Employment tax fraud is the deliberate evasion of required tax obligations related to payroll, withholding, and employment-related filings. Business owners across various industries, including medical tourism and healthcare, are legally responsible for collecting and paying several types of employment taxes to the federal government. These taxes include federal income tax withholding, social security, medicare taxes, and other employment tax returns submitted on a scheduled basis. When businesses willfully fail to report or pay these obligations, the Internal Revenue Service (IRS) may initiate audits and criminal investigations to address fraudulent conduct.

In recent years, particularly over the last three years, the IRS Criminal Investigation Division (IRS CI) has increased enforcement against employment tax fraud cases. These investigations often begin when a tax preparer files suspicious returns or when a business repeatedly neglects to submit proper forms or withholding taxes. Misreporting income, manipulating deductions, or misclassifying employees are all red flags that trigger further review. Employers who fail to comply with the Internal Revenue Code may face severe financial penalties, loss of business operations, and, in some cases, imprisonment.

Medical business owners and UK-based entrepreneurs managing U.S. operations must understand the full scope of their tax responsibilities. Being proactive helps prevent interest accrual, unexpected payment demands, and reputational damage. This guide explores common tax scams, legal consequences, and practical ways to reduce your tax burden while remaining compliant.

What Are Employment Taxes and Who Must Pay Them?

Employment taxes are mandatory contributions employers collect and submit to the Internal Revenue Service. These taxes fund critical federal government programs such as Social Security, Medicare, and unemployment insurance. Employers must withhold specific amounts from employee wages, then match those contributions through employer-paid taxes. Failing to comply with these obligationsâwhether by omission or intentâcan trigger an IRS audit, financial penalties, and even criminal investigations under the Internal Revenue Code.

Two broad categories define employment taxes: withheld taxes collected from employees and additional taxes paid directly by employers. The IRS considers withheld taxes especially serious because employers hold money in trust for the federal government. You can explore the full employment tax types and obligations list through official IRS guidance.

Employer Responsibilities

- Employers must withhold federal income tax, Social Security, and Medicare taxes from employee wages.

- They are required to match FICA taxes by paying their share of Social Security and Medicare contributions.

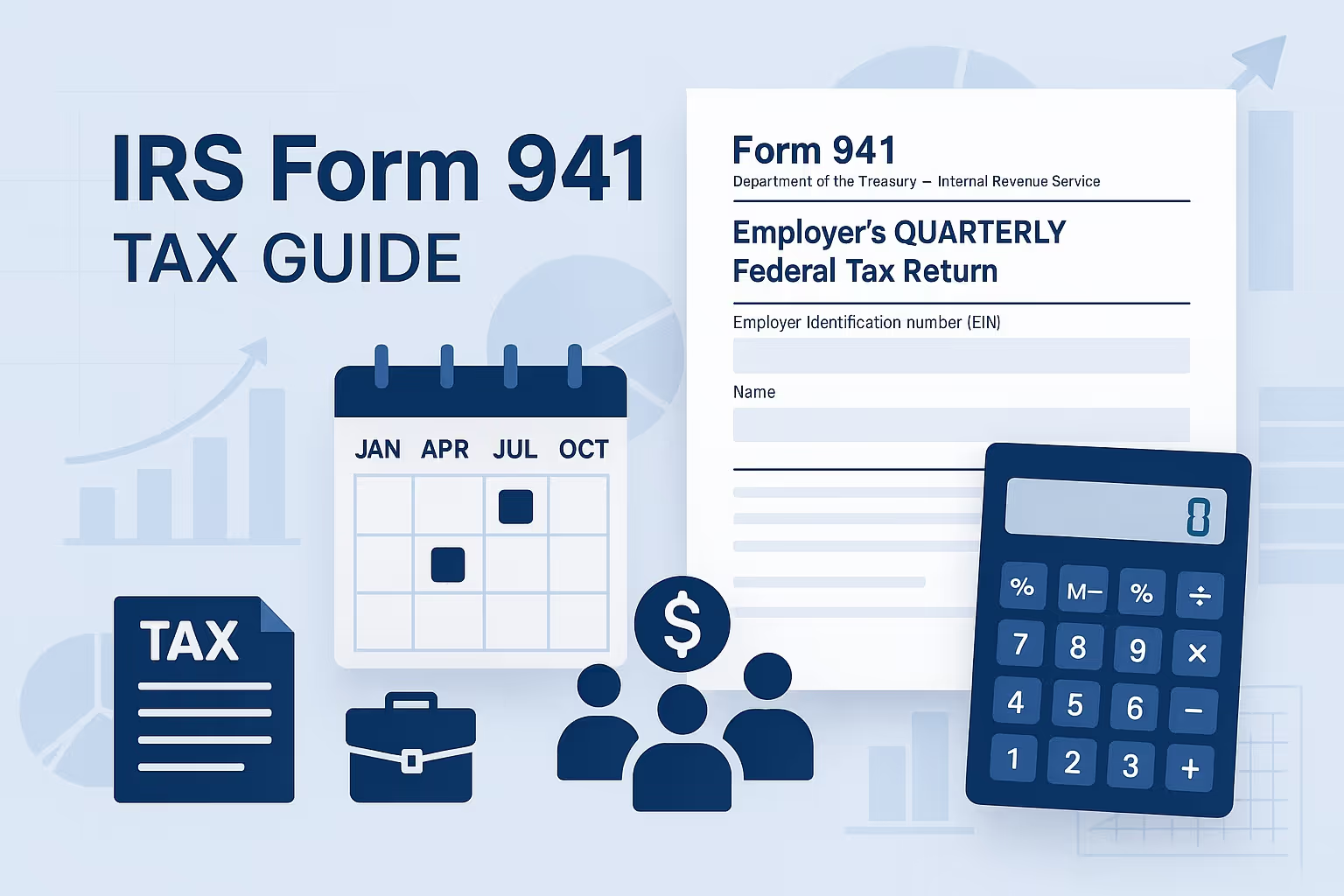

- Employment tax returns, such as Form 941 and Form 940, must be filed accurately and on time.

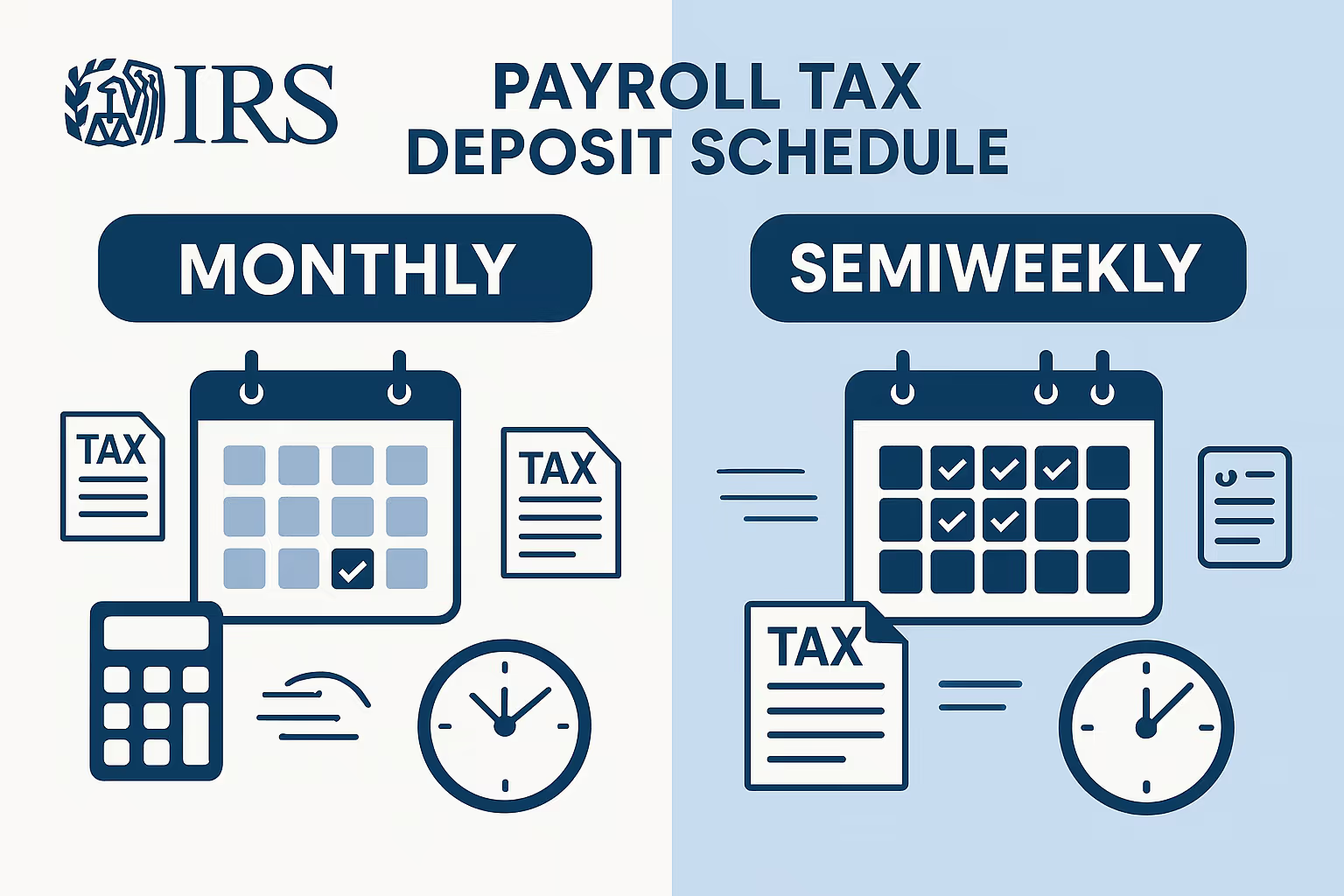

- Deposits must be made according to the IRS schedule, often through the EFTPS system.

- Employers must retain detailed payroll records for each employee, including wage calculations and withholding amounts.

Employee Responsibilities

- Employees contribute through automatic deductions from their paychecks for FICA and federal income tax.

- Workers should review wage statements regularly to confirm accurate withholding.

- Any discrepancies or fraud should be reported promptly to the IRS.

- Filing accurate tax returns ensures that wage and tax records match IRS expectations.

- Employees are also responsible for updating withholding elections to reflect their income and deductions.

If a business willfully fails to meet these responsibilities, it risks enforcement actions and potential personal liability for those in control of finances. These obligations apply equally to owners, financial managers, and even a tax preparer designated to handle filings. Understanding the full scope of tax responsibilities is essential for every employer. Compliance avoids penalties and interest, supports ethical payroll practices, and prevents long-term tax burden complications.

â

Typical Employment Tax Fraud Schemes and Tax Scams

Employment tax fraud is any attempt to avoid paying legally required payroll taxes through misrepresentation, concealment, or improper filings. These acts violate the Internal Revenue Code and can lead to audits, financial penalties, and criminal investigations by the Internal Revenue Service. In many cases, employers may underestimate the full scope of their responsibilities or work with a tax preparer who participates in fraudulent practices. Business owners in healthcare and medical tourism industries must remain vigilant to avoid such traps, especially when managing U.S. payroll from abroad.

The IRS has identified several typical schemes used to commit employment tax fraud:

- Employers classify regular employees as independent contractors to avoid paying withholding taxes and FICA taxes.

- Some businesses pay wages in cash to conceal actual compensation and avoid filing employment tax returns.

- Others submit false returns or underreport income to reduce their apparent tax burden.

- Employers may fail to file forms such as Form 941 or deposit collected taxes as required.

- Redirecting payroll tax funds to cover unrelated expenses or personal use is another frequent violation.

Beyond these internal schemes, external tax scams have become increasingly sophisticated. The IRS warns taxpayers about fraudulent preparers and fake notices demanding urgent payment. These scams can lead to financial loss and criminal exposure for business owners who are unaware of how these tactics operate.

Tax scams to watch for include:

- Preparers who promise substantial refunds or request inflated wage data.

- Communications that mimic IRS letters or notices but originate from fake sources.

- False tax returns filed using stolen personal information or business credentials.

- Preparers who omit signatures or supporting documents when filing tax returns.

- Phony payroll firms that collect withholding taxes but fail to remit them to the IRS.

Employers are responsible for verifying all filings, payments, and professional advisors associated with their tax account. The consequences can be severe if the IRS determines that a person has willfully failed to comply. To report suspicious activity or fraudulent behavior, visit the IRS tax fraud reporting portal. Whether intentional or not, these actions can result in interest, penalties, and loss of business credibility.

IRS Criminal Investigations: How Fraud Is Detected and Prosecuted

The Internal Revenue Service Criminal Investigation Division (IRS CI) is the agencyâs primary law enforcement unit for investigating violations of federal tax law. When a business willfully fails to fulfill employment tax obligations or submits false tax returns, IRS CI may open a criminal case. Most investigations begin with an audit or red flags submitted by a tax preparer. Inconsistent payroll records, large unpaid balances, and repeated non-filing over the last three years are key triggers for deeper review.

Red Flags That Trigger Investigations

- Ongoing failure to file employment tax returns for multiple quarters.

- Significant payroll amounts with no corresponding deposits of withholding taxes.

- Misclassified employees or payroll reports that do not match IRS records.

- Engagement with tax preparers who lack credentials or file incomplete forms.

- Contradictions between declared income and bank account activity.

If these issues suggest fraud, IRS personnel refer the matter to IRS CI. This unit conducts in-depth financial investigations using law enforcement tools like interviews, subpoenas, and asset tracing. Their findings determine the taxpayerâs intent and the scope of violations.

How a Case Moves Forward

- Revenue officers and auditors escalate the case to IRS CI.

- CI agents gather payroll records, tax filings, and financial statements.

- Withholding taxes that are not remitted are documented and calculated.

- The full scope of interest, penalties, and unpaid tax liabilities is reviewed.

- The case is forwarded to the Department of Justice for criminal prosecution when appropriate.

IRS CI works closely with federal prosecutors to pursue civil and criminal charges. These efforts often result in full restitution, asset seizures, and prison time for the responsible parties. To view real examples of recent prosecutions, visit the DOJâs Criminal Employment Enforcement updates.

Employers targeted for criminal investigation must respond thoroughly to all IRS inquiries. A failure to comply or provide records can lead to harsher penalties. Business owners should recognize that personal liability can apply when they manage payroll decisions and knowingly ignore tax obligations. Remaining compliant, truthful, and responsive is the most effective way to avoid IRS scrutiny and criminal liability.

Penalties and Consequences of Employment Tax Fraud

Employment tax fraud can result in substantial financial and legal consequences. When the IRS determines that a business has failed to meet its payroll tax obligations, it may impose civil and criminal penalties. These penalties apply to employers who fail to file tax returns, underreport income, or withhold taxes improperly. The Internal Revenue Code allows the IRS to collect unpaid balances, enforce compliance through liens or seizures, and refer severe cases for criminal investigation. One of the most aggressive civil enforcement tools is the Trust Fund Recovery Penalty (TFRP), which holds individuals liable for unremitted payroll taxes.

Civil Penalties

- Failure to file employment tax returns leads to a penalty of 5% per month, up to a maximum of 25%.

- Late deposits of withholding taxes can incur penalties ranging from 2% to 15%, based on how long the payment is delayed.

- Errors in reporting can result in a 20% accuracy-related penalty for negligence or substantial understatements.

- Confirmed fraud allows the IRS to impose a civil fraud penalty of 75% of the underpaid tax.

- Interest accrues until the full amount is collected from the original due date.

Civil actions may also include federal tax liens on business or personal property, which can affect credit and the ability to sell or transfer assets. The IRS does not excuse liability based on third-party involvement; even when a tax preparer handles filings, the employer remains ultimately responsible.

Criminal Penalties

- Willfully failing to collect or pay over employment taxes can result in up to five years in prison and fines of up to $250,000 for individuals.

- Filing false tax returns or submitting fraudulent documentation may lead to imprisonment and additional fines.

- Attempts to obstruct IRS collection or enforcement efforts carry criminal penalties.

- Convictions typically include restitution, interest, and long-term monitoring by the IRS.

- Business assets and personal accounts may be seized to satisfy criminal judgments.

To avoid these consequences, employers must maintain accurate records, review their filings regularly, and respond promptly to IRS notices. Missteps in payroll tax compliance are not only costly but can also jeopardize the future of the business itself.

Real IRS and DOJ Case Examples from the Last Three Years

Understanding how employment tax fraud is prosecuted helps business owners recognize the seriousness of noncompliance. Over the last three years, the Internal Revenue Service and the Department of Justice (DOJ) have aggressively pursued employers across various industries who willfully failed to submit employment tax returns or misused payroll funds. These cases illustrate the full scope of legal consequences, including criminal investigations, restitution, and imprisonment. Medical professionals, international clinic operators, and tax preparers should all take note of how the IRS and DOJ handle these violations.

Notable DOJ Prosecutions

- A payroll company owner in Maryland was sentenced to over one year in prison for failing to pay over-collected withholding taxes and embezzling from employee benefit plans.

- In Florida, a payroll service provider received 50 months in prison for collecting taxes but submitting false tax returns while failing to remit the funds.

- A New Hampshire software CEO was sentenced to 30 months in prison for deliberately avoiding over $14 million in payroll taxes, despite collecting them from employee wages.

- An Oregon business owner pleaded guilty to withholding payroll taxes but failing to deposit them with the IRS as required.

Key Enforcement Themes

- The DOJ and IRS consistently pursue both large corporations and small businesses.

- Prison terms range from one to five years, depending on the scale and willfulness of the violation.

- Courts require full restitution of unpaid employment taxes, penalties, and accumulated interest.

- Many prosecuted businesses attempted to conceal misconduct by manipulating forms or hiding wage transactions.

- IRS Criminal Investigation agents lead most of these cases, working with DOJ attorneys and forensic auditors.

These examples show that tax fraud is not limited to one industry or region. Businesses in healthcare, technology, construction, and services have all faced serious legal outcomes for failing to fulfill employment tax responsibilities. In each case, employers willfully refused to remit trust fund taxes or filed falsified returns to reduce their tax burden. The IRS has clarified that even international operators or businesses with complex structures are not exempt from enforcement. Staying compliant protects your business, employees, and professional credibility in the U.S. market.

Staying Compliant with Employment Tax Obligations

Employment tax compliance is not just a filing taskâit is a legal responsibility that affects every aspect of payroll, employee benefits, and business integrity. The Internal Revenue Service expects employers to file timely and accurate employment tax returns, submit proper payments, and promptly respond to any notices. A failure to meet these obligationsâintentional or due to negligenceâcan result in interest charges, financial penalties, or criminal investigations. Business owners, especially those managing operations remotely or through complex international structures, must control every transaction tied to payroll taxes.

Best Practices for Tax Compliance

Effective compliance begins with internal systems and routine oversight.

- Employers should file Forms 941 and 940 by the required deadlines and confirm receipt by the IRS.

- Withholding taxes must be deposited accurately and on schedule through the Electronic Federal Tax Payment System (EFTPS).

- Payroll records, including wage statements, benefit deductions, and classification records, must be retained for at least four years.

- Any discrepancies in wage payments or deductions should be resolved before filing tax returns.

- Employers should review IRS correspondence and resolve open notices quickly to prevent escalation.

IRS audits often begin with minor oversights, such as missed deposits or inconsistencies in Form 941. When these issues are left unaddressed, they can lead to further review, interest accumulation, or additional reporting requirements. Maintaining a calendar for filing deadlines and using secure payroll software reduces these risks.

Choosing the Right Tax Preparer

Hiring a qualified tax preparer is essential, but oversight remains the employerâs duty.

- Only work with preparers registered with a valid Preparer Tax Identification Number.

- Avoid firms that guarantee refunds or suggest omitting income or payroll data.

- Always request and review copies of submitted forms, especially those involving employee wages and deductions.

- Ensure tax returns are signed and include all required attachments.

- If fraud or errors are discovered, report the issue to the IRS immediately.

Employers must understand the full scope of their responsibilities and never assume someone else is accountable for their filings. The IRS does not waive penalties based on reliance on a third party. Protecting your business requires regular reviews, proper documentation, and clear communication with every person involved in payroll and compliance.

U.S. Tax Law, EU Connections, and International Considerations

Business owners in the European Union managing U.S. clinics or payroll operations must comply with American employment tax law. The Internal Revenue Service enforces federal obligations such as income tax withholding, Medicare taxes, Social Security, and federal unemployment contributions. These obligations apply regardless of where the business owner resides. Any person operating or overseeing a U.S.-based business that pays wages must follow Internal Revenue Code standards and submit accurate employment tax returns.

International oversight has tightened over the last three years. The IRS now collaborates more closely with European Union tax authorities through formal agreements supporting border enforcement. Foreign-based businesses are no longer immune from scrutiny. Payroll handled abroad must still meet U.S. deposit deadlines, withholding rules, and filing requirements. The employer remains ultimately responsible when a tax preparer fails to report income or underpays trust fund amounts. Interest penalties, or even criminal investigations, may follow. If irregularities surface

To stay compliant, EU-based employers should establish precise internal controls and work only with professionals experienced in U.S. employment tax law. Payroll and financial records should be reviewed regularly, and all tax returns must be filed on time. When the IRS issues a notice, it should be addressed immediately. Taxpayers must also be ready to respond to audits or information requests, even when operating outside the U.S. Taking a proactive approach ensures that the business meets its obligations, avoids unnecessary penalties, and protects its legal standing in both jurisdictions. Maintaining transparency and a full scope of documentation is essential when operating across international tax systems.

Frequently Asked Questions

What is the Trust Fund Recovery Penalty, and who can be held liable?

The Trust Fund Recovery Penalty (TFRP) is a civil penalty under the Internal Revenue Code. It allows the IRS to hold any responsible personâsuch as a business owner, financial officer, or payroll managerâpersonally liable for unpaid payroll taxes withheld from employees. If those trust fund taxes are collected but not submitted, the IRS can pursue the full amount, plus interest, from anyone with authority over financial decisions.

How does the IRS determine if someone willfully failed to comply?

Willfulness means a conscious, voluntary decision to disregard known tax obligations. The IRS considers whether the person was aware of the requirement and chose not to act. Evidence such as ignoring IRS notices, using funds for other business expenses, or prioritizing non-tax payments often supports a willful failure finding. Even reckless disregard may qualify. The IRS does not require proof of intent to defraudâonly intent to disregard the law.

Can a tax preparer be held accountable for fraud?

Tax preparers who knowingly submit fraudulent tax returns can face civil or criminal penalties. However, the employer is still responsible for all tax obligations. Business owners must verify all filings and ensure documents are correctly submitted. Relying on a preparer without oversight is not a defense. When errors are discovered, employers should contact the IRS and request help through programs designed to assist taxpayers with filing corrections.

What are the warning signs of employment tax fraud?

Red flags include missed filings, inconsistent payroll reports, inflated deductions, and unexplained wage payments. Businesses receiving repeated IRS notices or dealing with preparers who resist transparency should investigate. If you operate across jurisdictionsâsuch as from the European Unionâmaintaining oversight of U.S. payroll operations is critical. Any attempt to avoid IRS scrutiny through unrecorded transactions or misclassification may result in penalties. Immediate action protects your business and ensures tax compliance.

Can both civil and criminal penalties be applied for the same offense?

Yes, the IRS may apply civil penalties like fines and interest while the Department of Justice pursues criminal charges such as tax fraud or obstruction. These actions are separate and may result in imprisonment, restitution, or both. If your business operates internationally, penalties can extend across borders. The IRS may coordinate enforcement with authorities in countries like the European Union, especially when financial records show intentional misconduct.

How long does the IRS have to investigate or assess penalties?

The IRS typically has three years from the date a tax return is filed to assess penalties. If fraud or non-filing occurs, there is no statute of limitations. Employers should keep records of employment tax returns and payments for at least six years. All documents should be marked with the date last reviewed or updated. Accurate recordkeeping is your best defense during audits or criminal investigations.

What records should I maintain to protect my business?

Employers should retain wage reports, Forms 941 and 940, payment receipts, bank statements, and IRS notices. Records should be complete and accurate and reviewed at least annually. Supporting documents must reflect the last reviewed or updated date. Payroll files should also assist in verifying employee classifications, benefit deductions, and withholdings. Proper records reduce audit risk and prove compliance. Maintaining U.S.-compliant records is especially critical for international operators when working with foreign banks or contractors.

%2520What%2520Employers%2520Need%2520to%2520Know%2520About%2520IRS%2520Liability%2520and%2520Payment.avif)