Veterans

VeteransVeterans deserve tax benefits because they have made sacrifices that directly protect the freedoms of the United States. These benefits recognize the hardships of military service, including long deployments and physical or emotional challenges faced after separation. Tax relief ensures veterans keep more of their earned income, which supports long-term financial stability and family security. Offering tax benefits is one way the federal government continues honoring military service beyond active duty years.

Truck Drivers

Truck DriversDue to their industry's unique nature, truck drivers often face complex tax rules that differ from those of traditional employees. Long hours on the road create special financial considerations that affect income reporting and deductions. Many drivers must track expenses closely to claim legitimate benefits without raising IRS concerns. Understanding these challenges helps drivers avoid penalties and reduce stress during tax season.

Teachers

TeachersTeachers often cover classroom expenses using their money, buying supplies and resources to support student learning. These out-of-pocket purchases quickly add up, creating financial stress throughout the school year. Many educators do not receive reimbursement from schools or districts, making teacher tax deductions a critical way to recoup some costs.

Tattoo Artists & Self-Employed Therapists

Tattoo Artists & Self-Employed TherapistsRunning your business gives tattoo artists and therapists independence, but tax responsibility is unavoidable. Self-employed individuals must manage records, receipts, and expenses with accuracy. They must calculate taxable income carefully because underreporting can lead to IRS scrutiny. Unlike employees, they shoulder the full self-employment tax without employer contributions.

Spanish-Speaking / ITIN Taxpayers

Spanish-Speaking / ITIN TaxpayersITIN taxpayers are essential in maintaining fairness within the United States tax system. They file federal tax returns even without eligibility for a Social Security Number. The IRS uses the Individual Taxpayer Identification Number to track compliance accurately. This ensures taxpayers without SSNs can report income and avoid legal or financial risks.

Social Security Recipients

Social Security RecipientsSocial Security provides critical financial support to millions of Americans during retirement, disability, or after a family member’s death. It ensures a consistent income when people stop working or cannot earn due to health conditions. These benefits help cover basic living expenses and reduce financial insecurity. Without Social Security, many households would face significant financial hardship.

Social Media Influencers & Adult Industry WorkersThe IRS has started paying closer attention to influencer earnings across all social platforms. Revenue from brand deals, sponsorships, and ad revenue is no longer under the radar. Creators who once ignored taxes now face increased scrutiny from federal auditors. This shift signals that digital entrepreneurship must now align with traditional tax compliance standards.

Small Nonprofit Owners

Small Nonprofit OwnersSmall nonprofit owners start organizations every day to serve communities without chasing profit. They often balance limited budgets, volunteer help, and passionate missions. Unlike large institutions, they rarely have full legal or financial teams, which makes understanding IRS rules especially important for their survival.

Single Parents

Single ParentsSingle-parent tax rules directly shape your financial outcome during tax season. They determine whether you maximize savings or overpay. The IRS offers targeted relief programs to support households led by one parent. Understanding these rules ensures you claim every available deduction and credit accurately.

Seniors

Seniors A tax guide for seniors is essential because older adults face unique tax rules and opportunities after retirement. Many seniors underestimate the impact of new deductions and credits designed specifically for their age group. These provisions can significantly reduce taxable income, easing financial stress during retirement. Having a clear resource ensures older adults claim every benefit they deserve.

Self-Employed / Freelancers

Self-Employed / FreelancersSelf-employment allows people to choose clients, set schedules, and grow businesses on their terms. This independence allows creativity and flexibility that traditional jobs rarely provide to individuals. However, freedom also comes with managing every financial and legal detail. Taxes become one of the most important obligations for the self-employed.

Recently Divorced

Recently DivorcedDivorce or separation transforms household finances by altering income streams, responsibilities, and legal obligations. Tax planning becomes urgent since deadlines remain strict. Recently divorced taxpayers often discover that filing status significantly changes their overall tax bracket. This adjustment can raise liabilities quickly without proper preparation.

Real Estate Investors / Flippers

Real Estate Investors / FlippersReal estate investing creates wealth through rental income, appreciation, or flipping houses, but strict regulations govern every transaction. The IRS carefully monitors real estate investors and flippers because misreporting can distort taxable income. Each property sold or held carries unique tax implications that require proper classification. Investors who ignore these details risk costly mistakes and legal issues.

Pastors/Church Workers

Pastors/Church WorkersPastors and church workers face complex tax obligations that combine employee and self-employed rules. Clergy must balance income tax with self-employment requirements. The minister's housing and parsonage allowance reduces federal income tax but demands accurate recordkeeping. Without careful compliance, ministers risk overpaying taxes or losing valuable exemptions.

Musicians, Performers & Freelance Writers

Musicians, Performers & Freelance WritersCreative professionals like musicians, performers, and freelance writers are classified as self-employed because they control their income streams. Unlike salaried workers, they don’t receive automatic tax withholding or employer-provided benefits, which increases their responsibility for accurate reporting. Each project, gig, or royalty payment counts as taxable income, requiring detailed recordkeeping. The IRS expects these professionals to track and report income with precision.

Multi-State Movers & Remote Workers

Multi-State Movers & Remote WorkersMoving across state lines complicates your tax picture because each state has unique rules for income and residency. Remote employees often face conflicting payroll taxes when employers withhold in the wrong jurisdiction. These mismatches can create double taxation if both states claim the same income. Without careful planning, taxpayers lose money and risk disputes.

Low-Income Taxpayers

Low-Income TaxpayersLow-income taxpayers often struggle with confusing income tax rules while balancing tight budgets and everyday living expenses. They may not realize that federal tax laws provide specific credits to increase refunds for qualifying households. These missed opportunities can mean losing significant money that could support rent, food, or essential bills. Understanding obligations and available benefits is the first step toward protecting limited financial resources.

Immigrants

ImmigrantsImmigrants must understand U.S. tax obligations because taxes affect financial stability, legal compliance, and future opportunities in America. Taxes determine eligibility for certain credits and benefits, including family-related deductions. Knowing the rules helps immigrants avoid confusion and costly mistakes. A clear immigrants tax guide provides structured direction for navigating complex income tax requirements.

Immigrant EntrepreneursImmigrant entrepreneurs strengthen local communities by opening restaurants, shops, and service companies that create sustainable jobs. They also introduce cultural diversity, which enriches consumer choices and fosters innovation. Many immigrant-owned businesses expand quickly, contributing significantly to regional tax bases and economic resilience. Their collective efforts build stronger, more inclusive neighborhoods that benefit immigrants and long-term residents.

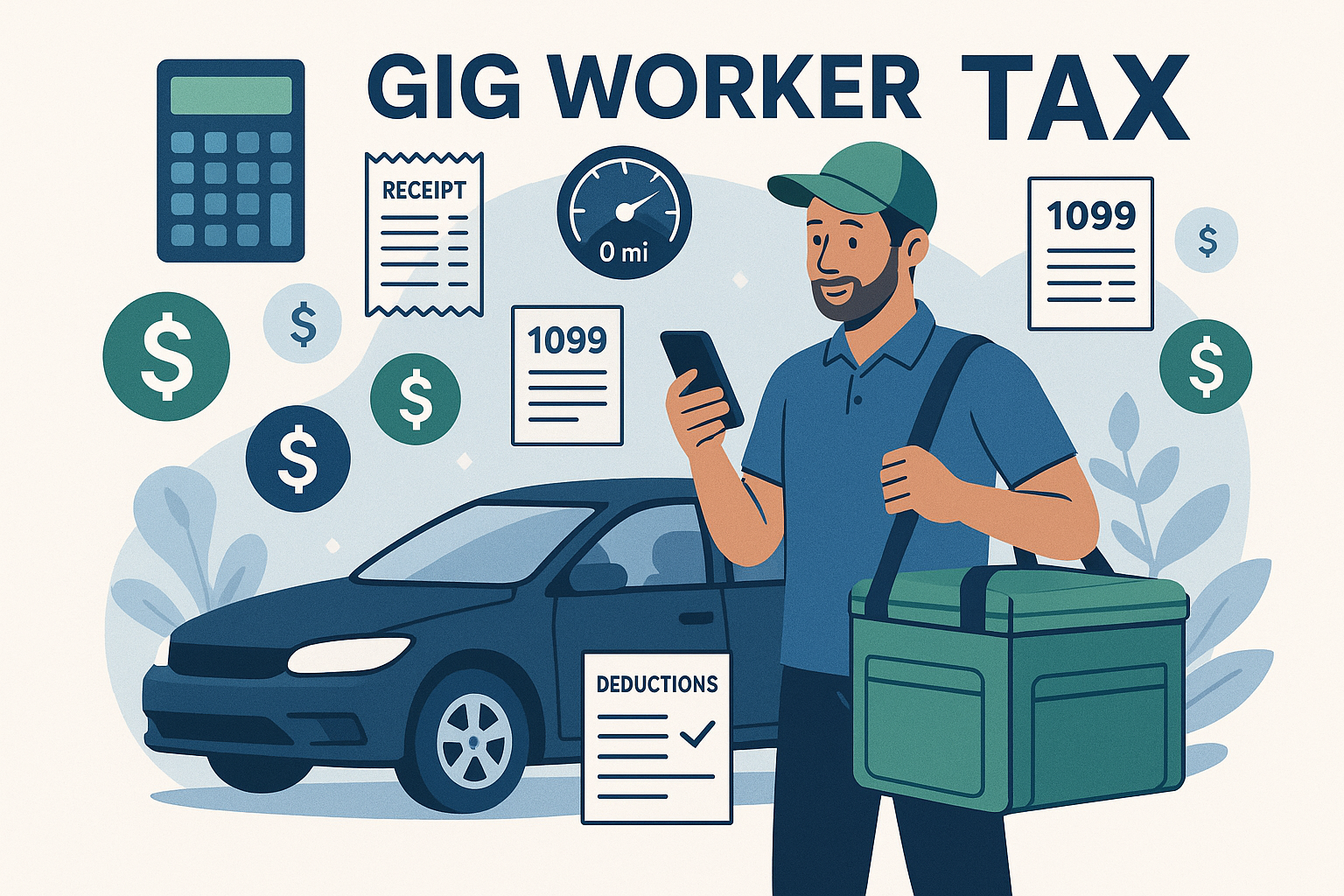

Gig Workers The gig economy has transformed traditional employment by allowing workers to earn flexible income through platforms like Uber and DoorDash. Delivery drivers and rideshare workers operate independently, controlling schedules while managing their business responsibilities. Unlike employees, they handle client interactions, vehicle upkeep, and record-keeping without direct employer oversight. This independence creates unique opportunities but also introduces additional responsibilities regarding financial planning and taxes.

Felons Returning to Workforce & Displaced Workers from LayoffsPeople re-entering the workforce after incarceration or layoffs face unique barriers and opportunities during job searches. A criminal record can make finding stable employment more difficult for former inmates than other applicants. Laid-off workers, meanwhile, must navigate unemployment benefits while seeking new work or training opportunities. Both groups share the goal of restoring financial stability and securing long-term careers.

Expat Taxpayers Returning to the U.S.Expat taxes can feel overwhelming when you return to the U.S. after living abroad for several years. You must navigate complex tax rules while adjusting to life back home at the same time. The IRS requires careful reporting of worldwide income, which adds extra pressure to returning expatriates. Preparation and awareness help minimize stress and avoid costly mistakes during your transition.

Early Retirement Withdrawals

Early Retirement WithdrawalsEarly retirement withdrawals give individuals quick access to money when unexpected expenses arise. These funds can help cover medical bills or job losses. However, withdrawing early can severely reduce long-term retirement savings and growth potential. Many taxpayers later regret the financial setback caused by early access to retirement accounts.

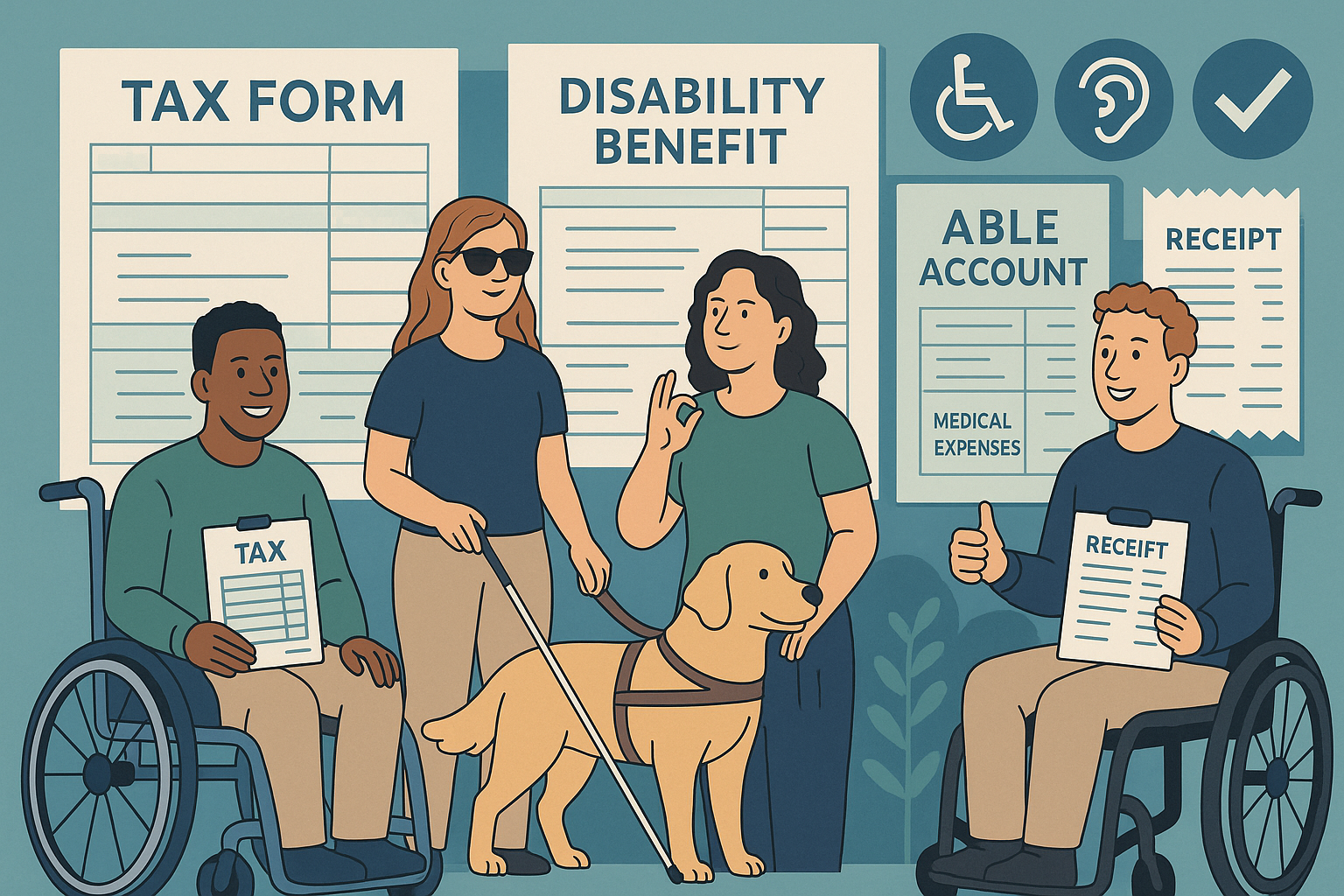

Disabled Individuals

Disabled IndividualsDisability rules create specific tax opportunities for individuals and small businesses that often remain underused without proper guidance. The IRS provides frameworks that outline how taxpayers should report disability income and related expenses. These rules directly affect eligibility for valuable deductions and credits that reduce taxable income. Without following them, individuals and businesses risk losing significant financial relief.

Disability Recipients & Caregivers

Disability Recipients & CaregiversDisability recipients receive financial support due to a condition limiting their work ability. Caregivers, often family members or professionals, provide daily assistance to support a loved one’s health and well-being. Their roles extend beyond personal care, including managing finances, taxes, and essential paperwork. Understanding these responsibilities helps protect both recipients and caregivers from unnecessary financial and legal challenges.

Crypto TaxpayersCrypto taxpayers include individuals and businesses that engage in digital asset transactions for investment, payments, or rewards. The IRS classifies cryptocurrencies as property, creating tax obligations similar to other investments. Each purchase, sale, or exchange of digital assets can trigger taxable events. Taxpayers must keep records of every crypto transaction to file them correctly.

Construction Workers

Construction WorkersConstruction workers often struggle with taxes because payment methods differ from traditional jobs. Many receive 1099 forms instead of W-2s. Independent contractors must manage their own tax withholdings and quarterly estimated payments. Without preparation, these obligations can quickly overwhelm even experienced professionals.

Barbers/Salon OwnersRunning a barbershop or salon demands strong business management alongside styling expertise. Owners must accurately track income, expenses, and deductions. The IRS requires proper documentation for every service and sale, especially cash transactions. Without consistent compliance, small errors may quickly become serious tax liabilities.

1099-K / PayPal / CashApp Income

1099-K / PayPal / CashApp IncomeThe 1099-K form is a tax document that reports payments received through third-party platforms like PayPal or Cash App. It shows the gross payment amount processed on your behalf, not just net earnings after fees. This form is issued by the payment processor, not the IRS itself. Both you and the IRS receive a copy for tax reporting purposes.

FAQS

Schedule your free, confidential tax relief review today.

Copyright © 2025 Get Tax Relief Now