For agricultural employers in the United States, complying with annual federal payroll tax obligations is essential. One of the most critical filings is IRS Form 943, designed specifically for employers who pay wages to farmworkers. This form allows agricultural businesses to report withheld federal income tax, Social Security tax, and Medicare taxes for the entire year. Unlike quarterly payroll forms used for non-agricultural workers, Form 943 is filed annually and reflects all applicable federal tax responsibilities related to farm labor. Employers can refer to the IRS Form 943 overview for official guidance.

Form 943 applies to employers who pay one or more farmworkers either a threshold amount in cash wages or a total annual payment across all workers. If either benchmark is met, the employer must file the formâeven if no taxes were withheld during the year. Agricultural employees, including seasonal workers and family members, often qualify under unique wage rules and exemptions, which makes understanding the requirements essential for compliance.

Filing IRS Form 943 correctly helps agricultural employers avoid penalties, ensure accurate records, and stay in good standing with the IRS. Understanding the federal income tax withheld rules, additional Medicare tax withholding, and total wages paid during the calendar year is vital before beginning the filing process.

Who Must File IRS Form 943?

IRS Form 943 is required for agricultural employers who meet certain wage thresholds when paying farmworkers. This form is specifically designed to report federal income tax withheld, Social Security tax, Medicare taxes, and any additional Medicare tax withholding related to agricultural labor. Filing is based on whether wages paid to agrarian employees meet one or both IRS-defined criteria during the calendar year.

Eligibility Tests

- $150 Per Worker Test

Employers must file Form 943 if they pay cash wages of $150 or more to any one farmworker during the year. Each employee, including family members, is considered individually. - $2,500 Combined Wage Test

If total cash wages and non-cash compensation paid to all agricultural employees combined reach $2,500 or more during the year, Form 943 is required.

Meeting either testâeven if only one is metâmakes filing mandatory. Both tests are independent of each other.

Special Rules and Exceptions

- Certain Hand Harvest Laborers

Depending on their employment arrangement, workers who are local, commute daily, and are paid less than $150 annually may be exempt from Social Security and Medicare taxes. - H-2A Visa Workers

While wages paid to H-2A workers must be reported, they are usually exempt from federal income tax withholding, Medicare, and Social Security taxes, unless voluntarily withheld. - Household Employees on Farms

Wages paid to household staff living in a private home on a farm may be reported on Schedule H rather than Form 943, depending on the workerâs role.

Once an employer begins filing IRS Form 943, it must be filed every yearâeven when no wages are paid or no taxes withheldâuntil a final return is submitted. Failing to comply with IRS filing requirements can result in penalties and increase your businessâs tax liability. Agricultural employers should keep accurate payroll records and consult a qualified tax professional when eligibility is unclear.

Wages and Taxes Reported on Form 943

IRS Form 943 requires agricultural employers to report specific wage types and tax obligations for farmworkers. Understanding which payments are taxable and how different taxes apply is essential for filing an accurate form and avoiding compliance issues. This includes tracking the total wages paid and the taxes withheld throughout the calendar year.

Types of Reportable Wages

- Cash wages: include hourly, salaried, and piecework payments made directly to farmworkers. These are subject to all federal employment taxes and determine whether Form 943 must be filed.

- Non-cash wages, such as food, lodging, or goods, are counted toward the $2,500 wage test but may not be taxable for Social Security or Medicare.

- Taxable fringe benefits, such as bonuses, personal use of farm vehicles, or housing allowances, are subject to income and payroll taxes unless specifically excluded.

- Sick pay, including employer-paid or third-party ill leave, is reportable if it qualifies as taxable compensation under IRS rules.

- Family leave wages: must be included when paid, unless exempt. These are subject to Social Security and Medicare taxes.

Taxes to Report

- Federal income tax withheld: must be reported, even if the amount is zero. This shows compliance with withholding obligations.

- Social Security tax applies to wages up to the annual cap, with the required employee and employer portions.

- Medicare taxes: apply to all wages without a cap. Both the employee and employer contribute equal shares.

- Additional Medicare tax withholding must be applied to wages above $200,000 per employee per year. The employee pays this tax, but the employer withholds it.

Accurate reporting of these items is critical to remaining in good standing with the IRS. Employers must determine whether all compensation types are taxable and ensure taxes are correctly calculated and deposited. Total wages paid, uncollected employee share amounts, and the correct amount of tax liability should match supporting payroll records. This section of Form 943 must be completed carefully to reflect what was earned and what taxes were withheld or owed for the entire year.

How to Complete IRS Form 943 Step-by-Step

Completing IRS Form 943 requires precise information about agricultural wages, taxes withheld, and deposits made throughout the tax year. This form reports federal income tax, Social Security tax, Medicare taxes, and additional Medicare tax withholding for agricultural employees. Employers must gather complete payroll records before filling out the form to ensure each entry is accurate.

Preparation and Required Information

- Employer identification number: Use only the EIN issued by the IRS. Do not enter a Social Security number or other personal ID.

- Payroll records: Confirm total wages paid to all agricultural employees. Include cash wages, taxable fringe benefits, family leave, and third-party sick pay.

- Federal income tax withheld: Check year-end reports to calculate the full amount withheld from employeesâ wages over the entire year.

- Adjustments from previous period: Prepare documentation for any prior-year corrections or adjustments due to rounding errors, sick pay, or sick leave misreporting.

Completing the Main Lines

- Line 1: Enter the number of agricultural employees working during the pay period, including March 12.

- Line 2: Report the total cash wages subject to Social Security tax.

- Line 3: Multiply Line 2 by 12.4% to calculate the Social Security tax owed. This includes both the employer and employee shares.

- Line 4: Enter the total wages subject to Medicare taxes. There is no wage cap for this amount.

- Line 5: Multiply Line 4 by 2.9% to determine the Medicare tax due. This also includes both the employer and employee portions.

- Line 6: Identify wages subject to additional Medicare tax withholding, which applies when an employeeâs annual wages exceed $200,000.

- Line 7: Multiply Line 6 by 0.9% to calculate the additional Medicare tax. Only the employee pays this amount, but the employer must withhold and report it.

- Line 8: Enter the total federal income tax withheld from all agricultural employees during the calendar year.

Final Tax Calculations

- Line 9: Add Lines 3, 5, 7, and 8 to calculate total taxes owed before adjustments.

- Line 10: Enter any rounding-related adjustments, group-term life insurance, or third-party sick pay corrections.

- Line 11: Add or subtract adjustments to find total taxes after corrections.

- Line 12: Report any tax credit for qualified research if applicable.

- Line 13: Subtract any credits from total taxes to get the net liability.

For line-by-line guidance and current rates, refer to the official instructions for Form 943 on the IRS website. Employers may also consult a tax professional or payroll service provider to confirm totals and ensure accurate reporting.

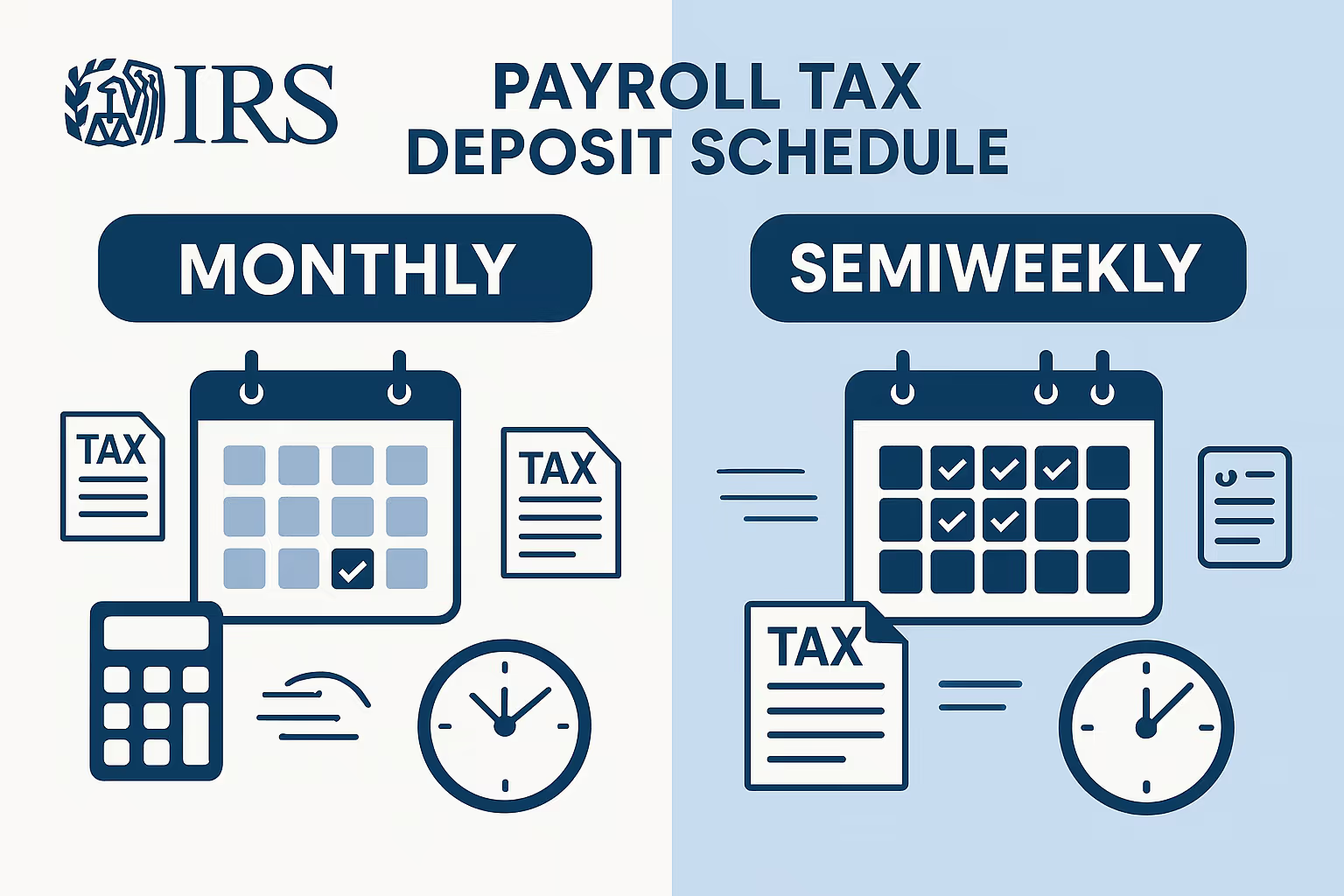

IRS Deposit Rules and Deadlines

Understanding IRS deposit rules is essential for agricultural employers filing Form 943. Employers must deposit taxes for federal income tax withheld, Social Security tax, Medicare taxes, and additional Medicare tax withholding. The deposit schedule depends on the tax liability during a specific IRS-defined lookback period.

Monthly and Semiweekly Deposit Schedules

- Monthly schedule depositor: If your total tax liability during the lookback period is $50,000 or less, you must deposit all taxes by the 15th day of the month following the month wages are paid.

- Semiweekly schedule depositor: If your total liability exceeds $50,000, your deposits are due semiweekly. Taxes for wages paid on Wednesday, Thursday, or Friday must be deposited by the following Wednesday. The due date is the following Friday for wages paid on Saturday, Sunday, Monday, or Tuesday.

The lookback period runs from July 1 of the second prior calendar year through June 30 of the previous year. It determines your deposit frequency for the current tax year.

Additional Deposit Rules

- $100,000 next-day deposit rule: If your accumulated liability reaches $100,000 on any day, you must deposit the entire amount by the next business day, regardless of your regular deposit schedule.

- Annual liability under $2,500: If your total yearly taxes are less than $2,500, you can pay the full amount with your return, using a check or money order.

- Overpayment applied or refunded: If you overpay your tax, you can use the excess for the following yearâs liability or request a refund from the IRS.

All deposits must be made using the Electronic Federal Tax Payment System (EFTPS). This system allows employers to schedule payments in advance and keep records of deposit confirmations. Failing to deposit taxes on time may result in penalties, even if the full amount is eventually paid. Employers should match their tax liability with the correct deposit schedule and payment deadlines throughout the year.

Paper Filing vs. E-Filing Form 943

Agricultural employers have two options for submitting IRS Form 943: mailing a physical form or filing electronically. Choosing the correct method can affect processing time, error rates, and compliance. While the IRS accepts both options, e-filing is increasingly recommended for accuracy, speed, and convenienceâespecially for employers managing high volumes of payroll data.

Paper Filing Requirements

- Employers who mail Form 943 must use the correct mailing address based on their business location.

- The completed form must include all required fields. Forms with missing information or errors may be rejected or delayed.

- Paper filers must also include payment if taxes are due and not already deposited. This can be sent by check or money order along with the return.

- Remember to retain a copy of the completed form and proof of mailing for your records.

Benefits of E-Filing

- Electronic filing provides faster processing and immediate confirmation of receipt by the IRS.

- Errors such as missing fields, incorrect amounts, or invalid EINs are less likely, as many e-file systems validate entries before submission.

- Employers can use tax software or work with a payroll service to file Form 943 directly through the IRS-approved e-file system.

- E-filing is especially useful for those using a payroll service provider, as it streamlines communication between payroll data and the IRS.

- Employers who e-file also receive digital confirmation, making tracking submissions easier and avoiding late penalties.

Whether choosing to file electronically or by paper, employers must ensure the correct amount is reported and submitted by the due date. Late or inaccurate filings may result in penalties, even if taxes were already paid. Using a paid preparer or tax professional may help verify totals and provide guidance on the most efficient filing method. Regardless of the technique, keeping accurate payroll, deposits, and return submissions records is essential for IRS compliance during the tax year.

Common Filing Errors and How to Avoid Them

Many agricultural employers encounter avoidable errors when completing IRS Form 943. These mistakes can result in penalties, delayed processing, or mismatches in tax records. Understanding how to file IRS Form 943 accurately begins with identifying the most common filing pitfalls.

Common Errors

- Incorrect total deposits: The IRS compares deposits to reported tax liability. A mismatch may trigger a notice or correction request.

- Federal income tax withheld, missing, or misreported: Line 8 must be filled out to reflect that, even if zero tax was withheld. Leaving it blank is a common mistake.

- Misreporting taxable fringe benefits subject to tax: Benefits like housing, vehicle use, or bonuses are often taxable. These must be included in total wages paid.

- Submitting the wrong tax return form: Form 943 is required for agricultural employees. Filing Form 941 or 944 instead may result in misapplied taxes.

- Not using a paid preparer when needed: Employers managing multiple adjustments or operating across states should consider working with a professional to ensure accuracy.

Prevention Strategies

Double-check all payroll data before filing. Confirm that wages subject to Social Security and Medicare taxes, additional Medicare tax withholding, and total wages match supporting records. The IRS expects consistency across forms and deposits. Review the entire tax return carefully. Ensure all fields are complete and accurate and reflect actual wages and liabilities for the calendar year. If using software or a payroll service provider, verify data entries before submission. Refer to IRS penalty guidance for filing errors and their consequences. Accurate filing reduces the risk of errors, improves IRS processing, and helps ensure full compliance with tax obligations.

Special Situations for Agricultural Employers

Some agricultural employers operate under unique circumstances that affect how they report wages and taxes on Form 943. Whether you employ household workers on a farm, active members of the armed forces, or manage farm operations across multiple states, you must understand how these factors influence your filing and federal tax obligations.

Household Employees on Farms

- Employers may have household staff working in a private home on their farm. Depending on their role and wage structure, these employees can be reported on Form 943 or separately on Schedule H.

- If you choose not to include household employees on Form 943, you must use the appropriate schedule to report their wages as part of your tax return.

Multiple Employer Scenarios

- Some farm businesses operate in multiple states or partner with other employers. In these cases, detailed records of each employee's wages and which employer is responsible for withholding and depositing taxes are essential.

- Each employer must report wages separately, and the correct amount of federal tax must be paid for each worker.

Armed Forces and Crew Leaders

- Wages paid to active members of the armed forces performing agricultural work may follow special rules depending on employment classification.

- You must determine the legal employer if you work with a crew leader. If the crew leader supplies labor and pays the workers, they may be the responsible partyânot the farm operator.

Stopping Operations Mid-Year

- If you stop paying wages during the calendar year and do not expect to resume, you must file a final return. Check the box on Form 943 indicating it is your last filing, and include the date you ceased operations.

- Maintain your payroll records for at least four years after submitting the final return.

Employers managing these special situations should consult a tax professional to ensure proper handling of payroll, recordkeeping, and reporting obligations for agricultural employees under federal tax law.

Frequently Asked Questions

What is the purpose of IRS Form 943?

IRS Form 943 reports payroll taxes for agricultural employees, including federal income tax withheld, Social Security, Medicare, and additional Medicare tax withholding. Employers file it annually to report taxes on wages paid to farmworkers. Filing ensures compliance with federal requirements and accurate credit for employee contributions. Unlike Form 941, which applies to non-farm workers, Form 943 is specifically for farms and agricultural labor. It applies to both seasonal and full-time workers.

How do I know if Iâm required to file?

You must file IRS Form 943 if you paid any farmworker cash wages of $150 or more during the year, or if total wages to all agricultural employees exceeded $2,500. If either condition is met, filing is requiredâeven if no federal income tax was withheld. This rule ensures accurate tracking of federal tax obligations and helps avoid underreporting penalties. Farm employers must assess these thresholds annually based on their payroll records.

What happens if I file Form 941 or 944 instead?

Filing Form 941 or 944 instead of Form 943 is incorrect for farmworkers. The IRS may misapply your federal tax deposits or consider your tax return incomplete. Using the wrong form can delay processing, lead to penalties, or cause confusion regarding tax liability. Always use Form 943 when reporting wages for agricultural employees. Review worker classifications and refer to IRS instructions to ensure you file the proper return for your business type.

Is an additional Medicare tax required for farmworkers?

If an employee earns over $200,000 during the year, employers must withhold additional Medicare tax at 0.9% on wages exceeding that amount. This applies even for agricultural employees, though the employer does not pay a matching portion. The employer is, however, responsible for correct additional Medicare tax withholding and timely deposits. Failure to withhold or report this properly can lead to IRS penalties and interest charges, even when only one worker qualifies.

What if I close my business or stop paying wages?

You must file a final return when you stop paying wages and do not plan to continue operations. Check the box on Form 943 to indicate itâs your last return, include the final payroll date, and submit all taxes due. Employers must also retain payroll records for at least four years after filing the final return. Filing a proper final return prevents future IRS notices or assumed ongoing liability for employment tax deposits.

Can I file Form 943 electronically?

Yes, IRS Form 943 may be e-filed using approved tax software or through a paid preparer. E-filing ensures faster processing, immediate confirmation of receipt, and reduced errors compared to paper filing. Itâs instrumental if you use a payroll service provider. Electronic filing helps meet deadlines efficiently and ensures that your federal income tax withheld, Social Security, and Medicare taxes are correctly submitted and recorded for each tax year.

%2520What%2520Employers%2520Need%2520to%2520Know%2520About%2520IRS%2520Liability%2520and%2520Payment.avif)