Understanding payroll tax compliance is a fundamental responsibility for all businesses operating in the United States. Employers must manage federal employment tax compliance to meet legal standards and protect their employeesâ financial futures and business operations. These responsibilities include accurate tax filing, proper payment scheduling, and timely submission of required forms to the Internal Revenue Service.

Employer payroll taxes include multiple components such as withheld federal income tax, social security tax, medicare taxes, and the employerâs share of employment taxes. In addition to these standard requirements, employers must comply with federal unemployment tax rules, which the Federal Unemployment Tax Act governs. Businesses must calculate employer payroll taxes correctly each pay period to ensure all taxes withheld align with the current federal income tax rates and due dates. Failing to do so can result in serious interest charges and penalties from the Internal Revenue Service.

Employment taxes apply to both the employer and the employee, affecting wages, benefits, and long-term financial reporting. Most employers are required to report payroll taxes regularly, depending on their deposit schedule and tax liability. By adhering to federal tax withholding obligations, businesses maintain credibility and avoid significant consequences of payroll tax non-compliance.

Understanding Federal income tax withholding

Federal income tax withholding is one of the most important aspects of federal employment tax compliance. Employers are required to withhold a portion of each employeeâs wages and remit it to the Internal Revenue Service. This system ensures that employees pay their federal income tax gradually throughout the year rather than in a single payment during tax season. The amount to be withheld is determined by the employeeâs Form W-4, which outlines their filing status, dependents, and additional withholding requests.

Businesses must consider employee details and IRS-provided tax tables to calculate employer payroll taxes accurately. The official withholding instructions and percentage methods are available through IRS Publication 15 (Circular E), which is updated annually. Employers must ensure the correct amount is withheld each pay period and deposited promptly to the United States Treasury.

- Payroll tax withholding applies to wages, salaries, bonuses, and commissions paid to employees.

- Withholding amounts vary depending on income level, filing status, and Form W-4 selections.

- The Internal Revenue Service updates withholding guidelines annually, and employers must apply changes promptly.

- Employers are responsible for timely calculating, collecting, and depositing withheld federal income tax.

- Most employers follow monthly or semiweekly deposit schedules, depending on their total tax liability.

Employers must also report payroll taxes accurately using IRS forms and adhere to due dates to avoid penalties. This includes tracking the employerâs and employeeâs share of total tax liability.

- Businesses must file tax returns like Form 941, reflecting all withheld taxes for the reporting period.

- Interest charges may apply for late deposits or underpayments.

- Employers should document withheld amounts each pay period and verify accuracy before depositing.

- Employers generally do not receive tax credits on withheld income tax, but must report it fully.

- Most employers are required to submit withheld amounts electronically and maintain thorough records.

Meeting federal tax withholding requirements protects both the business and its employees. Ensuring timely deposits and accurate reporting supports compliance and reduces the risk of audit or financial penalties.

social security and medicare taxes (FICA & Additional Medicare Tax)

Employers must comply with federal employment tax obligations by withholding social security and medicare taxes from employeesâ wages and contributing an equal employerâs share. These are known as FICA taxes under the Federal Insurance Contributions Act. These payroll taxes fund essential social security programs and Medicare services. Employers are responsible for accurate calculations each pay period and must deposit these taxes on time to the United States Treasury.

Standard Social Security and Medicare Taxes

- Employers must withhold social security tax at a rate of 6.2% from employees' wages, up to the annual wage base limit set by the Internal Revenue Service.

- The employer must also contribute a matching 6.2% amount, making the total social security tax 12.4%.

- Medicare taxes are withheld at 1.45% of all wages, with the employer contributing an additional 1.45%.

- There is no income cap on medicare taxes, so it applies to all taxable wages without limit.

- Employers generally include these taxes in each payroll run and ensure they are reported correctly to meet federal employment tax compliance standards.

Additional Medicare Tax Requirements

- The additional medicare tax applies to employees earning over $200,000 in a calendar year.

- Employers are required to withhold an extra 0.9% from the employeeâs wages above this threshold.

- Unlike the standard medicare tax, there is no employerâs share for the additional medicare tax.

- Employers must monitor cumulative employee earnings and apply the additional withholding in the correct pay period.

- Failing to withhold this tax can result in interest charges and significant penalties during IRS assessments.

The employer and the employee are responsible for their respective shares of these employment taxes. Employers must report payroll taxes on Form 941 and keep detailed records to prove compliance. Calculating these taxes correctly helps employers avoid audit triggers and supports employee eligibility for future Social Security benefits. Most employers must deposit these taxes electronically and meet filing due dates. A strong payroll process that tracks employee and employer share helps reduce tax liability risks and ensures full compliance with federal tax withholding laws.

Employer Payroll Taxes and FUTA (Federal Unemployment Tax Act)

Employer payroll taxes include more than just social security and Medicare contributions. Businesses must also comply with the federal unemployment tax act (FUTA), which funds unemployment programs managed by the United States Treasury. Unlike other employment taxes, FUTA is paid entirely by the employerâno employeeâs share is involved. Compliance with FUTA requirements is essential for avoiding penalties and meeting federal employment tax compliance standards.

Understanding FUTA Liability and Payment Requirements

- The standard FUTA tax rate is 6.0% and applies to the first $7,000 of each employeeâs wages annually.

- Most employers qualify for a credit of up to 5.4% if they pay state unemployment tax on time, reducing their net federal unemployment tax rate to 0.6%.

- Employers must track employee wages carefully to determine when FUTA tax applies during each pay period.

- If the total undeposited FUTA tax exceeds $500 in any quarter, the employer must deposit by the IRS deadline.

- The Internal Revenue Service requires employers to report FUTA annually on IRS Form 940, using the IRS Form 940 Instructions to ensure accuracy.

Key Compliance Practices for Employers

- Most employers are required to deposit FUTA tax quarterly, even if their primary payroll schedule is monthly or semiweekly.

- Employers pay this tax independently of payroll tax withholding, which must be managed as part of broader employment taxes.

- Businesses that fail to calculate employer payroll taxes accurately may face interest charges and significant penalties.

- When filing, employers generally claim the state unemployment tax credit, which helps reduce overall tax liability.

- Reporting payroll taxes correctly ensures consistency across all employment tax obligations, including federal and social security taxes.

Employers must understand the relationship between state unemployment tax and FUTA when calculating total payroll tax responsibilities. Agricultural employees, household workers, and seasonal businesses may be subject to special FUTA rules requiring careful review. Keeping clear records each pay period and using accurate data to report payroll taxes supports long-term compliance.

By paying the correct amount on time and filing all required tax return forms, businesses fulfill their federal unemployment tax obligations and avoid audit risks. While often overlooked, FUTA compliance is vital in overall employer payroll taxes and federal employment tax enforcement.

Filing Employment Taxes: Required Forms and Deadlines

Filing employment taxes is a critical part of federal employment tax compliance. The Internal Revenue Service requires employers to report payroll taxes using specific forms and submit them by designated due dates. These filings account for withheld federal income tax, social security tax, Medicare taxes, and federal unemployment tax. Employers must report both the employeeâs and employerâs share accurately and on time to avoid interest charges and penalties.

Core Federal Forms for Payroll Tax Filing

- Form 941 is filed quarterly to report payroll taxes withheld from employees and the employerâs portion of social security and medicare taxes.

- Form 940 reports annual federal unemployment tax liability, including any adjustments based on state unemployment tax credits.

- Form 944 is used by certain small employers, who are allowed by the IRS to file once per year instead of quarterly.

- Form W-2 provides employees with a summary of wages and taxes withheld and must be issued by January 31.

- Form W-3 is the transmittal form accompanying W-2s sent to the Social Security Administration. It must follow the instructions for Forms W-2 and W-3 to ensure proper formatting and delivery.

Reporting Schedules and Filing Compliance

- Employers generally must file these forms electronically unless approved for paper filing.

- Due dates depend on the businessâs deposit schedule and total tax liability, with most employers following quarterly or annual deadlines.

- Accurate completion of each tax return form helps reconcile amounts deposited with the United States Treasury.

- Misreporting payroll taxes can result in significant penalties, even if taxes were correctly deposited.

- Employers must retain payroll documentation for each pay period, including wages, taxes withheld, and deposit confirmations.

Meeting filing requirements is separate from making payroll tax deposits. While deposits are usually due monthly or semiweekly, filing obligations follow a different schedule. Employers pay close attention to both components to remain compliant. Most employers must manage multiple tax forms and confirm that all data submitted aligns with payments made. Following the correct filing procedures helps ensure accurate federal tax withholding records and minimizes the risk of penalties or audit complications. Staying organized and timely is essential for complete and consistent employment tax reporting.

Calculating Employer Payroll Taxes and Using EFTPS

Employers are responsible for accurately calculating payroll taxes for each pay period to meet federal employment tax compliance standards. This includes the employeeâs and employerâs share of various taxes. These obligations cover withheld federal income tax, social security tax, medicare taxes, and federal unemployment tax. Calculating each amount and submitting timely payments through the Electronic Federal Tax Payment System (EFTPS) helps reduce audit risks and interest charges.

Key Steps in Payroll Tax Calculations

- Federal income tax withholding is based on each employeeâs Form W-4 and the current IRS tax tables.

- Social security tax is calculated at 6.2% of employee wages up to the annual wage base limit, with the employer matching the same rate.

- Medicare taxes are withheld at 1.45%, with the employer also contributing 1.45% on all wages.

- Employers must withhold an additional medicare tax of 0.9% for employees earning over $200,000 annually.

- The FUTA tax is 6.0% of the first $7,000 employee wages, reduced by applicable state unemployment tax credits.

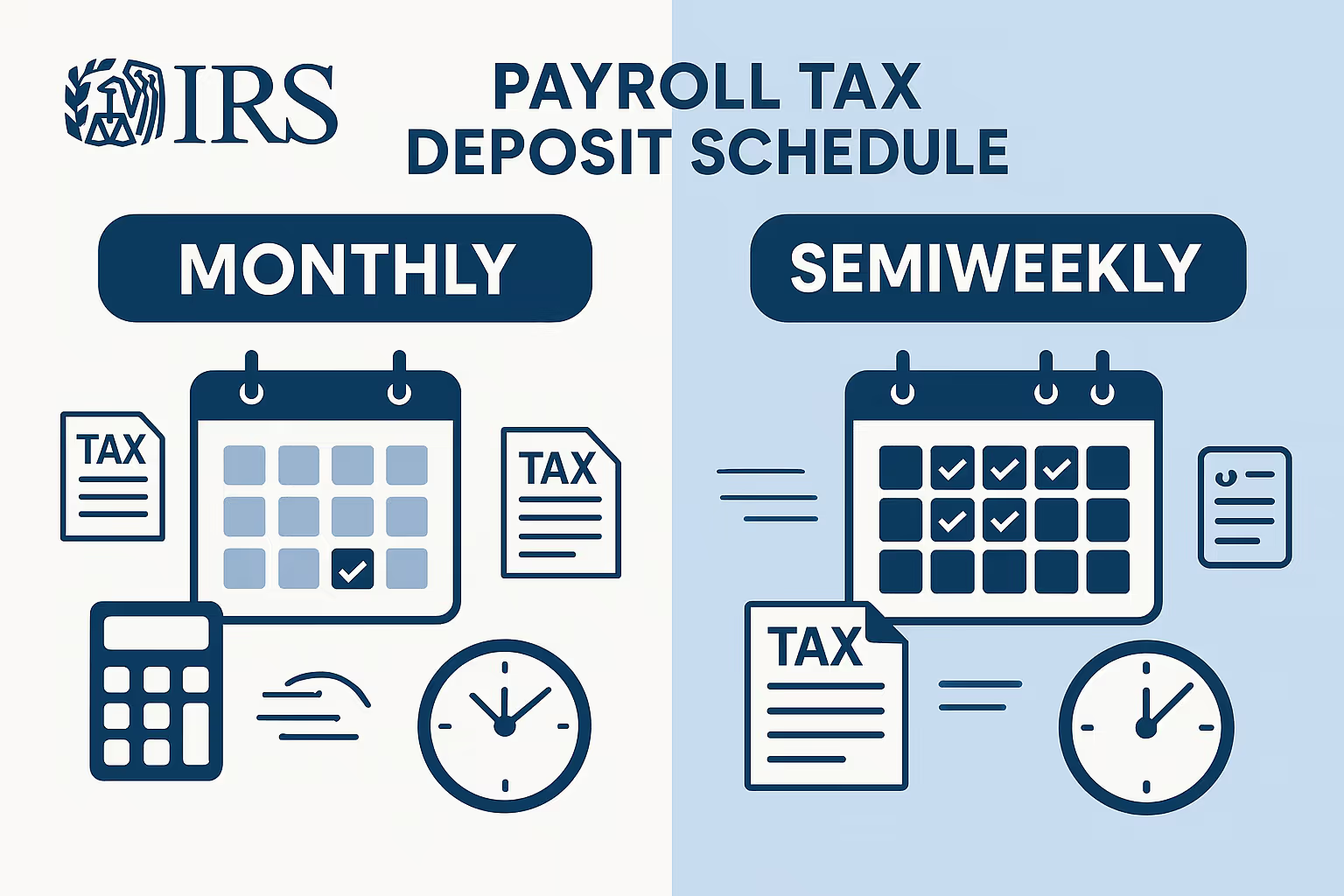

The Internal Revenue Service classifies employers as monthly or semiweekly depositors based on total tax liability in a lookback period. Most employers are required to use EFTPS to deposit taxes to the United States Treasury.

EFTPS Deposit Schedules and Compliance

- After payroll is issued, depositors must make payments by the 15th of the month.

- Semiweekly depositors must deposit taxes based on the payday: WednesdayâFriday payrolls are due the following Wednesday; SaturdayâTuesday payrolls are due the following Friday.

- If a business accumulates $100,000 in tax liability on any day, the full amount must be deposited by the next business day.

- To avoid discrepancies, employers must ensure deposits match the amounts reported on each tax return.

- Late deposits are subject to interest charges and significant penalties, even if the return is filed on time.

Accurate payroll tax calculations and timely EFTPS deposits help most employers stay compliant, reduce tax liability errors, and efficiently fulfill their employment tax obligations.

Special Situations: Exemptions, Contractors, and Fringe Benefits

Not all employees and compensation types follow the same payroll tax rules. Employers generally must recognize exceptional cases that affect their federal employment tax compliance. These include classifications like independent contractors, agricultural employees, household workers, and nonstandard forms of compensation such as fringe benefits. Proper handling of these cases is essential to calculate employer payroll taxes and meet all tax obligations accurately.

Independent Contractors and Worker Classification

No withholding required for contractors: Independent contractors are not subject to payroll tax withholding, and employers do not pay their employerâs share of social security or medicare taxes.

1099-NEC for qualifying payments: Businesses must issue Form 1099-NEC to each contractor paid $600 or more during the tax year.

Risks of misclassification: Improperly treating an employee as a contractor can result in serious consequences, including back taxes, interest charges, and tax liability penalties.

IRS classification rules apply: The Internal Revenue Service evaluates worker status using behavioral and financial control factors.

Consult a tax professional: When classification is unclear, employers should seek professional advice to avoid costly mistakes.

Exemptions and Fringe Benefit Considerations

Agricultural employees may qualify for exceptions: Specific rules govern social security tax and federal unemployment tax for farm workers.

Household workers follow different IRS guidance: If cash wages exceed a set threshold during a pay period, household employers must withhold and report employment taxes.

Local taxes vary by location: Some jurisdictions require additional payroll tax withholding alongside federal income and unemployment taxes.

Fringe benefits may be taxable: Items such as housing, bonuses, or vehicle allowances may require payroll tax withholding and must be reported accurately.

Proper valuation is required: The fair market value of fringe benefits must be included when calculating the employeeâs wages and the employerâs tax obligations.

Understanding these unique payroll situations helps businesses comply with federal employment tax requirements. It also ensures that employeesâ wages are reported correctly and that employers pay what is owed. Addressing these variables proactively helps most employers meet filing requirements, stay ahead of due dates, and avoid significant penalties.

Best Practices to Stay Compliant and Avoid Penalties

Compliance with federal employment tax rules requires consistency, organization, and timely action. Even minor errors in calculating or reporting payroll taxes can lead to serious consequences, such as interest charges or penalties from the Internal Revenue Service. Employers generally reduce risk and strengthen payroll operations by following these essential best practices throughout each pay period and tax cycle.

Establish a complete payroll calendar:

A well-maintained calendar should outline all pay periods, deposit due dates, and filing deadlines for specific forms. This allows employers to manage payroll workflows accurately and avoid late filings.

Automate calculations using trusted payroll software:

Quality payroll systems help employers calculate employer payroll taxes and automate tax filing. They also send reminders for deposit schedules and ensure taxes are paid to the United States Treasury through EFTPS.

Rely on a tax professional for complex cases:

Businesses with multiple tax jurisdictions or unique employment structures should consult a tax advisor. This ensures compliance with federal income tax, social security tax, and unemployment tax requirements.

Reconcile records before every deposit:

Before submitting taxes withheld from employeesâ wages, employers should verify that payroll summaries match their deposit amounts. Tracking the employerâs and employeeâs share separately avoids errors in reported payroll taxes.

Retain documentation for each reporting period:

Employers must keep accurate records of payments, forms filed, and payroll tax withholding. These records support tax return preparation and help demonstrate compliance in the event of an audit.

Applying these best practices supports accurate tax filing, helps employers meet due dates, and protects against avoidable penalties. Most employers that invest in reliable payroll systems and professional guidance remain in good standing with the Internal Revenue Service. Maintaining strong processes also helps ensure employees receive accurate paychecks and tax documents, further enhancing trust and accountability. Federal employment tax compliance is not only a legal requirement but an essential part of responsible business operations.

Additional Payroll Compliance Topics for Employers

Federal employment tax compliance includes more than just regular filing and deposits. Employers are also responsible for understanding additional issues that affect payroll accuracy and long-term tax reporting. These details often arise during audits, tax return reconciliation, or when businesses expand operations across multiple jurisdictions. Recognizing and addressing these topics early helps avoid unnecessary interest charges, tax liability adjustments, and compliance risks with the Internal Revenue Service.

- Tax credits may reduce total employer liability: Although they do not apply directly to withheld federal income tax, eligible credits may lower the amount owed on an employerâs annual return.

- The United States Treasury expects matched records: All deposits must align with amounts reported on IRS forms. Inconsistencies may trigger penalty notices or requests for clarification.

- The employerâs share and the employeeâs share must be reported separately. Federal forms such as Form 941 require accurate breakdowns of social security and Medicare taxes by source.

- Some employers are subject to local taxes: Depending on the location, additional reporting obligations may apply beyond federal tax withholding.

- Most employers must track multi-state payroll accurately: Businesses with employees working in multiple states must comply with varying state unemployment tax and wage reporting rules.

Staying aware of these issues supports clean reporting and reduces compliance errors. Employers should regularly review their payroll systems and verify that all relevant detailsâsuch as tax credits, local obligations, and multi-state filingsâare accounted for each pay period. Strong internal systems, supported by a qualified tax professional when needed, help employers meet every requirement. By going beyond the basics, businesses protect themselves from audit exposure, penalties, and other serious consequences tied to inaccurate employment taxes.

Frequently Asked Questions

What taxes are included in federal employment tax compliance?

Federal employment tax compliance includes withheld federal income tax, medicare taxes, Social Security tax, and the employerâs share of federal unemployment tax. These taxes must be calculated for every pay period and submitted to the Internal Revenue Service IRS. Employers are responsible for ensuring timely deposits and filing accurate tax returns. All payroll deposits should be made through an approved financial institution or EFTPS to correctly credit the employeesâ paychecks.

How do I calculate employer payroll taxes correctly?

To calculate employer payroll taxes, start with the employeeâs Form W-4 and apply the correct IRS tax rates. Withhold federal income tax based on filing status and allowances. Apply social security and medicare taxes to gross wages, and withhold the additional tax if applicable. The employer must also contribute their share. Calculations must include the federal unemployment tax and account for state tax credits to ensure compliance with the Internal Revenue Service IRS standards.

When are my payroll taxes due to the IRS?

Payroll taxes must be deposited based on the assigned deposit schedule. Monthly depositors submit taxes by the 15th of the following month. Semiweekly depositors follow IRS rules tied to payroll timing. Most employers file Form 941 quarterly with the Internal Revenue Service IRS. Deposits should be made through a financial institution using EFTPS. All employers must ensure payments reflect employeesâ paychecks and are submitted accurately to avoid interest charges or late deposit penalties.

What happens if I misclassify a worker as an independent contractor?

If an employer misclassifies a worker, the Internal Revenue Service IRS may impose serious consequences, including unpaid taxes, interest, and penalties. Employers who avoid paying the employerâs share of Medicare and Social Security taxes risk audits. Responsible persons may be held liable for trust fund recovery penalties. Unlike employees, independent contractors do not have taxes withheld, and self-employed individuals are responsible for paying their tax liabilities, including Medicare and Social Security taxes.

%2520What%2520Employers%2520Need%2520to%2520Know%2520About%2520IRS%2520Liability%2520and%2520Payment.avif)