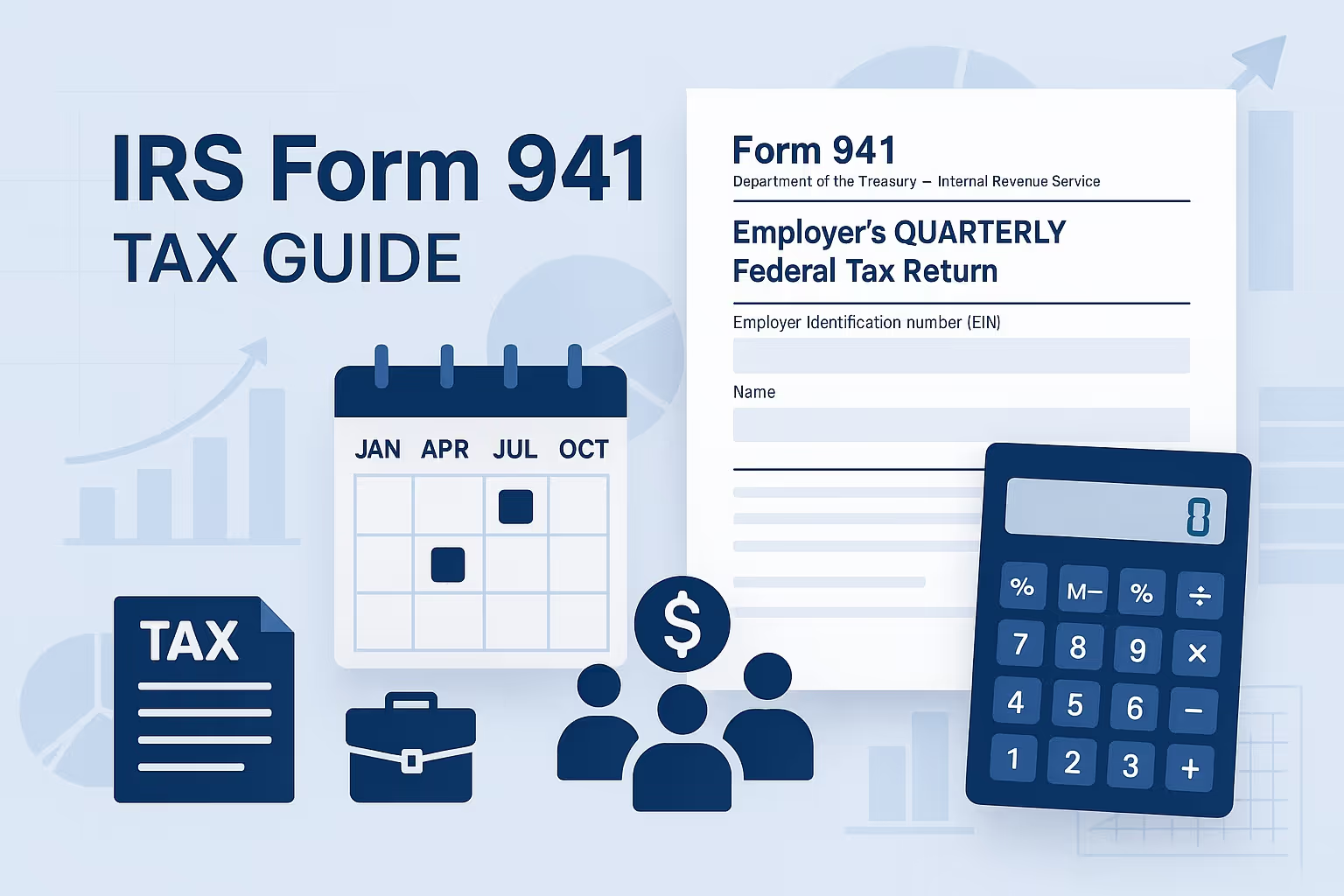

- Employers submit Form 941 quarterly to report federal income tax, social security tax, and medicare taxes withheld from employeesâ wages. Instructions and updates are on the IRS website: Form 941 â Employerâs Quarterly Federal Tax Return.

- Form 940 is filed annually to report federal unemployment tax, based on each employeeâs wage base and any allowable credits.

- Form W-2 must be provided to each employee annually, summarizing total wages and withheld taxes.

- Form W-3 is the transmittal for all W-2s filed with the Social Security Administration.

- Self-employed individuals use Schedule SE attached to Form 1040 to report and pay their employment taxes.

Penalties for Late or Incorrect Reporting

- Missing a tax deposit due date may lead to immediate penalties and daily interest accrual.

- Inaccurate wage reporting can result in mismatches with federal records, delaying processing and potentially harming employeesâ social security benefits.

- Repeated reporting errors may prompt audits, levies, or federal tax liens.

- Incomplete or incorrect submissions increase the risk of rejected filings and potential civil penalties.

- Employers generally remain fully responsible for the accuracy of filings, even when working with payroll service providers.

Proper payroll tax reporting is essential to maintaining federal tax compliance and supporting public programs such as unemployment insurance and social security. Employers must follow all due dates, confirm data accuracy, and file forms using approved methods. Staying current on IRS requirements helps businesses avoid costly errors and reinforces the financial integrity of their payroll systems.

Understanding the Federal Unemployment Tax

Employers pay the federal unemployment tax, or FUTA, solely to support the federal government's unemployment compensation programs. It is not deducted from employeesâ wages. Employers who meet certain thresholds must calculate, report, and pay this tax annually to the Internal Revenue Service using specific guidelines and deadlines to avoid penalties and maintain compliance.

Employer Liability and Wage Thresholds

Employers generally owe FUTA tax if they paid $1,500 or more in total wages during any calendar quarter or had at least one employee working for any part of a day in 20 or more different weeks in a year. This applies even if the employee was part-time or temporary.

Wage Base and Tax Rate

The FUTA tax applies only to the first portion of wages paid to each employee, known as the annual wage base limit. Once an employeeâs wages exceed this limit, no additional FUTA tax is owed for that year. The standard FUTA rate is 6.0%, but employers may qualify for a credit of up to 5.4% if they also pay state unemployment tax on time, reducing their effective rate to 0.6%.

Reporting and Coordination with State Tax

FUTA is reported annually using Form 940. Depending on the total amount owed, quarterly deposits may be required. Coordination with state unemployment tax is essential, especially in states with credit reductions, which can increase the employerâs FUTA liability.

The federal unemployment tax plays a critical role in sustaining unemployment programs nationwide. Employers must remain aware of wage thresholds, reporting rules, and payment deadlines to meet their obligations and avoid unnecessary penalties.

IRS Enforcement and the Trust Fund Recovery Penalty

When employers fail to deposit required payroll taxes, the Internal Revenue Service initiates enforcement procedures to collect the unpaid amounts. These include federal income taxes withheld from employees, social security taxes, Medicare taxes, and the additional Medicare tax. Since these are classified as trust fund taxes, the IRS considers nonpayment a serious breach of responsibility. Employers collect these taxes on behalf of the federal government, and failing to remit them places both the business and its leadership at risk.

Initial IRS Enforcement Measures

- The IRS first issues a Notice and Demand for Payment outlining the unpaid tax liability and requesting immediate resolution.

- If the employer fails to respond, the IRS may file a federal tax lien against business property or assets.

- The agency may also issue a levy, seizing business bank accounts or incoming payments to satisfy the debt.

- Interest and penalties begin accruing immediately until the balance is paid in full.

- Prolonged noncompliance may lead to the business's seizure of inventory, equipment, or other assets.

Trust Fund Recovery Penalty (TFRP)

- The TFRP applies when an individual is responsible for collecting or paying trust fund taxes and willfully fails to do so.

- Business owners, payroll service providers, financial managers, or employees with control over economic decisions may be subject to the penalty.

- Willfulness is the voluntary, intentional failure to deposit taxes after becoming aware they are owed.

- The penalty is equal to the trust fund portion of unpaid payroll taxes, including withheld federal income taxes and the employeeâs social security and Medicare.

- The IRS may collect this penalty directly from the responsible individualâs wages, bank accounts, or personal property.

Employers can often avoid aggressive enforcement by acting quickly once a notice is received. The IRS provides several payment plan options for qualifying taxpayers, including access to the IRS Online Payment Agreement Tool, which allows businesses to request structured repayment arrangements. Prompt action, accurate recordkeeping, and early communication with the IRS are key to minimizing risk and resolving payroll tax issues efficiently.

Setting Up Payment Plans with the IRS

When full payment of unpaid federal payroll taxes is not possible, the Internal Revenue Service offers payment plans to help employers meet their obligations without facing immediate enforcement actions. These plans, also known as installment agreements, provide structured repayment options for businesses that need more time to settle their tax liability. Applying for a plan when financial hardship is identified can prevent penalties from escalating and reduce the risk of federal tax liens or levies.

Payment Plan Options Available

- Short-term payment plans allow businesses to pay their tax balance in full within 180 days. No setup fee is charged, though penalties and interest continue to accrue until paid.

- Long-term installment agreements are available for businesses that need more than 180 days. These agreements require monthly payments based on the taxpayerâs financial capacity.

- The In-Business Trust Fund Express Installment Agreement is available to employers who owe $25,000 or less in trust fund taxes and can pay the full amount within 24 months.

- Direct debit arrangements are required for businesses with debts between $10,000 and $25,000 and are recommended for reducing the risk of default.

- Low-income businesses may qualify for reduced or waived setup fees, depending on income thresholds and eligibility.

How to Apply and Modify Agreements

- Employers can apply for payment plans using the IRS Online Payment Agreement Tool, which offers faster processing and lower setup fees than phone or mail applications.

- Phone applications are available through IRS business support lines and are appropriate for more complex cases or businesses that do not qualify online.

- Paper applications using Form 9465 and applicable financial statements can be submitted by mail, but typically involve higher fees and slower approval.

- Agreements can be modified if the employerâs financial situation changes, including adjustments to payment amounts or bank account information for direct debit payments.

- Employers must remain current with all future tax obligations to avoid defaulting on an approved agreement.

Setting up a payment plan does not eliminate tax liability but provides an opportunity to regain compliance and avoid enforcement. Employers who follow through on their payment commitments, file all required forms on time, and make timely tax deposits can gradually resolve payroll tax debts while maintaining business operations.

Frequently Asked Questions

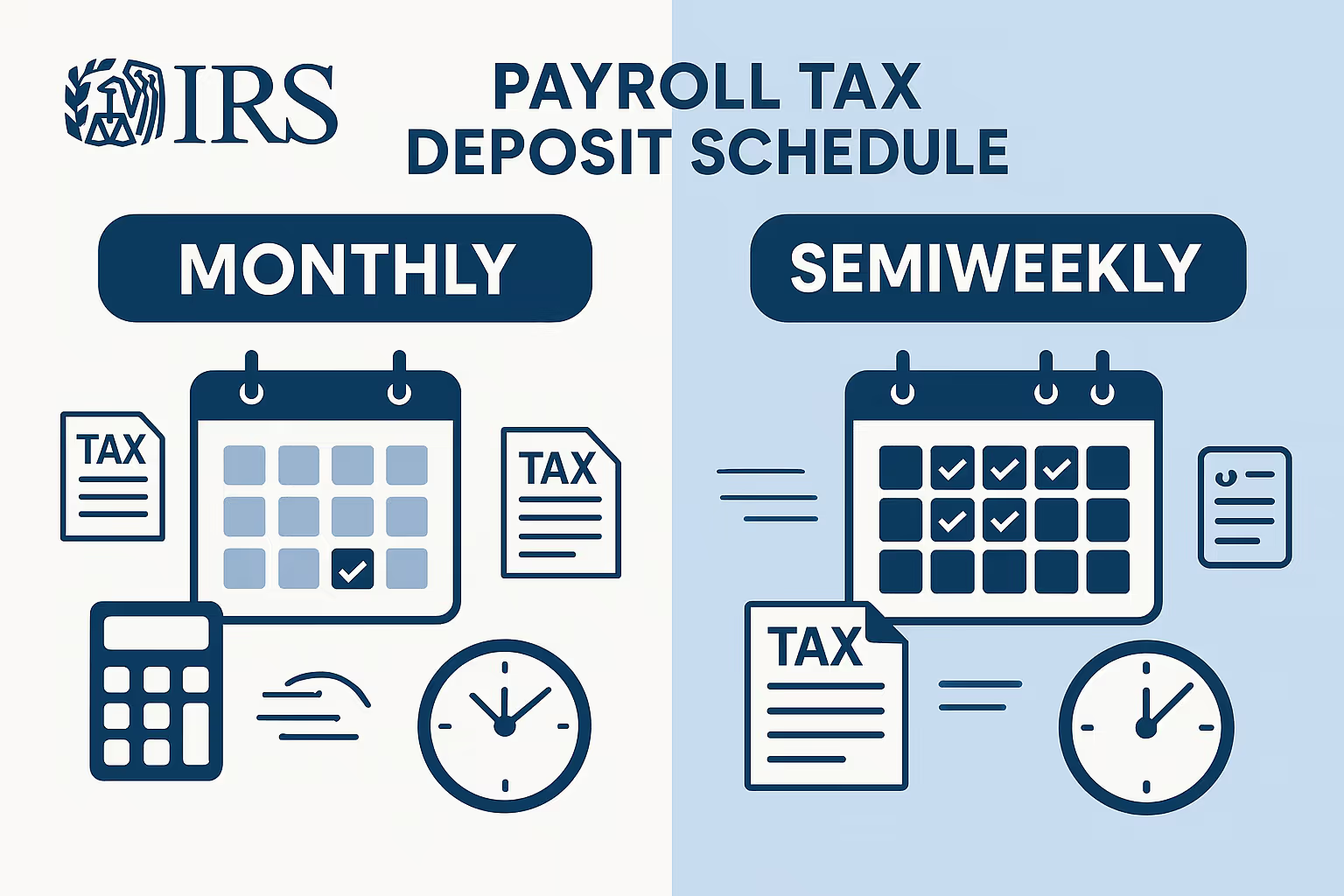

What is the due date for federal payroll tax deposits?

Federal payroll tax deposit due dates depend on your deposit scheduleâmonthly or semiweekly. Monthly depositors pay by the 15th of the following month, while semiweekly filers pay within one to three business days after payday. The IRS expects employers to calculate payroll taxes correctly and use specific forms such as Form 941. Missing deadlines leads to penalties and interest. Consulting a tax professional ensures compliance with deposit rules, especially for businesses managing multiple payroll cycles or reporting frequencies.

How is the additional Medicare tax calculated for high earners?

The additional Medicare tax applies to employees earning over $200,000 in a calendar year. Employers must calculate payroll taxes and withhold a further 0.9% on wages exceeding this threshold. There is no employer match. This tax must be reported on specific forms, and the amount should appear on the employeeâs tax return. Accurate tracking and proper payroll software help avoid errors. A tax professional can assist in monitoring income thresholds and ensuring proper compliance with federal guidelines.

Can the IRS penalize foreign employers for unpaid federal payroll taxes?

Yes, foreign businesses with U.S.-based employees must follow IRS tax requirements. Failure to calculate payroll taxes accurately or submit a proper tax return using specific forms can result in penalties, liens, or the trust fund recovery penalty. The IRS does not exempt international employers from enforcement. Hiring a U.S.-based tax professional helps ensure proper deposit timing, correct forms, and accurate wage reporting, especially when employing remote workers or running payroll outside the United States.

What happens if withheld taxes are used for other expenses?

Withheld taxes must never be used for operational costs like rent, payroll, or supplies. These funds belong to the government and must be deposited in full. Using them elsewhere is considered willful noncompliance and may trigger the trust fund recovery penalty. This applies to all employers, including those managing agricultural employees. Employers are responsible for ensuring timely deposits and accurate documentation. Working with a tax professional helps ensure trust fund taxes are correctly handled and never misapplied.

Can FUTA credits reduce my federal unemployment tax rate?

Yes, employers may qualify for a FUTA credit of up to 5.4% by paying state unemployment tax on time, reducing the federal unemployment rate from 6.0% to 0.6%. If applicable, this applies to the first $7,000 of each employeeâs wages, including agricultural employees. The credit is claimed on Form 940. To benefit, employers must calculate payroll taxes carefully and meet all deadlines. A tax professional can assist with accurate reporting and coordination between state and federal requirements.

Do payroll errors affect employee social security benefits?

Yes, incorrect wage reporting or late filings may delay or reduce an employeeâs future Social Security benefits. The Social Security Administration uses wage data submitted via specific forms like Form W-2. Benefits may be miscalculated if totals are incorrect or submitted after the due date. These issues apply to all employees, including agricultural employees. Reviewing data within a few business days of processing payroll and consulting a tax professional can prevent reporting mismatches and long-term consequences for both employer and worker.

What is the best way to avoid enforcement if I fall behind on payroll taxes?

The best step is to contact the IRS immediately and apply for a payment plan. The IRS offers structured installment agreements that allow employers to pay over time. Using the IRS Online Payment Agreement Tool helps avoid delays and reduces paperwork. In the meantime, continue to file every tax return and meet current payroll deposit due dates. A tax professional can help you prepare financial documents, submit specific forms, and develop a strategy to avoid enforcement or penalties.

%2520What%2520Employers%2520Need%2520to%2520Know%2520About%2520IRS%2520Liability%2520and%2520Payment.avif)