Business owners operating in the United States, including those residing abroad, must legally withhold certain employment taxes from their employeesâ wages and submit those amounts to the Internal Revenue Service (IRS). These withheld taxes, known as trust fund taxes, include federal income tax and the employee portion of Social Security and Medicare taxes. When these collected taxes are not paid to the IRS on time, the consequences can be severe. Under the U.S. tax code, the IRS may pursue the trust fund recovery penalty (TFRP), which allows the agency to hold responsible persons personally liable for the unpaid amount.

This penalty does not simply affect companies; it directly impacts individuals. The IRS can target those who exercise financial control over payroll decisions, even if they are not the business owners. A responsible party may lose personal assets if the agency determines they willfully failed to ensure proper tax payments. These liabilities can apply to executives, bookkeepers, payroll providers, and anyone with decision-making authority over federal tax deposits or payroll compliance.

Understanding the rules governing the TFRP is essential for any employer with staff in the U.S. Whether you manage tax payments directly or oversee a payroll service provider, this guide will outline your obligations, risks, and available options to help you remain compliant and avoid personal financial exposure.

What Are Trust Fund Taxes?

Trust fund taxes are amounts withheld from employeesâ wages that employers are legally obligated to remit to the Internal Revenue Service. These taxes are not the employerâs funds; they are collected on behalf of the federal government. When wages are paid to employees, the employer assumes a fiduciary responsibility. If these withheld amounts are not deposited on time, the IRS may impose the Trust Fund Recovery Penalty, which holds specific individuals personally liable for the unpaid amount.

The following tax components are categorized as trust fund taxes:

- Federal income tax withheld from employee wages

- The employee share of Medicare taxes

- Social Security taxes are withheld from employees.

- Withheld income collected during each payroll cycle

- Certain employment taxes are reported on IRS Forms 941 and 944

- withheld taxes that remain unpaid by the deposit deadlines

- Collected taxes that should be submitted to the IRS

- Tax payments are deducted from employee wages.

- Payroll taxes recorded but not yet remitted.

- Funds intended for federal tax deposits only

Employers must understand that these funds are not business capital. They cannot be used to cover operating costs, loan repayments, or any other company obligations. Using trust fund amounts for any non-tax purpose places the businessâand those in controlâat risk of enforcement. The IRS treats such actions as a serious violation of federal tax law.

Employers often delegate payroll functions to third-party payroll providers. While outsourcing can help streamline operations, it does not eliminate legal responsibility. A business must submit every tax deposit accurately and on time. This includes regularly reviewing payroll records and confirming that all deposits match amounts withheld from employeesâ wages.

Failure to manage this duty may result in personal financial exposure. The IRS will pursue the responsible person if federal income tax, Medicare taxes, or other collected taxes are not deposited as required. Employers should treat every tax deposit with the same urgency as payroll itself. Doing so maintains compliance and protects the business and its leadership from severe penalties.

Employment Taxes and IRS Oversight

employment taxes are required contributions that businesses must withhold from employeesâ wages and remit to the IRS. These include amounts withheld from workers, such as federal income tax, Medicare taxes, and certain employer obligations. The IRS considers these collected taxes a fiduciary responsibility, and failure to pay them properly may lead to penalties or personal liability for those in control of payroll processes.

IRS Employment Tax Categories

- Federal income tax withheld from employee paychecks

- The employer and the employee share Social Security and Medicare taxes.

- Withheld income recorded on IRS Forms 941 or 944

- Certain employment taxes are based on seasonal or part-time employment.

- Tax payments are temporarily held before being deposited.

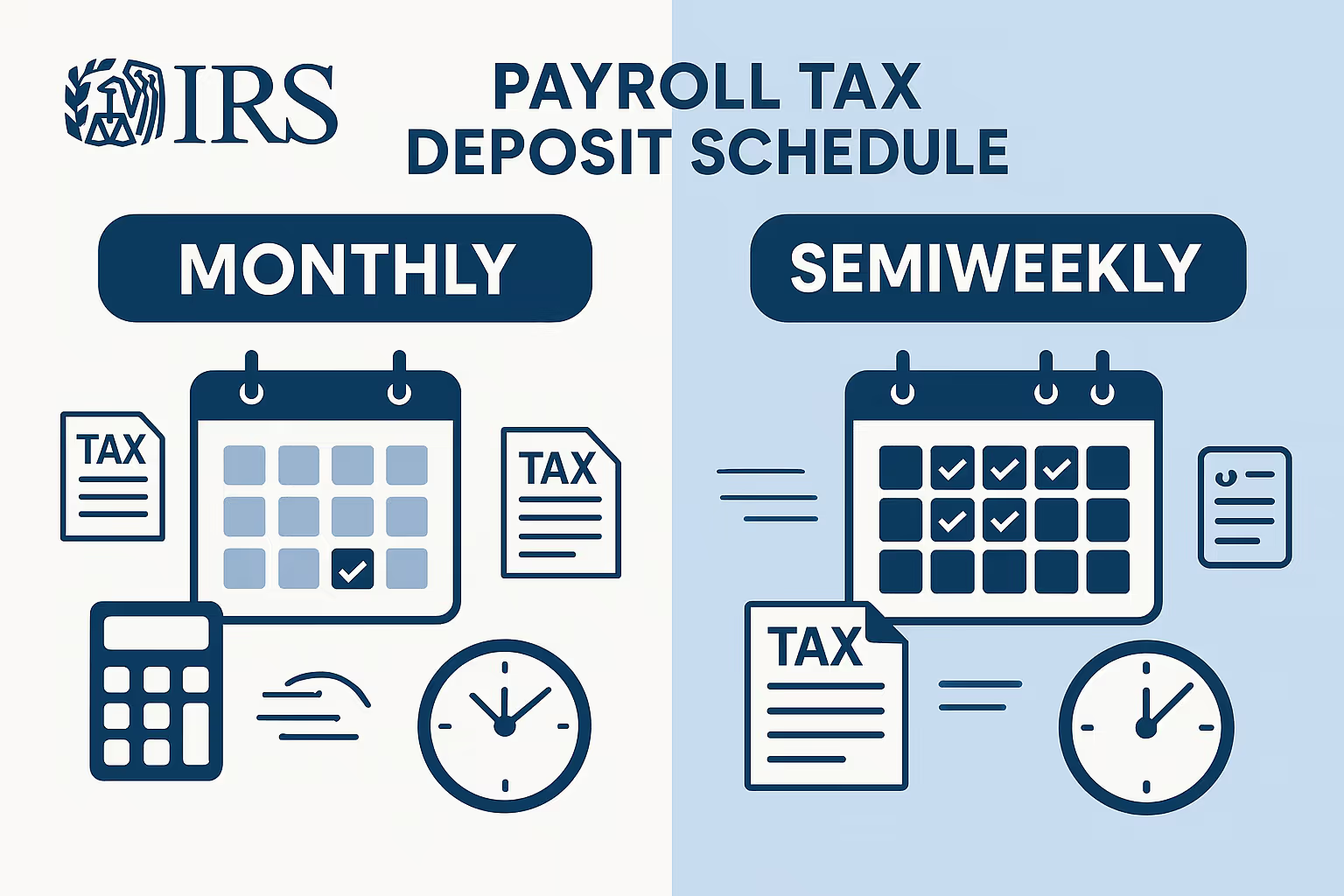

Payroll Deposit Obligations

- Required deposits must be submitted electronically through EFTP.S

- Schedules are either monthly or semi-weekly, based on payroll volume.

- Unpaid amount penalties apply when deposits are missed.

- Even when using payroll providers, employers remain responsible

- Frequent noncompliance may result in an IRS TFRP investigation.

Employers should review IRS Publication 15 (Circular E) to understand employment tax obligations in detail. This official guide outlines withholding, deposit rules, and employer responsibilities. Using third-party payroll service providers may help manage logistics, but oversight remains essential. Employers must regularly verify that tax deposits match the withheld taxes from employeesâ wages.

The IRS treats every tax deposit as a legal duty. Collected taxes are not business incomeâthey are public funds. Responsible parties must treat every deposit with urgency and care. Failure to comply may expose them to personal risk under the Trust Fund Recovery Penalty, especially if payments are delayed, incomplete, or mismanaged.

Who can be held personally Accountable for TFRP?

The Trust Fund Recovery Penalty allows the IRS to hold individuals personally responsible for unpaid trust fund taxes. This enforcement power applies to anyone with control over tax payments, regardless of ownership status. Liability is based on two factors: whether the person was responsible for ensuring payment of withheld taxes and whether they intentionally disregarded their obligation. The IRS defines this through the lens of actionânot job titles.

Key Signs of Responsibility

- Authority to direct or authorize payroll tax payments

- Ability to sign checks or access business accounts

- Control over deciding which creditors or obligations are paid

- Duty to manage payroll records or file tax returns

- active role in financial operations affecting withheld taxes

Common Responsible Parties

- Business owners or corporate officers

- Managing members of LLCs or partnerships

- Employees of payroll service providers involved in deposits

- Controllers, CFOs, or finance managers with operational authority

- Individuals who knowingly ignored IRS notices or ongoing tax issues

More than one individual can share responsibility. The IRS may assess the full unpaid amount to each responsible person, collecting from one or several until the balance is resolved. Employees may be liable if they managed payroll functions or made payment decisions, even if someone else signed the final check.

The IRS evaluates whether a person had the authority and the opportunity to prevent nonpayment. Use of a payroll provider does not protect responsible persons from liability. If someone knewâor should have knownâthat employment taxes were unpaid and failed to act, they may be held accountable under the tax code.

The financial risk is serious. Personal assets such as bank accounts or savings may be targeted to recover the amounts owed. During an IRS investigation, documents like bank statements and payroll records are used to prove involvement. Even without evil intent, the IRS will enforce the TFRP if the failure to pay is found to be willful or negligent.

â

Understanding the TFRP Investigation Process

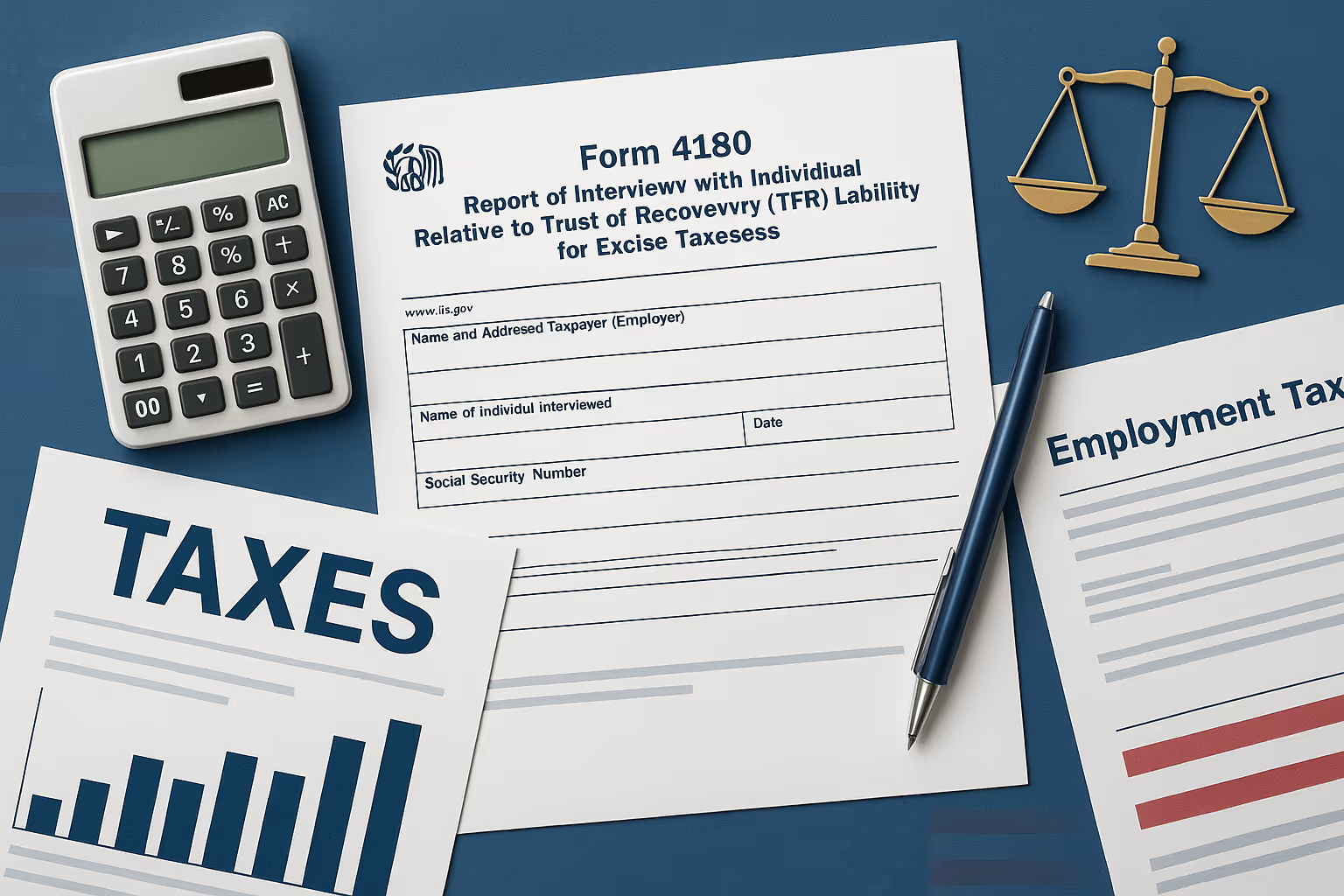

IRS Form 4180 and the Role of the Revenue Officer

The IRS begins most Trust Fund Recovery Penalty investigations by conducting an interview using IRS Form 4180. This form helps determine who qualifies as responsible and whether their failure to pay trust fund taxes was willful. A Revenue Officer leads the interview and asks about the individualâs involvement in payroll processes, tax decisions, and overall control of financial operations.

The questions aim to uncover whether the person authorized payroll, directed tax payments, or received IRS notices regarding unpaid trust fund taxes. The IRS may also inquire about access to business accounts, review of payroll records, and handling of federal tax deposits. Responses are documented and form part of the agencyâs evidence.

Evidence and Documentation Collected by the IRS

In addition to the interview, the IRS gathers supporting documentation to assess the unpaid amount. This includes payroll records, tax returns, internal emails, and bank statements. These records help determine whether collected taxes were deposited as required or withheld and misused. The penalty may be assessed personally when the agency finds that a responsible party intentionally disregarded these obligations.

Multiple individuals within a company may be considered responsible parties. The IRS will assess the situation based on actual financial control, not just titles. Those with authority over employeesâ wages or payment schedules may be liable, even if their role was not executive.

If a person is found responsible and their inaction was deemed willful, the IRS can assess the full unpaid amount under the TFRP. Personal assets such as wages, bank accounts, or property may be subject to collection. Anyone involved in tax decisions or payroll processing must be prepared to explain their actions and demonstrate they acted in good faith throughout the process.

Letter 1153 and Appeal Rights

What is Letter 1153?

Letter 1153 is the IRSâs formal notice informing an individual that it intends to assess the Trust Fund Recovery Penalty. It outlines the unpaid trust fund taxes and identifies the responsible person. The notice serves as an opportunity for the recipient to respond before the penalty becomes legally enforceable.

What Is the Deadline to Respond?

The IRS gives recipients 60 days to file a written protestâor 75 days if the letter is mailed internationally. Failing to respond in time results in immediate assessment and potential collection actions targeting personal assets. It is critical to act quickly and secure professional assistance.

What Should a Protest Contain?

The written protest must clearly state disagreement with the proposed penalty. It should include facts, references to the tax code, and supporting documents such as payroll records, tax returns, and bank statements. To be valid, it must be signed under penalty of perjury.

What Happens During the Appeal?

Once the protest is accepted, the IRS refers the case to its Office of Appeals. This division operates independently from IRS Collections. The appeals officer will review all evidence and allow the taxpayer to explain their position. A successful appeal can prevent assessment altogether.

Why Prompt Action Is Essential

If no protest is filed, the IRS can collect the full unpaid amount from the responsible parties. This may involve wage garnishments or seizure of personal accounts. Responding within the appeal window protects legal rights and may pause enforcement actions while the case is under review.

Legal Defenses Against the Trust Fund Recovery Penalty

Facing the Trust Fund Recovery Penalty does not automatically mean a person will be held liable. The IRS must determine that the individual was both a responsible person and acted willfully in failing to ensure trust fund taxes were paid. If either of these conditions is not met, the penalty should not apply. Employers and managers can defend against liability by providing documentation that shows a lack of authority, knowledge, or intent to disregard tax obligations.

Defenses Based on Lack of Responsibility

- The person had no control over payroll, tax payments, or the disbursement of collected taxes.

- They lacked access to payroll records or company bank accounts.

- Their role was clerical or ministerial, without decision-making power.

- They were not involved in preparing or submitting federal tax deposits.

- They were not aware that employment taxes had gone unpaid

Defenses Based on Lack of Willfulness

- The person relied on a payroll service provider or financial officer in good faith.

- They took reasonable steps to address tax issues once discovered.

- They did not intentionally disregard IRS rules or notices.

- Internal records show prompt efforts to resolve the unpaid amount.

- They were misled or excluded from communications regarding tax responsibilities.

These defenses must be supported by credible evidence to be effective. The IRS evaluates tax return filings, payroll records, bank statements, emails, and documented job duties to determine whether a person acted with control and awareness. General claims of misunderstanding or lack of involvement are not enough. The agency focuses on actual authority and behavior when taxes were withheld but not deposited.

Even when a person has some involvement in payroll, they may not be liable if they lack authority over tax-related decisions. Establishing that another individual was solely responsible, or that the accused party took appropriate actions upon learning of the issue, can be enough to avoid penalty assessment. A professional tax advisor can help prepare a fact-based defense supported by detailed records.

IRS Installment Agreements and Other Payment Options

Once the IRS assesses the Trust Fund Recovery Penalty, the individual becomes personally liable for the full unpaid amount. This liability is treated similarly to federal tax debts and may result in serious collection actions. Fortunately, the IRS offers payment solutionsâincluding installment agreementsâthat help taxpayers manage their obligations while protecting their assets.

Installment Agreements

- Enable responsible persons to repay the unpaid trust fund taxes over time through monthly payments.

- Require detailed financial disclosures, including income, payroll records, and bank statements.

- May trigger a federal tax lien to secure the governmentâs interest during repayment.

- Compliance with current and future federal tax deposits is mandatory throughout the term.

- Missed payments or new delinquencies can cause the agreement to default.

Taxpayers can apply online through the IRS Installment Agreement Page, which outlines available plan types and eligibility criteria. However, complex TFRP liability cases require manual review and professional assistance to structure a workable agreement.

Offer in Compromise and Alternative Resolutions

- An Offer in Compromise allows settlement of the total balance for less than the full amount owed.

- The Not Collectible status may temporarily suspend collections for those facing financial hardship.

- Before approval, the IRS evaluates all financial records, including tax returns and payroll data.

- Taxpayers must remain compliant with all future tax payments and reporting requirements.

- Ongoing federal tax deposits must continue without interruption, even under relief status.

These IRS programs are designed to help resolve debts while considering taxpayers' financial capacity. They allow responsible parties to avoid wage garnishment, bank levies, or property seizures, provided all terms are followed.

Individuals should consult a tax professional because trust fund penalties involve detailed financial and compliance analysis. The IRS reviews collected taxes, the responsible party's roles, and the financial documentation before granting relief. With the right approach, taxpayers can reduce their burden and protect their financial future.

Preventing Trust Fund Tax Problems Before They Start

Preventing Trust Fund Recovery Penalty exposure begins with proactive compliance. Employers must remember that trust fund taxes, such as withheld income and payroll deductions, are not operating funds. These are taxes collected from employees and held temporarily for the government. If misused or delayed, these amounts can result in personal liability under the tax code for any responsible person involved in financial oversight.

Strengthening Internal Controls

- Assign clear responsibility for submitting tax payments and monitoring payroll records.

- Use dual-approval systems for processing payroll and federal tax deposits.

- Keep a dedicated bank account for collected taxes to avoid misuse.

- Conduct routine internal audits to verify compliance with IRS deposit schedules.

- Maintain written procedures and support documentation, including bank statements.

Recognizing Early Warning Signs

- Receipt of IRS notices related to missed tax deposits or late tax returns.

- Payroll service provider inconsistencies or sudden changes in deposit practices.

- Cash shortages are causing delays in employeesâ wages or tax payments.

- Gaps between amounts withheld and what is reported on tax filings.

- Complaints from employees regarding incorrect or missing tax withholdings.

The IRS provides additional guidance in IRS Publication 784 â Understanding the TFRP, which outlines how to avoid personal liability through proper payroll tax management. Business owners working with third-party payroll service providers must stay involved. The IRS holds employers responsible, even when payroll is outsourced.

Implementing control measures, reviewing reports, and resolving discrepancies quickly reduces the risk of IRS action. Responsible parties who take early steps to ensure accuracy in federal tax deposits and payroll records can avoid costly penalties and protect their assets. Prevention is the most effective defense when dealing with trust fund taxes.

Frequently Asked Questions

What is the Trust Fund Recovery Penalty, and how is it calculated?

The Trust Fund Recovery Penalty equals the unpaid amount of withheld trust fund taxes, including federal income tax and the employee share of Medicare and Social Security. The IRS determines the liability by reviewing payroll records, tax return filings, and bank statements. If the employer withheld but did not deposit these funds, the IRS may assess the full amount against any responsible person involved in payroll, tax payments, or federal tax deposits.

Who qualifies as a responsible person under the TFRP rules?

A responsible person has authority over financial decisions involving employeesâ wages, tax payments, and payroll records. This can include business owners, corporate officers, controllers, and even payroll service provider staff. The IRS looks at actual authority and controlânot job titlesâto determine responsibility. Anyone who can direct or influence tax deposits or collected taxes may be personally liable for the unpaid amount under the federal tax code.

Can multiple individuals be held liable for the same unpaid trust fund taxes?

Yes, the IRS may assess the full unpaid amount to more than one responsible person. Though the total will be collected only once, any individual assessed can be pursued for full payment. The IRS does not allocate portions among responsible parties but seeks the most efficient recovery path. If one person pays the full balance, they may seek contributions from other liable parties through legal or civil channels.

Does using a payroll service provider remove liability?

No, while a payroll service provider may manage filings and tax deposits, the employer remains responsible for ensuring those deposits are made. If trust fund taxes are withheld from employeesâ wages but not paid to the IRS, the accountable person may still face the TFRP. The IRS does not consider outsourcing as a defense. Employers must review payroll records and confirm tax payments have been processed as required under federal tax deposit guidelines.

What documents support a TFRP defense?

Key documents that support a defense include payroll records, tax returns, internal correspondence, job descriptions, and bank statements. These materials help show whether a person had authority or acted willfully. Demonstrating a lack of control or proving that another party handled tax payments can reduce or eliminate liability. The IRS uses these documents during a TFRP investigation to assess whether collected taxes were mismanaged or improperly withheld from employees' wages.

What options are available if I canât pay the penalty?

Taxpayers may qualify for IRS installment agreements, Offers in Compromise, or Currently Not Collectible status. These options allow gradual repayment or partial settlement of the unpaid amount based on income, expenses, and assets. The IRS reviews financial disclosures, payroll records, and tax compliance history. Staying current with federal tax deposits and future returns is required to maintain eligibility. Seeking help from a tax professional improves approval chances and negotiation outcomes.

How do I appeal a proposed TFRP assessment?

After receiving Letter 1153, you have 60 days (75 if international) to file a written protest. This preserves your right to appeal the Trust Fund Recovery Penalty before the IRS finalizes the assessment. The protest must include your arguments, supporting facts, applicable tax code references, and documentation like payroll records or bank statements. Once accepted, the IRS Office of Appeals will review your case independently and issue a determination based on your submission.